What will remain of the world after the Covid-19 tsunami? Changes in behaviour and the disappearance of companies are the most obvious consequences. In this dossier, we analyse 11 scenarios, their risks but also their solutions.

Summary

- The public debt

- Central banks and liquidity injections

- Medical and scientific research

- Relation to work

- Online commerce

- Electric cars and mobility

- Entertainment and events

- Travel and tourism

- STrade fairs

- Distance learning

- Technological innovation

Introduction

But what is also certain is that the economic imbalances that are already quite visible will be even more so tomorrow and will probably even be accentuated. The injections of liquidity by central banks will create new speculative bubbles, while the public debt will increase, especially in countries already in difficulty such as Italy and Greece. In political and social terms, the post-COVID-19 period could prove to be a real time-bomb. Remote working has become the rule in all sectors and raises questions about the future of relations between employees and employers. Will remote working become the norm, and what other implications will this have? What will become of business travel, air travel, evenings out at the movies or restaurants? Will the Western lifestyle, based on entertainment and leisure, be challenged? What will become of the tourism, catering and events sectors which, by the very nature of their activities, involve concentrating populations and limiting social distancing?

The public debt

Expansionary fiscal policies by governments will lead to an increase in public debt in all countries. We are witnessing an escalation of stimulus packages into hundreds of billions of Euros. All European countries will have to find growth relays to make the prospect of perpetual debt somewhat credible. At the very least, GDP will have to be increased enough to repay interest without generating more debt. Otherwise, it could be a disaster that could end as it did for the countries of southern Europe in 2011 when the “spread” increased and investors having to refinance maturing debt demanded high-interest rates. This forced market GDP growth could result in drastic measures such as extreme labour flexibility and job insecurity. GDP growth in the United States has thus been built up since the Reagan era, thanks to the impoverishment of manual workers. It should also be remembered that the post-crisis chaos of 1929 gave birth to the totalitarian and autarchic regimes that ravaged the world. Fortunately, central banks now know how to manage a crisis (this was not the case for the American central bank in 1929) and the governments in power are enjoying a revival of confidence (Italy, Germany) which makes nationalist parties inaudible.

Risks

- the impoverishment of the working class through the deconstruction of the social model, searching for growth at all costs

Solutions

- GDP growth to absorb excess debt

- suppression of cash to asphyxiate the underground economy

- the removal of tax havens

- GAFA tax

- flat tax

Central banks and liquidity injections

As in the 2008 financial crisis, central banks will inject liquidity into the system in an attempt to stem the global economic downturn. This is a Keynesian recovery, and everyone agrees that this is the right solution. The low cost of money (zero or even negative interest rates) facilitates this injection (also called “helicopter money”). But let’s make no mistake about it: this is money creation. There is nothing in front of this newly printed currency, whether it is denominated in dollars, euros or any other currency.

But while central bank action can help keep markets afloat, for the time being, its effectiveness will be limited for the economic crisis looming on the horizon. Zero or negative interest rates do not automatically revive tourism, nor the reopening of restaurants, nor the revival of the industrial chain. It takes a shock in consumer confidence for that to happen. On the other hand, these massive injections of liquidity, these free loans, in short, will contribute to the formation of probable speculative bubbles. Ironically, it is the markets that benefit from government largesse that will bet against them. What a paradox! Governments offer money to markets that, unregulated, will use it to make short-term profits and precipitate the downfall of lenders (the States).

Risks

- loans to companies already in bad shape and loss of capital (bad debt)

- speculative bubble formation

Solutions

- Keynesian stimulus through liquidity injections (secured loans)

- Diffrentiated loan granting procedures (exclusion of companies with accounts in tax havens or using complex arrangements such as the Dutch sandwich, priority to local companies and relocation of strategic production)

Investments in medical and scientific research

“All evil is good” as the saying goes. One of the positive consequences of the Covid-19 crisis concerns investment in medical research and digital developments. This crisis will also have revealed that it is possible to work fast by joining forces. Never in the history of research has progress been made so quickly by so many researchers simultaneously.

The research that will be carried out in the coming months will also make it possible to reinvent safety at work, in shops and cinemas. The few concepts that are emerging are for the moment practical, short-term solutions to a series of problems that are still poorly understood. But from 2021 onwards, more sophisticated solutions will appear that will offer new functionalities in addition to protecting us from viruses.

