The new inflationary crisis looming in 2026 risks jeopardizing the recovery of the organic market. In this comprehensive report, we review the evolution of the market worldwide, then focus on Europe and examine future prospects.

The organic market had barely recovered from the post-Covid contraction when a major new challenge (if not a crisis) began to emerge: the return of inflation and changing consumer spending priorities. After a decade of almost uninterrupted growth, consumption of organic products experienced a sharp decline in several European countries starting in 2021, before beginning to stabilize in 2025. Our market research company has gathered the key figures, analyzed trends by distribution channel and country, and provides a rigorous overview of the organic sector, from production to consumption.

Contact the IntoTheMinds institute

Key takeaways

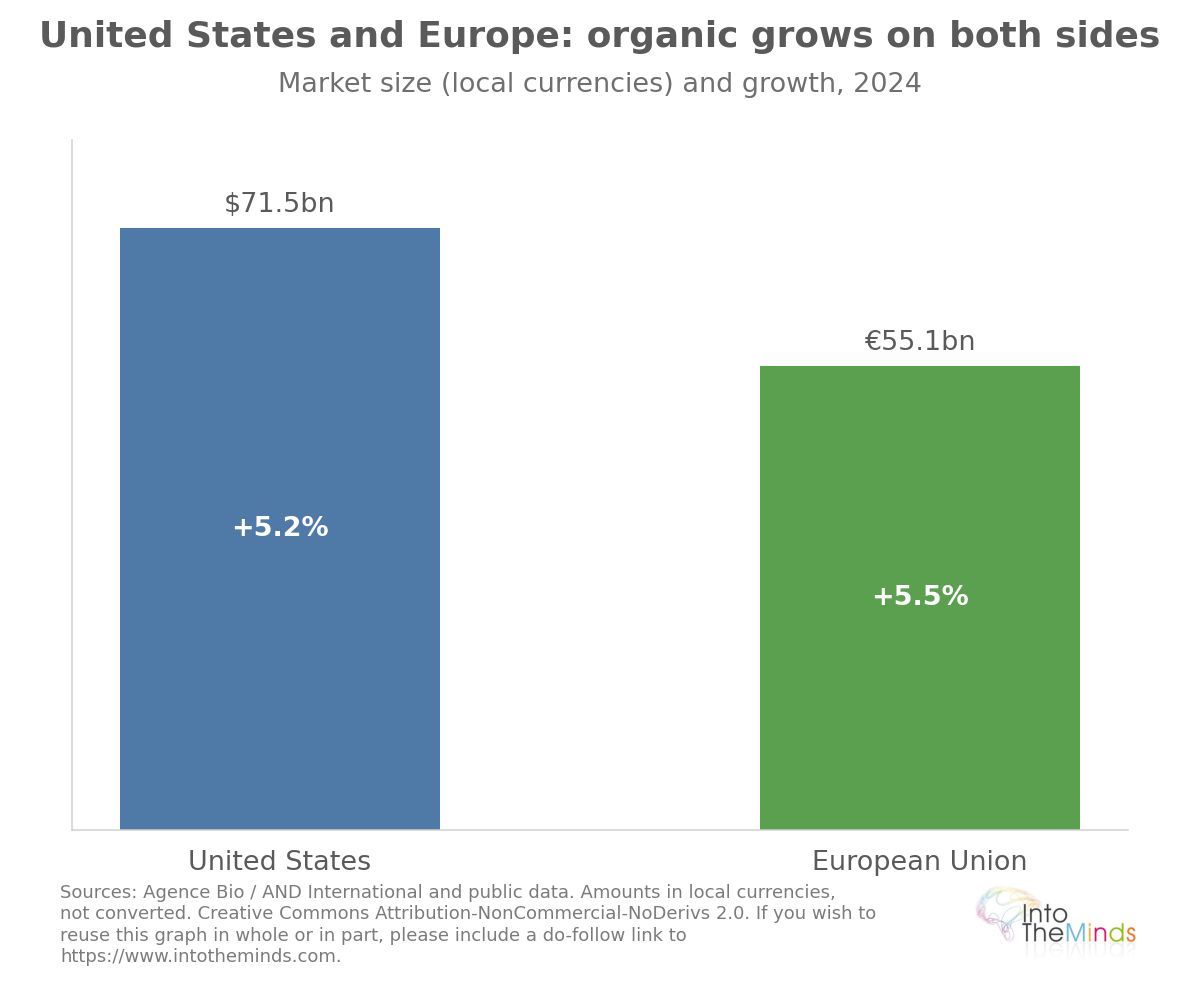

- In the United States, the organic market continues to grow and reach record levels, confirming its position as the world’s leading organic market, far ahead of the European market as a whole.

