The cognac market has changed completely over the past 10 years. Exports are declining, geopolitical tensions are impacting sales, and alcohol is no longer popular among young people. In this article, I provide a comprehensive overview of the situation using the most recent figures.

The French spirits sector is going through a rather difficult period. The cognac market in particular is bearing the full brunt of geopolitical and trade tensions. This brandy, long a champion of exports and perceived overseas as a symbol of French excellence (it was popularized by rappers), is now in crisis. The decline in alcohol consumption among younger generations and the rise of the No/Low market are also likely contributing factors. In this article, our market research institute analyzes the cognac market based on the most recent data available.

Key takeaways

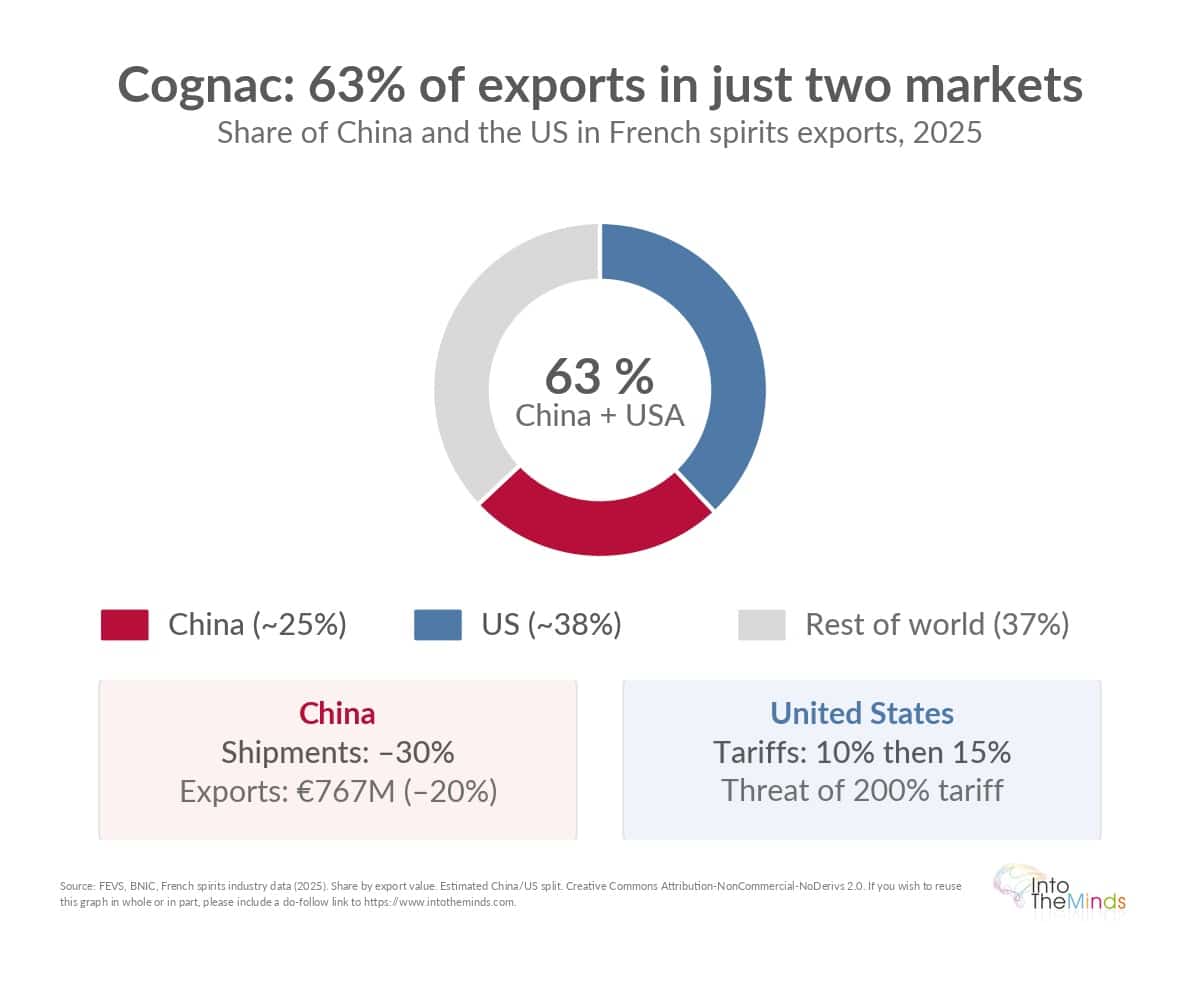

- The cognac market remains dominated by two geographical areas: China and the United States account for 63% of French spirits exports in 2025