Risks

- the privatisation of research and capture of profits, for the benefit of private firms (confiscation of the common good)

Solutions

- the homogenisation of legislation on clinical trials (the European directive has not been translated into national law)

- abolition of the paid access model for scientific articles

- relaunching scientific research by allocating extraordinary budgets

New workplace relationships

The health emergency has forced many people to work remotely. Even the countries lagging furthest behind in telework have been moving at breakneck speed.

The world of work after COVID-19 will, therefore, no longer be the same. The question on everyone’s mind is: “Will technology allow us to stay at home? As we have seen, office work, whether private or public, can be done at home without too much difficulty. It took a severe crisis to realise this and change attitudes.

3 essential rules need to be respected to make working remotely possible:

- high-quality network infrastructure and fast internet access for every employee

- good digital culture for all employees and autonomy with IT tools

- a thoughtful and systematic organisation of teleworking. The trust factor is crucial to making teleworking a success. If there is a lack of trust between the employer and the employee, between the manager and the rest of the team, if objectives cannot be evaluated very regularly, the whole system will collapse.

Risks

- lack of human interaction reduces the potential for innovation and creativity.

- loss of control and motivation

Solutions

- a hybrid model where some tasks are done at home (2-3 days a week) and projects involving innovation work are done with the rest of the team.

A breakthrough in e-commerce

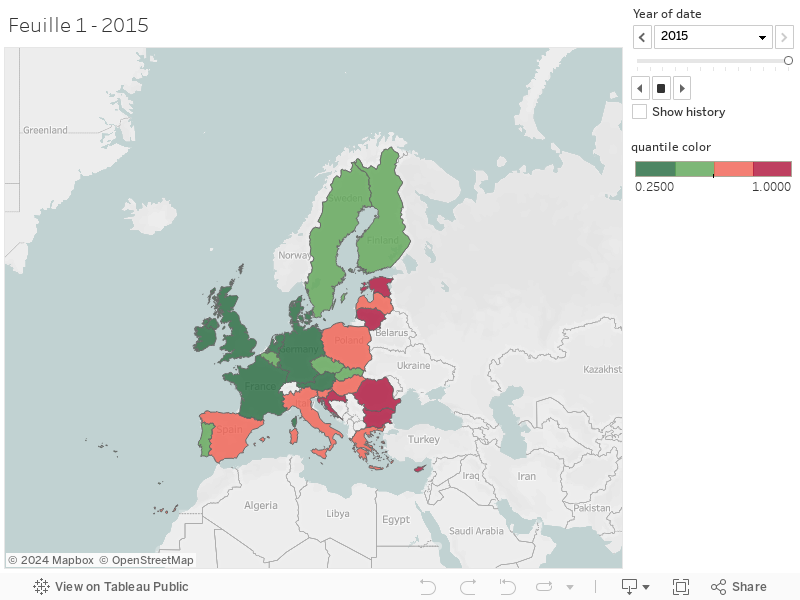

Coronavirus promotes e-commerce. It could, therefore, become a powerful ally in the fight of governments against the underground economy. Electronic trade cannot be tax-exempt. The sums lost by governments due to the underground economy could, therefore, be partly offset. This would simplify the repayment of the newly created public debt. If the consequences of the pandemic confirm the changes in purchasing habits, the use of credit cards to the detriment of cash will become an engine of transition towards a more virtuous economy where fraudsters would find it harder to prosper. To find out where this virtue is lacking, you can use the map below, which shows the countries of Western Europe according to their degree of the underground economy.

The growth of electronic payments will create new jobs in website construction and secure online payment methods. However, there are drawbacks to moving to an “all-electronic” world. While the development of e-commerce now seems to be indispensable (see our analyses on food retail and non-food retail), buying in virtual shop windows will contribute to ever-increasing desertification of territorial areas. The most fragile shops will close. Only food shops and those with an emphatic “advice” dimension (opticians, car dealers, and so on) will remain. The threat to window shopping will remain very present, forcing retailers to redouble their efforts to build customer loyalty and turn to phygital models.