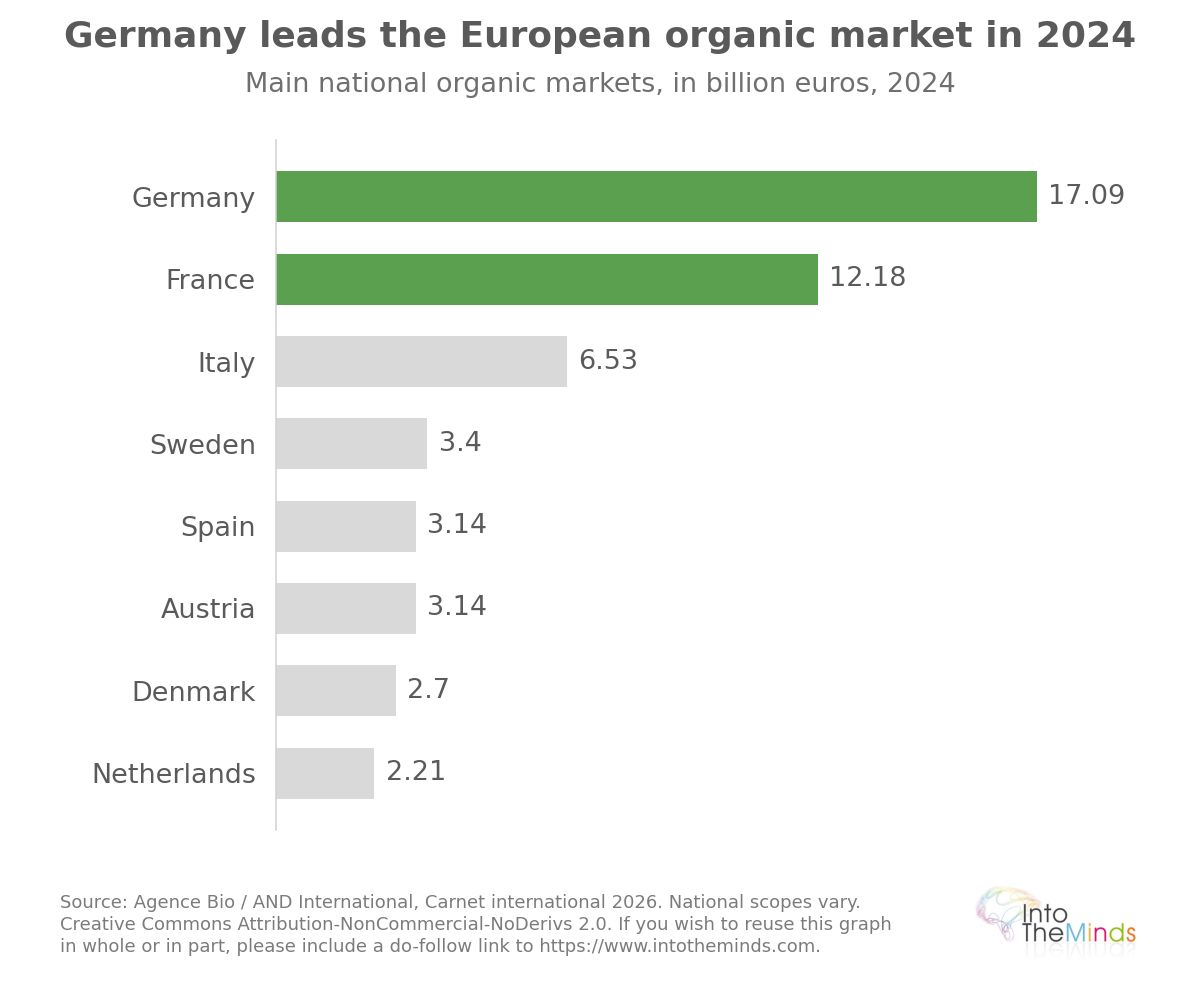

- The European Union organic market is worth €55.1 billion. It continues to grow overall despite major national disparities. Germany and France alone account for 55% of the European Union organic market.

- Germany is Europe’s leading organic market, with €17.09 billion in 2024.

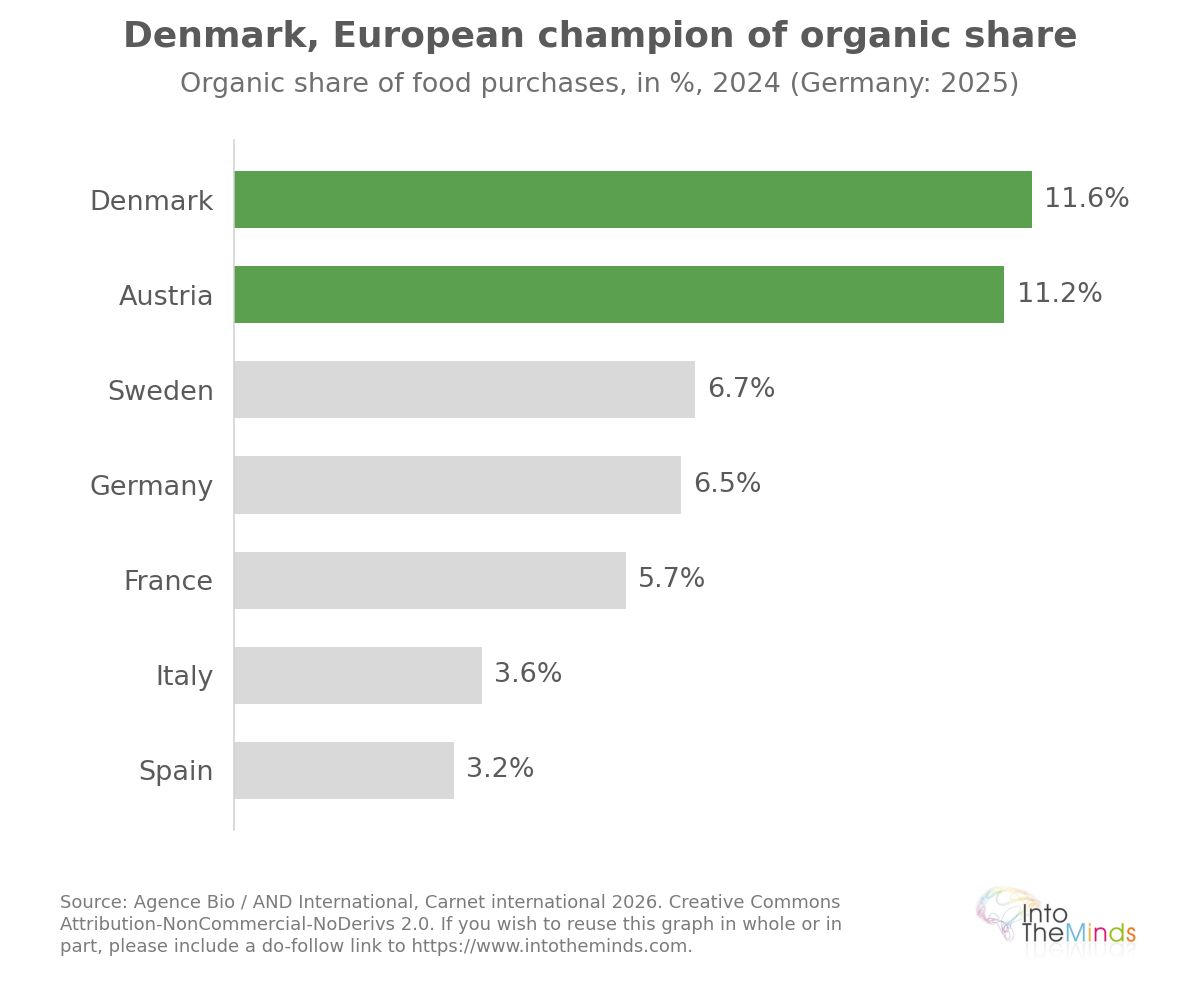

- Denmark recorded the highest share of organic products in food purchases in Europe in 2024, at 11.6%, ahead of Austria (11.2%).