- Trade tensions led to a 30% drop in shipments to China in 2025 following anti-dumping measures

- Major houses (LVMH, Rémy Cointreau, Pernod Ricard) are adapting their strategies with mixed results depending on the market

- The domestic French market remains modest but culturally rooted, with 47% of French people reporting consuming cognac in 2024

- Innovation focuses on customer experience (spiritourism) and environmental sustainability rather than the product itself. Packaging constraints are therefore becoming more noticeable (see this other article on the topic)

An international market under geopolitical pressure

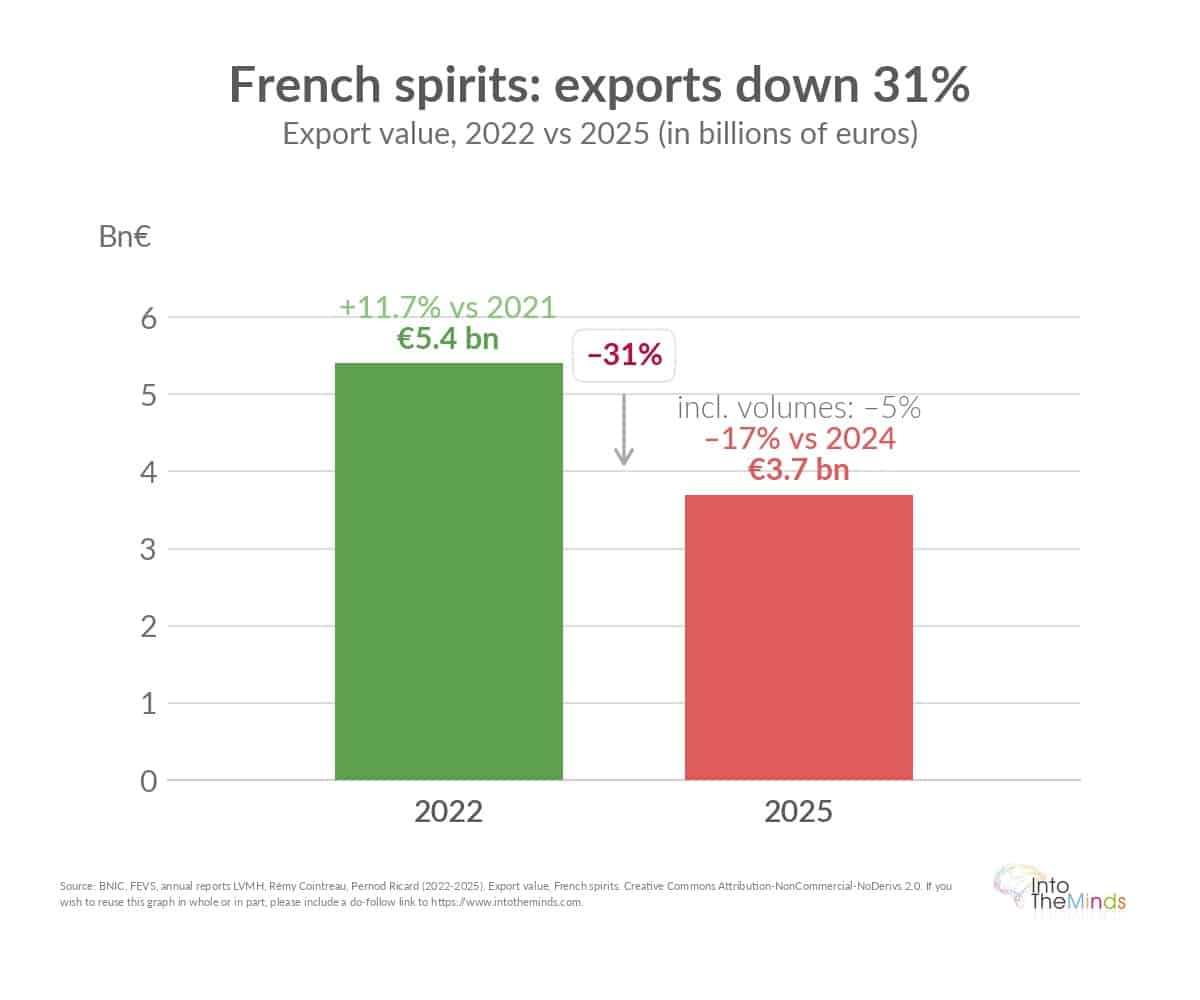

Analysis of the cognac market reveals a structural dependence on exports, which is both its strength and its vulnerability. In 2022, French spirits exports reached €5.4 billion, up 11.7% compared to 2021. Cognac retained its leading position, despite a slight decline of 3.7%.

This situation deteriorated significantly from 2024 onwards. In 2025, the value of French spirits exports fell to €3.7 billion, a decrease of 17% compared to 2024 and 31% compared to 2022 (see chart below). Volumes also declined by 5%, particularly affecting French wine-based spirits.

This evolution illustrates a new reality: the cognac market can no longer rely on linear growth. Global demand persists, but it is fragmenting and becoming politicized. Producers must now integrate geopolitical risks into their commercial strategies.

Geographical concentration: strength and Achilles’ heel

The cognac industry relies on two main markets that largely determine its performance. In June 2025, China and the United States accounted for 63% of exported sales in the French spirits sector. This geographical concentration creates a powerful leverage effect but also exposes the sector to systemic risks.

The French cognac market

Unlike export markets, the domestic cognac market remains secondary in volume. In French mass retail, sales declined by 9.49% in 2022 compared to 2021. The broader category (cognac, armagnac, calvados) represented €65.11 million in 2022, down 4%, for 3.01 million units.