Risks

- The investment in an e-commerce site proves to be unprofitable. The infrastructure is not sufficient to generate online sales, and the owner does not master the digital world enough to promote his services and products.

Solutions

- In addition to subsidies for technological investments, it is essential to train traders in digital technology. The next 2 years will be ruthless for those who do not master the digital codes.

Electric cars abandoned; industry redesigned

Car factories have closed all over Europe. Dealers closed for almost 2 months. New registrations have collapsed (see statistics here). The Covid-19 pandemic is also reshuffling the maps of the car industry from an industrial point of view. Regional macro-zones capable of covering the entire component supply chain can be expected to form. This reorganisation of the supply chain will impact all products, whether finished or semi-finished, as well as raw materials.

The collapse of oil prices will slow down the penetration of electric cars. More expensive, they will also be abandoned as a result of the decline in purchasing power. Public transport, which is being ignored, will lead motorists to prefer to travel with their vehicles. The existing car fleet will, therefore, continue to age in the absence of new registrations.

Risks

- Ageing of the carpool

- Use of public transport declining due to fear of the virus and road congestion

Solutions

- Consultation between employers and employees. For transportation programs coordinated with teleworking schedules.

Entertainment and special events at risk

The travel and entertainment sectors are likely to be subject to significant change. Some companies active in these sectors will not be able to resist them and will close their doors. The devastation has already begun.

Activity in these sectors involves concentrations of customers that are currently incompatible with the sanitary requirements. Reinventing company agreements will, for example, be a challenge. The fashion industry, whose dynamics are driven by fashion shows, will also be affected. Can Karl Lagerfeld’s magnificent fashion shows still exist in the post-COVID-19 era?

The world of entertainment will have to operate with reduced capacities, with halls that are half-empty for many months, forcing the rehearsal of shows to satisfy as many people as possible. Solutions will have to be found to cut operating costs by 50% so as not to have to increase ticket prices. For example, we can imagine that there will be more cinema presentations to make the infrastructure profitable, that the shortest shows (theatre, concerts) will subsequently be without intermission and that several performances will be held in the afternoon and evening.

The situation for museums and exhibitions is more contrasted. A distinction must be made between hyper-museums and their collections of world-wide scope, and all other museum places. For the latter, which are already accustomed to lower attendance, it will just be a matter of regulating and smoothing out the entries. For the former (Vatican, Louvre, MET, and so on), regulation will inevitably mean a loss of income. The record attendance at the Louvre, for example (10.2 million visitors in 2018) will not be reached any time soon. The drastic drop in intercontinental travel will sound the death knell for Asian and North American tourism in European capitals. High-end hotels will feel the pinch.

Risks

- Declining interest in large museums and increasing deficits due to limited admissions to reduce visitor density.

- structural impossibility of reaching break-even points for live performances because of social distancing rules

Solutions

- in addition to booking schedules, booking routes to avoid crowds at critical locations

- longer opening hours to spread out the visits (already practised for extensive exhibitions)

- Increase in the number of performances of the same live show on the same day

- subsidising visits to local museums until the end of 2020 with “culture” vouchers

Travel and tourism: the revenge of the local

The world of tourism is likely to experience a deep crisis. Air transport will idle in 2020 and 2021 (see our detailed analysis here) and can only hope for a return to normality around 2022. Cruise ship passengers combine unfavourable elements and have been the object of real drama at sea during the epidemic. The adverse factors in this sector are:

- massive investments in larger and larger boats

- huge asset base

- huge maintenance costs even when the activity is at a standstill

- high customer concentration

- high fill rate required to reach the break-even point

This sector may never be able to recover from the crisis, and there is a real likelihood that these mega-ships will be grounded forever. The Venice lagoon will do very well without these day-trippers.

Tourism will likely become more local and more focused on the family cocoon. Travel will be less far away; country houses and second homes will be favoured. In a context of declining purchasing power, the mobile home rental sector could experience impressive growth because it combines flexibility, discovery and security.

Risks

- the disappearance of traditional and undifferentiated travel agencies

- cruise ship bankruptcies (giant ships) and job losses in shipyards

Solutions

- let cruise-lines operating oversized boats disappear (harmful to the environment and the cities visited)

- promote local and quality tourism

- impose taxes for long-distance air travel (>x hours)

The end of trade shows and fairs?