- In France, at-home organic consumption reached €12.176 billion in 2024, up +0.8% in value but down -1.1% in volume, after four consecutive years of decline.

- French mass retail lost around 10 percentage points of market share in 4 years. It represented 55% of organic product sales in 2020 and 45% in 2024.

- The share of organic products in retail food sales in France fell from 6.6% in 2021 to 5.7% in 2024.

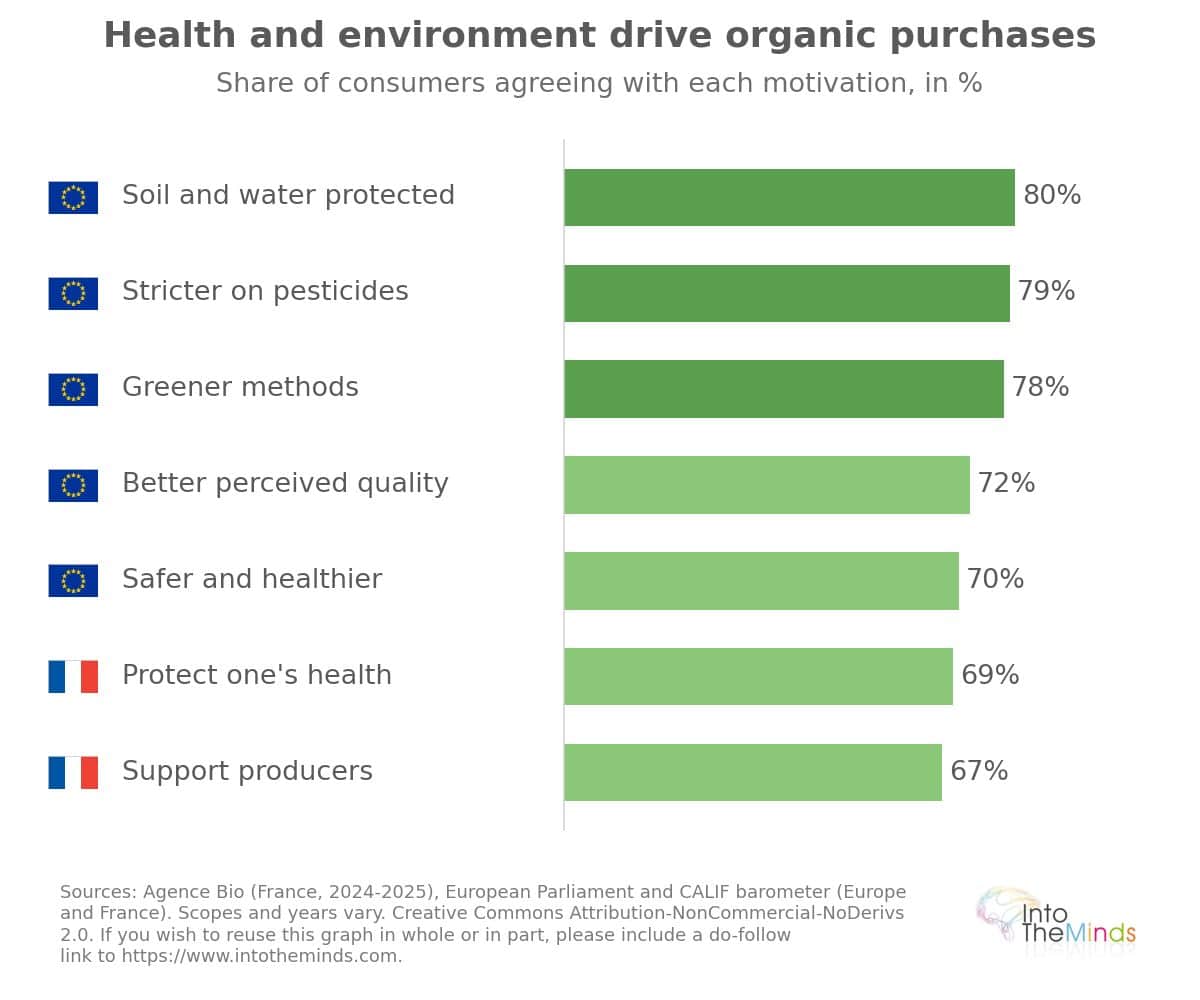

- 81% of Europeans believed in 2025 that organic products rely on better environmental practices and offer superior quality.

- An organic product costs on average 30% more than its conventional equivalent.

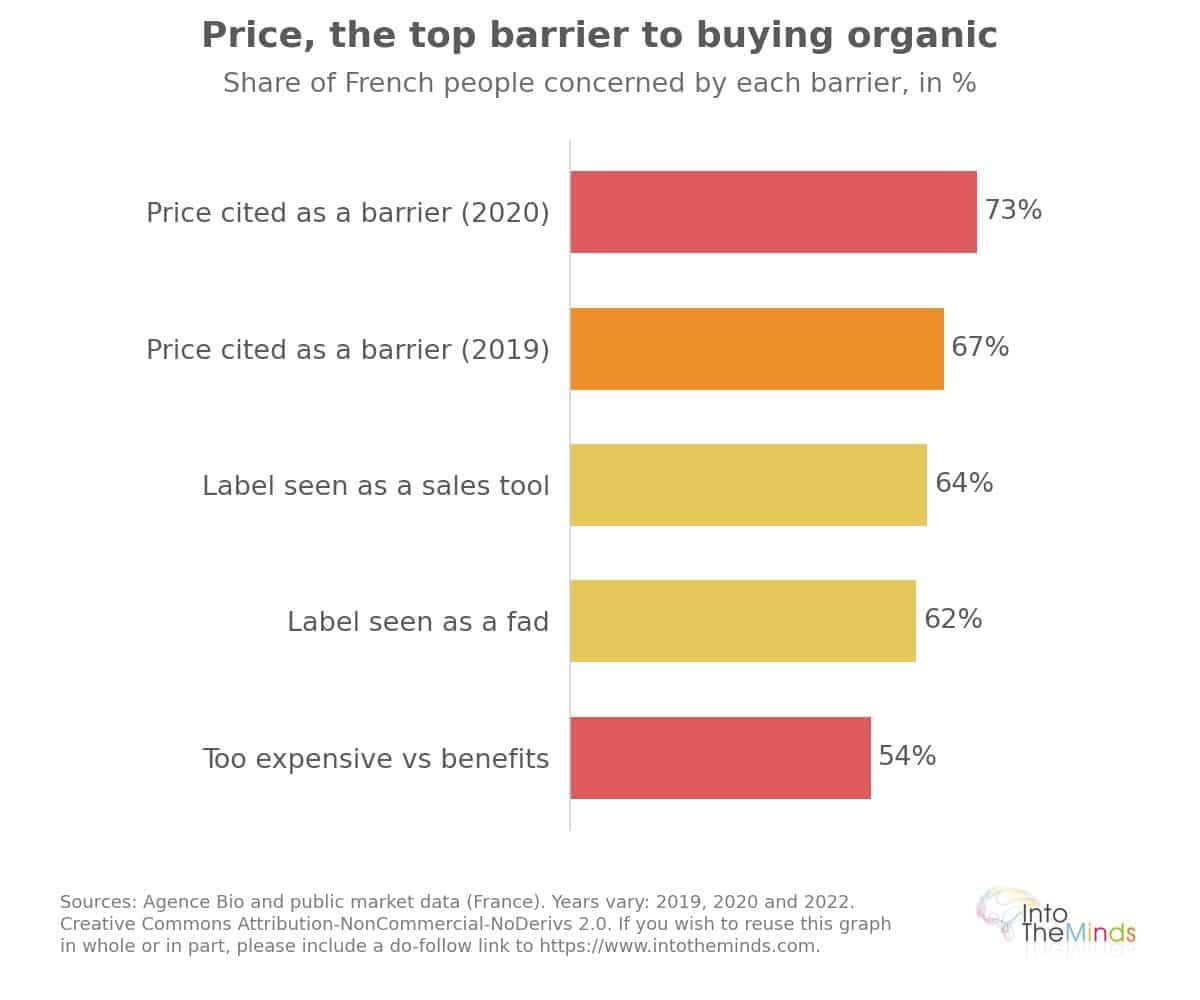

- The price of organic products is cited as a barrier to purchase by 73% of consumers.

- 54% of French consumers considered organic products too expensive relative to their benefits (2022).

The organic market in Europe and worldwide

The European Union: a €55 billion market

The EU organic market was estimated at €55.1 billion in 2024, up +5.5% compared with 2023, after having grown 2.3-fold over ten years. Organic farmland reached nearly 18.1 million hectares in 2024 (+0.6%), representing 11.1% of the EU’s utilised agricultural area, across more than 438,000 farms.

| Country | Organic market 2024 | 2023–2024 change | Organic share of food market |

|---|---|---|---|

| Germany | €17.09 bn | +6.3% | 6.5% (2025) |

| France | €12.176 bn (at-home consumption) | +0.8% | 5.7% |

| Italy | €6.526 bn | +5.7% | 3.6% |

| Austria | €3.139 bn | +6% | 11.2% |

| Sweden | €3.4 bn | -1.5% | 6.7% |

| Spain | €3.143 bn | +3% | 3.2% |

| Denmark | €2.7 bn | +3.5% | 11.6% |

| Netherlands | €2.205 bn | +11.3% | not available |

The Danes appear to be the most convinced and committed organic consumers. Denmark recorded the highest organic share of food purchases in Europe in 2024, at 11.6%, ahead of Austria (11.2%). Austria also stands out for having the highest share of organic farmland in the EU, at 27.2% in 2024.

By contrast, Spain—Europe’s leading country in terms of total organic farmland (2.945 million hectares)—allocated only 3.2% of its food purchases to organic products, reflecting an export-oriented specialisation rather than strong domestic consumption.

A global market dominated by the United States

Globally, organic farmland amounted to 98.9 million hectares in 2023, up +2.6% compared with 2022. Latin America recorded the strongest annual growth, with one million additional hectares (+10.8%). Oceania accounted for more than half of global organic farmland, although demand is concentrated elsewhere.

The United States is therefore the world’s largest market, with $71.5 billion in 2024, up +5.2%, and projected to reach around $100 billion within a decade. This figure far exceeds the entire EU market (€55.1 billion), confirming North America’s central role in global organic consumption. Ironically, the US is often associated with junk food (which benefits sellers of anti-obesity drugs) while also being the world’s largest organic market.

Key players and market dynamics

Let us now look at distribution channels. Each channel has followed its own trajectory since the 2020 peak, and it is worth noting that organic food has long been a specialist-driven market.

The driving role of organic stores

Specialist organic retailers went through a severe restructuring phase between 2022 and 2023, with closures of unprofitable stores and several bankruptcies. However, they returned to growth in 2025. The main players recorded growth of around +7% to +8%. In 2020, at the market peak, the leading French specialist network generated €1.62 billion (+16.6%) across around 700 stores, while the leading integrated chain reported €395 million (+22.4%) with 224 stores.

This rebound is partly explained by a spillover effect: consumers disappointed by reduced organic assortments in mass retail shifted toward specialised channels, which offer a broader and more consistent range.

The revival of organic in mass retail

Still focusing on France, mass retail remains the main distribution channel for organic products. However, its market share is eroding. The decline since 2021 is due to three concurrent factors:

- reduction in organic product ranges on shelves (Streamlining movement)

- price pressure, leading retailers to prioritise conventional private-label products

- competition from alternative positioning products (pesticide-free, free-range, local) capturing part of demand.

One example illustrates this tension: in 2022, 12% of losses in organic eggs came from a shift toward free-range eggs, a category that does not carry the AB label but meets part of consumer expectations. Since June 2025, organic sales in mass retail have returned to positive growth. This was an encouraging signal for the sector, but inflationary pressures are approaching again, bringing renewed consumer trade-offs toward cheaper products (as in 2022).

Direct sales and short supply chains

Direct sales have shown steady growth throughout the period, driven by demand for local products and direct producer–consumer relationships. In France, they represented around €1.5 billion in 2022, i.e. a doubling over ten years, with +4% growth between 2021 and 2022 even as other channels declined.