Until last February, trade fairs (B2B fairs) were considered central players in markets such as art, automobiles or technology (think of the Maastricht fair, the Geneva fair or the CES in Las Vegas). These fairs had experienced continuous expansion, only interrupted by internal dissent, as in the case of the Basel Watch Show. In March, the coronavirus brought an entire system to its knees. For some countries, such as Italy, the shock was severe. Italy is the 4th largest player in the world in terms of trade fairs. To measure the extent of the consequences, we need to give some figures. In Italy, trade fairs bring together 200,000 exhibitors and 20 million visitors every year, generate 60 billion euros in turnover and contribute 50% of the exports of the companies taking part. The SIAL food exhibition, held every two years, is a vital driving force in the food sector and brings together more than 6,000 exhibitors in Paris alone.

The question to be asked is: will trade shows still be possible in the post-COVID era? Will virtual exhibition spaces become the norm? We do not believe in the disappearance of B2B trade shows, nor their replacement by virtual events. According to our experience, the added value is far too low compared to what a “physical” trade fair brings. Let’s not talk here about the elements of body language, of negotiation, which are impossible to capture in a virtual space. Let’s focus on the possibility, during a trade show, of going around a market and its players in a short period. The trade show is a business accelerator, and for this reason, COVID will not have its skin. What seems clear to us, however, is that major international trade shows (NAB Las Vegas, CES Las Vegas, NRF New York, Mobile World Congress Barcelona, SIAL Paris) are impossible to hold for at least the next 6 months.

Risks

- the important trade fairs will not be able to be held for another 6 months.

- reduction of exhibition capacity and limitation of the number of exhibitors, leading to a decrease in attractiveness and innovation

Solutions

- digital solutions for preparing trade fairs and appointments (already widely available but not yet widely promoted)

- distribution of mega exhibitions over larger areas across a city or region

Remote teaching: beware of danger!

The closure of schools has created an unprecedented situation that has catapulted all teachers into the world of long-distance education. The world of education has suddenly changed. More accustomed to dealing with toilet paper shortages, it had to learn how to manage computer facilities overnight. It was a rude awakening in the 21st century. Unfortunately, the official education system, inadequately prepared, still doesn’t make it and the private actors, much better organised, are winning the day.

If technology improves traditional teaching, can it replace it? Long-distance education is not a solution to all problems. There are many risks: lack of interaction, dropping out, distractions, … “physical” teaching has the advantage that it places the student in a physical setting (the classroom) which forces him to concentrate. Let us not forget either that the cognitive capacities of the child are formed thanks to interactions and that at any age, the human being needs relationships with his peers to develop. One-way distance education does not provide a complete answer to all these challenges.

If distance education is to play a significant role in the future, a fundamental success factor will be personal control and monitoring. It is unthinkable to imagine that a 12-year-old student could be sufficiently disciplined to work in complete autonomy in front of a MOOC or any other form of remote course.

Risks

- replacing face-to-face learning with distance learning solutions

- loss of contact with some students

- lack of remote monitoring by the teachers

- Privatisation of education

Solutions

- serious and daily remote monitoring via teachers: use of videoconferencing so as not to lose the link with the pupil

Technological innovation and 5G out of order

Technology companies have not escaped the adverse effects of the Covid-19 crisis. Innovation has been slowed or even stopped by the paralysis of research centres. Sales have stalled after the closure of stores and sales targets for 2020 will not be met. Production lines (in China) have been affected, and their market launch will be delayed. The new iPhone 9 could thus arrive on the market much later than expected.

Optical fibres will also be strongly affected by the effects of the coronavirus. The shutdown in the city of Wuhan, where there is the largest concentration of suppliers in this sector (from Fiberhome to Accelink), has slowed production, could cause a domino effect even on 5G (demand for fibre for this technology is much higher than for 4G), which would, in turn, affect the production of 5G smartphones.

Risks

- delay in the deployment of 5G (due to China’s dependence^)

- lagging innovation cycle

Solutions

- the pooling of pan-European forces for the production of crucial elements for innovation

- relocation of strategic industries

Illustrations : shutterstock

![Illustration of our post "Pricing: strategies, techniques, examples [Guide 2025]"](/blog/app/uploads/pricing-120x90.jpg)