After the first lockdown in 2020, nearly one in ten organic consumers stopped buying organic in supermarkets in favour of local producers and farm-gate sales. In 2020, 59% of French consumers said they prioritised local products and short supply chains (+5 points year-on-year), and 57% preferred seasonal products. This structural preference for local has permanently strengthened direct sales as a complementary channel in the organic market. However, shortages in supermarkets may have mechanically forced consumers to switch to other distribution channels.

Organic consumer behaviour

Understanding organic market dynamics requires a deep analysis of consumer motivations, profiles, and barriers. Data collected through numerous surveys helps break down these behaviours.

Who are organic consumers?

Continuing with the French market, organic penetration reached 97.6% in 2019, 98.3% in 2020, and 98.6% in 2022: virtually all French households purchased at least one organic product during the year. However, purchase frequency and volume vary significantly across consumer segments.

Highly regular consumers accounted for 32% of the French population and generated 63% of organic food revenue. These committed buyers were the first to reduce purchases during the inflation crisis of 2022–2023. The decline then spread to upper-middle-class households, which accounted for 47% of the contraction observed in 2023.

Historically, the first organic consumers are affluent households with children and affluent retirees, representing 50% of organic purchases according to European data. Low-income households with children are the smallest buyer group.

Purchase motivations: health, environment and wellbeing

Consumer motivations for organic products remain stable over time and revolve around two main axes:

- Personal health: in 2024, 63% of French people were concerned about the health impact of food (source: Agence Bio), and 69% cited health protection as their main reason for buying organic.

- The environment: 80% of French people believed in 2025 that organic farming helps preserve soil and water quality (Agence Bio Barometer, 2025).

- Perceived quality: according to European Parliament data, 72% of European consumers believe organic products are of higher quality, and 70% consider them safer and healthier.

- Agricultural practices: 79% of European consumers believe organic production is more restrictive in pesticide and antibiotic use, and 78% see it as more environmentally friendly.

- Willingness to support producers: 67% of French consumers said they were willing to pay more for food products with a positive impact on French agriculture (2025).

Barriers to organic adoption

Price remains the main barrier. An organic product costs on average 30% more than its conventional equivalent, and up to 54% more according to some estimates. In 2022, 54% of French people considered organic products too expensive relative to their benefits, and 67% cited price as a barrier in 2019, rising to 73% in 2020.

The trust crisis around labels has worsened the situation. In autumn 2022, 55% of respondents considered it not very important or unimportant for a product to carry an organic label, 62% saw it as a trend, and 64% as a marketing tool. Yet 94% of French people knew the AB logo in 2021 and 91% trusted it, suggesting that the issue is not awareness but perceived value under budget constraints.

Competing claims (pesticide-free, free-range, local, preservative-free) have also fragmented demand by offering partially substitutable promises at lower prices.

Organic value chains in detail

Market analysis becomes more precise when broken down by product category. Dynamics vary significantly across segments.

Organic fruit and vegetables

Fruit and vegetables are the flagship category of organic consumption. In Europe, 40% of organic spending is on fruit and vegetables. In Belgium and across Europe, this category leads by a wide margin, ahead of meat, fish, dairy, bread and cereals.

In the first half of 2025, organic fruit and vegetables emerged as a key driver of market recovery in France, accounting for one-third of household organic spending on fresh traditional produce. This category benefits from strong habitual purchasing and high in-store visibility, making it a natural lever for consumers returning to organic.

Organic dairy products and meat

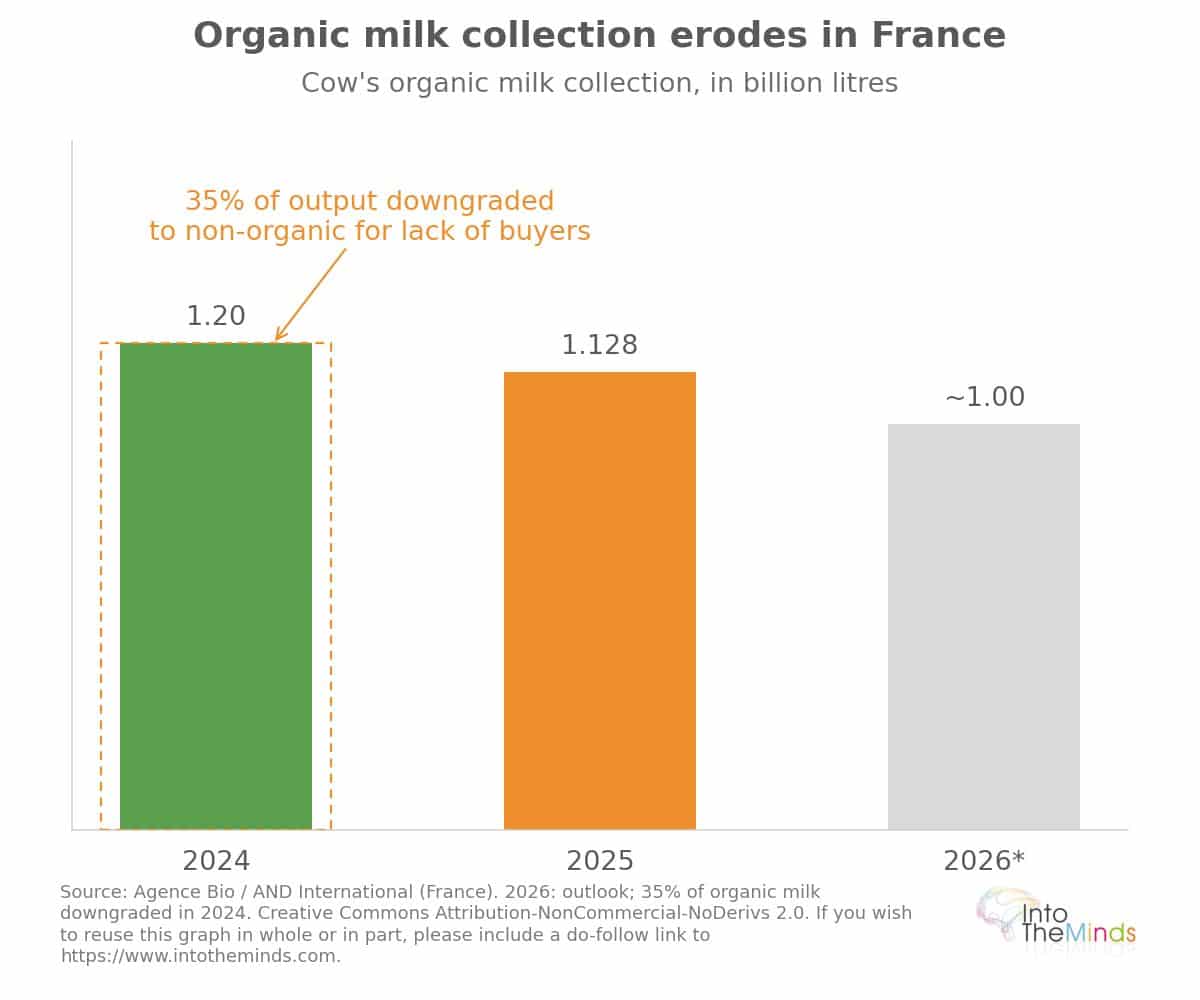

The French organic dairy sector illustrates structural tensions in production. Organic cow’s milk collection declined by -3.9% in 2024 (around 1.2 billion litres), then fell to 1.128 billion litres in 2025, with a projection of around 1 billion litres in 2026, i.e. less than 5% of national milk collection. In 2024, 35% of organic milk was downgraded, meaning it was sold without the organic premium at conventional prices because no buyers were found. The average price paid to French producers for 1,000 litres of organic milk was €519.79 in 2024.

In 2023, eggs, yoghurt and long-life milk were among the nine categories accounting for one-third of organic market losses. The shift from organic eggs to free-range eggs represented 12% of losses in this category, illustrating the permeability between different quality claims.

Out-of-home catering and organic

Out-of-home catering remains a relatively small but growing channel. In France, it represented €640 million in 2019 and €505 million in 2020, a year heavily impacted by lockdown closures (-21%). This channel has since recovered to exceed €600 million again, with collective catering (school canteens, hospitals) subject to regulatory obligations to source organic and local products.

At European level, the Agence Bio publishes each year a specific barometer on out-of-home catering, which tracks the integration of organic products into collective and commercial food service channels, a segment that industry stakeholders consider a structural growth driver for the years ahead.

Key figures of the organic market in France

To understand the current state of the organic sector, it is necessary to distinguish global dynamics from national trajectories, which follow very different logics. Data from Agence Bio and reports published in 2025 provide a precise overview of the situation.

Size and growth of the French organic sector

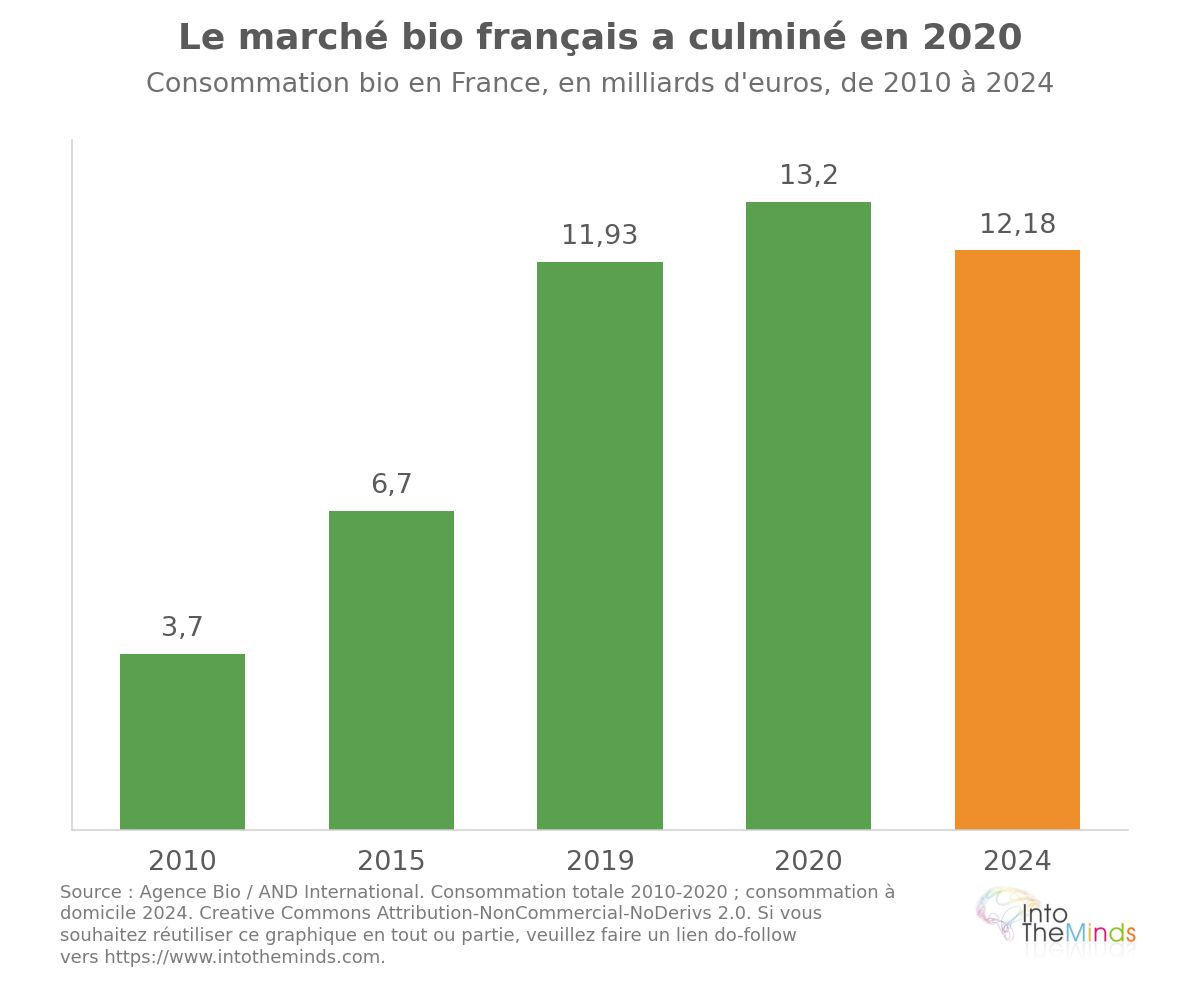

In France, organic consumption (household purchases and out-of-home catering) reached a historic peak of €13.2 billion in 2020, compared with €6.7 billion in 2015 and €3.7 billion in 2010. This level then declined every year until 2024, when at-home consumption stood at €12.176 billion, up only +0.8% in value but down -1.1% in volume compared with 2023. Including out-of-home catering, the market exceeded €13 billion in 2024 (+1.0%), while remaining below its 2020 and 2021 levels.

The share of organic products in French retail food sales stabilized at 5.7% in 2024, compared with 6.6% in 2021. This erosion of nearly one percentage point over three years illustrates the scale of the sector’s downturn.

On the agricultural side, France had 2.711 million hectares of organic farmland in 2024, representing 10.2% of its usable agricultural area. According to Agence Bio data, the country ranked second in Europe for organic farmland, behind Spain (2.945 million hectares) and ahead of Italy (2.515 million hectares).

Evolution of French organic consumption

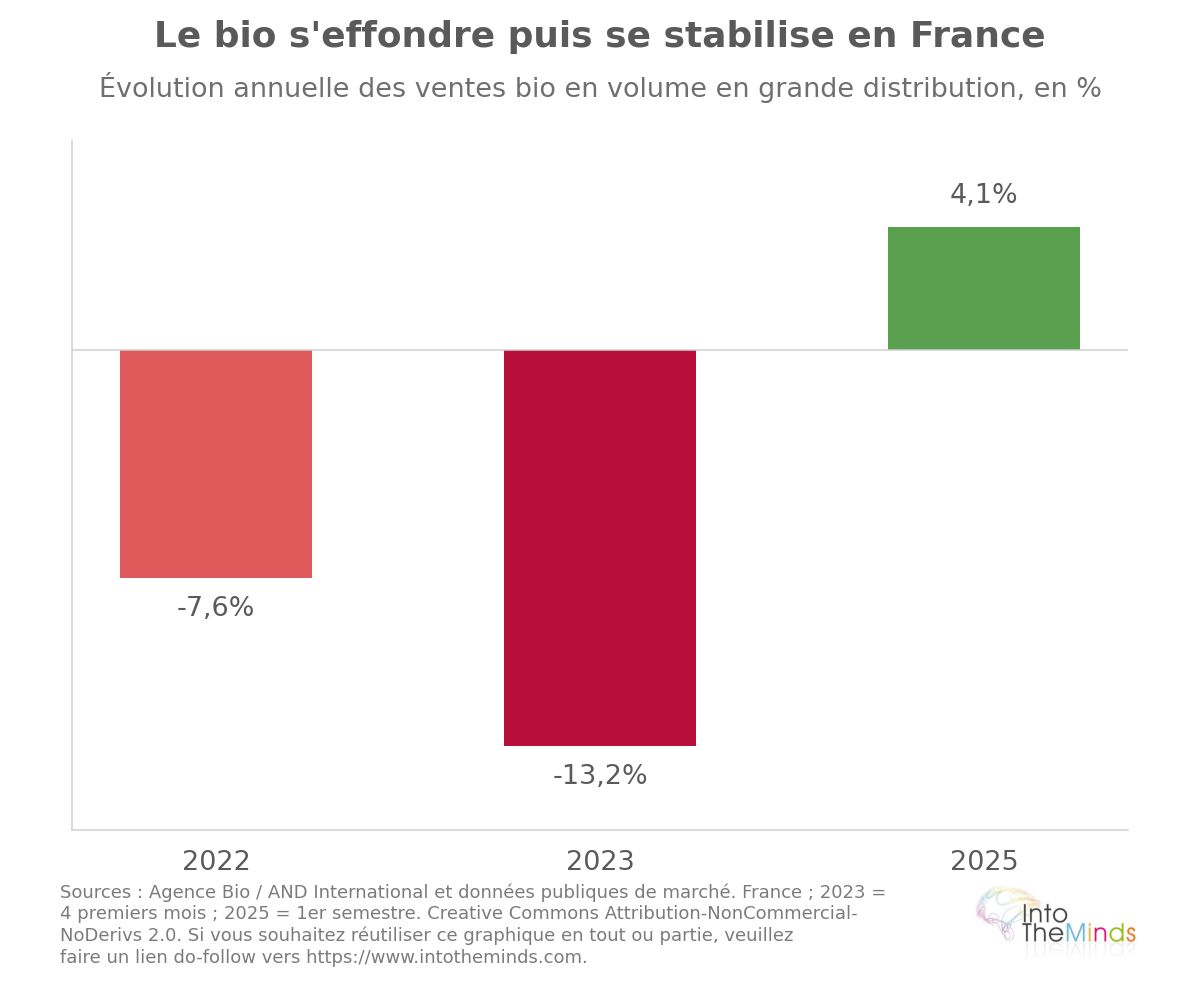

The turning point emerged gradually. From the second half of 2020, growth in mass retail began to slow. The real inflection point occurred in February 2021: from that moment onward, organic sales in supermarkets declined every month. In October 2021, the drop reached -9.7% in value and -9.2% in volume.

The deterioration accelerated under the effect of food inflation. In 2022, organic sales fell by -7.6% in volume (compared with -2.2% for conventional products). At the beginning of 2023, the decline reached -13.2% over the first four months of the year, in a context of +17% inflation on organic products in supermarkets in May 2023. In 2023, 80% of organic categories recorded a decline, and the crisis had erased four years of growth.

Signs of recovery emerged from 2025 onwards. In the first half of 2025, the market grew by +4.1% compared with the first half of 2024, with a market share stabilizing at 4.1% on a cumulative annual basis in summer 2025. This is the first period of stability recorded since the downturn that began in 2020.

Distribution channel data

The structure of sales channels changed significantly between 2020 and 2024.

| Distribution channel | Organic market share France 2020 | Organic market share France 2024 | Change |

|---|---|---|---|

| Mass retail | 55% | 45% | -10 points |

| Specialized retail | 29% | 27% | -2 points |

| Direct sales | 11% | 13% | +2 points |

| Artisan-retailers | 6% | 9% | +3 points |

Mass retail therefore lost around ten points in four years. In 2024, sales of specialized organic stores increased by +5.3%, while organic sales in mass retail still declined by -4.4% at constant weighting. Direct sales, which represented around €1.5 billion in 2022 (or 13% of the organic food market), have doubled over ten years.

In the short term (this year), we believe the organic sector risks experiencing a shock resulting from the inflation crisis triggered by the closure of the Strait of Hormuz.

Outlook and future challenges of the organic sector

The French Ministry of Agriculture’s Centre for Studies and Strategic Foresight published in April 2025 a study titled “What future for the French organic sector by 2040?”, conducted by consultancy firms Ceresco and Crédoc. It identifies four contrasting scenarios for 2040, built around 20 key variables.

Scenarios for evolution towards 2040

The four scenarios do not aim to predict the future but to explore plausible futures.

- Scenario 1: organic not prioritized. Economic growth takes precedence over environmental concerns. Organic products disappear from mass retail shelves and refocus on an affluent and loyal customer base, before regaining interest from 2030 onwards due to strategic resource crises and climate shocks.

- Scenario 2: organic marginalized by a “third way”. Other agricultural approaches promising environmental benefits (no pesticides, non-certified agroecology) gain ground and capture demand at the expense of the organic label. Price works in favor of these alternative approaches.

- Scenario 3: “lightened” and widespread organic. A less stringent organic standard becomes widespread, increasing volumes but diluting the value of the label.

- Scenario 4: dominant organic. Public policies and consumer behavior converge toward predominantly organic agriculture and food systems.

Three factors are decisive for the future of the sector:

- the price of organic products

- the perception of labels

- expected benefits (health and environment)

These three variables determine the sector’s ability to attract new consumers and retain existing buyers. In the short term (this year), we believe the organic sector risks experiencing a shock resulting from the inflation crisis triggered by the closure of the Strait of Hormuz. This is a scenario already tested in 2022, which caused major disruptions in the sector. Remember that price is the number one adjustment factor, and household budgets are not elastic.

Durability and competitiveness challenges

Upstream in the value chain, the situation of French organic farmers remains fragile. According to the 2025 organic farmers’ barometer, 82% were satisfied with their commitment and 93% proud to farm organically, but only 23% were optimistic about the sector’s future, compared with 40% who were pessimistic. Economic fragility is real: 35% of farms generated an annual gross income below €5,000, and 57% of farmers reported dissatisfaction with their income.

Expectations focused primarily on fair prices (94% of respondents), stronger communication (92%), and increased financial support (89%). The average size of French organic farms was 43 hectares in 2025, with an average farmer age of 48.6 years. A more encouraging signal at European level: 20.7% of organic farmers were under 40 in 2024, compared with 11.9% across all farms, indicating stronger generational renewal than average.

Organic as a response to tomorrow’s food challenges

Despite cyclical difficulties, underlying support for organic principles remains high. In 2025, 81% of Europeans believed that organic agriculture is based on better environmental practices and delivers higher quality products. This shared conviction, which persists despite declining sales in several markets, suggests that recent difficulties are driven more by short-term economic trade-offs than by a lasting rejection of the model.

The issue of reducing plant protection products and preserving biodiversity remains central to long-term food challenges. Organic farming, which prohibits GMOs, synthetic fertilizers, pesticides, and chemical herbicides, offers a coherent response to these issues. The sector’s ability to make this response accessible to a broader audience—particularly by narrowing the price gap with conventional products—will largely determine its trajectory toward 2040. Agence Bio publishes a detailed annual assessment report on the organic market, which serves as the official French reference for tracking these developments.

FAQ: Questions you may have

What is the size of the organic market in France in 2024?

In France, at-home organic consumption amounted to €12.176 billion in 2024, up +0.8% in value but down -1.1% in volume compared to 2023. Including out-of-home catering, the market exceeded €13 billion. The share of organic products in retail food sales stabilized at 5.7%, compared to 6.6% in 2021. For an in-depth analysis of the organic market among consumers, IntoTheMinds offers market research tailored to food industry players.

Why did the organic market decline between 2021 and 2024?

The decline of the French organic market is due to several cumulative factors: food inflation (organic products cost on average 30% more than conventional equivalents, with +17% inflation for organic products in supermarkets in May 2023), erosion of the perceived value of the AB label (55% of French consumers considered it unimportant in autumn 2022), and competition from alternative claims such as “pesticide-free” or “free-range”. The two main buyer profiles, representing 63% of organic turnover, were the first to reduce their purchases. To understand consumer perceptions of a product or label, brand awareness studies can provide precise insights.

Where do the French buy organic products?

In 2024, mass retail still accounted for 45% of organic sales to households in France, down from 55% in 2020. Specialized organic stores accounted for 27%, direct sales for 13%, and artisans/retailers for 9%. Mass retail lost around 10 percentage points of market share in four years, in favor of local channels and direct sales. In 2020, online organic sales (click & collect and e-commerce) represented around €938 million, with organic products accounting for 8.6% of FMCG e-commerce sales.

What is the situation of the organic market in Europe?

The European Union organic market reached €55.1 billion in 2024 (+5.5%), with 18.1 million hectares of organic farmland (11.1% of usable agricultural area). Germany and France accounted for 55% of European consumption in value. Denmark had the highest share of organic food purchases (11.6%), ahead of Austria (11.2%). Spain led in absolute organic farmland (2.945 million hectares). National trajectories differ significantly: the Netherlands grew by +11.3% in 2024 while Sweden declined by -1.5%.

How to conduct a market study on the organic sector?

A market study on the organic sector requires combining several approaches: analysis of secondary data (Agence Bio reports, Agreste data, European statistics), quantitative surveys of consumers to measure behaviors and perceptions, and qualitative analysis to understand purchasing motivations and barriers. Depending on whether the target is retail, production, or processing actors, methods differ. IntoTheMinds conducts B2C market studies and B2B studies for food industry players in France, Belgium, and Luxembourg.

What are the prospects for the organic market towards 2040?

The foresight study published in April 2025 by the French Ministry of Agriculture’s Center for Studies and Prospective identifies four contrasting scenarios for 2040, ranging from a marginalized organic sector to a dominant one in food systems. The three key drivers are organic product prices, label perception, and expected benefits. In the first half of 2025, the French market grew by +4.1% compared to the first half of 2024, marking an initial sign of recovery after four years of decline. Opinion surveys help continuously track changes in consumer perceptions of organic products.