This relative weakness does not prevent a strong cultural presence. In 2024, 47% of French respondents said they consumed cognac. During end-of-year festive meals, 15% cited it as their preferred digestif. Cognac therefore retains a symbolic place in French consumption habits, particularly during celebrations. However, as you will see in the chart below, domestic usage is not enough to sustain the profitability of spirits groups. Growth happens abroad.

The Chinese challenge: between crisis and adaptation

The Chinese market was heavily impacted in 2025. The anti-dumping investigation targeting European spirits led to a 30% drop in shipments. Direct exports of French wines and spirits to China fell to €767 million, a decrease of 20% compared to 2024.

In response to this crisis, the industry negotiated a minimum price agreement that limited the damage. For Rémy Cointreau, the potential additional cost was reduced to €10 million, compared to €40 million initially expected. The sector estimates a global additional cost of 12% to 16% for entering the Chinese market, well below the initially planned duties (31% to 39%).

However, this agreement remains conditional on the reimbursement of deposits paid since October 2024 and the reopening of duty-free channels, which represent nearly 20% of revenue generated in China by French producers.

The United States: a market under scrutiny

The US market is not immune to trade turbulence. In 2025, European wines and spirits first faced an additional 10% duty, then the EU-US agreement of August 21, 2025 established a 15% tax. In early 2026, a new threat of 200% tariffs on French wines and champagnes highlights the continued instability of the trade environment.

| Market | Impact 2025 | Measures applied | Outlook |

|---|---|---|---|

| China | -30% shipments | Minimum price agreement (12–16% additional cost) | Gradual recovery Q2 2025/2026 |

| United States | 15% taxation | Variable additional duties | Improvement from Q2 2024 for some houses |

| Europe | Stable | Limited impact of Ukraine war | Position maintained |

Strategies of major cognac houses

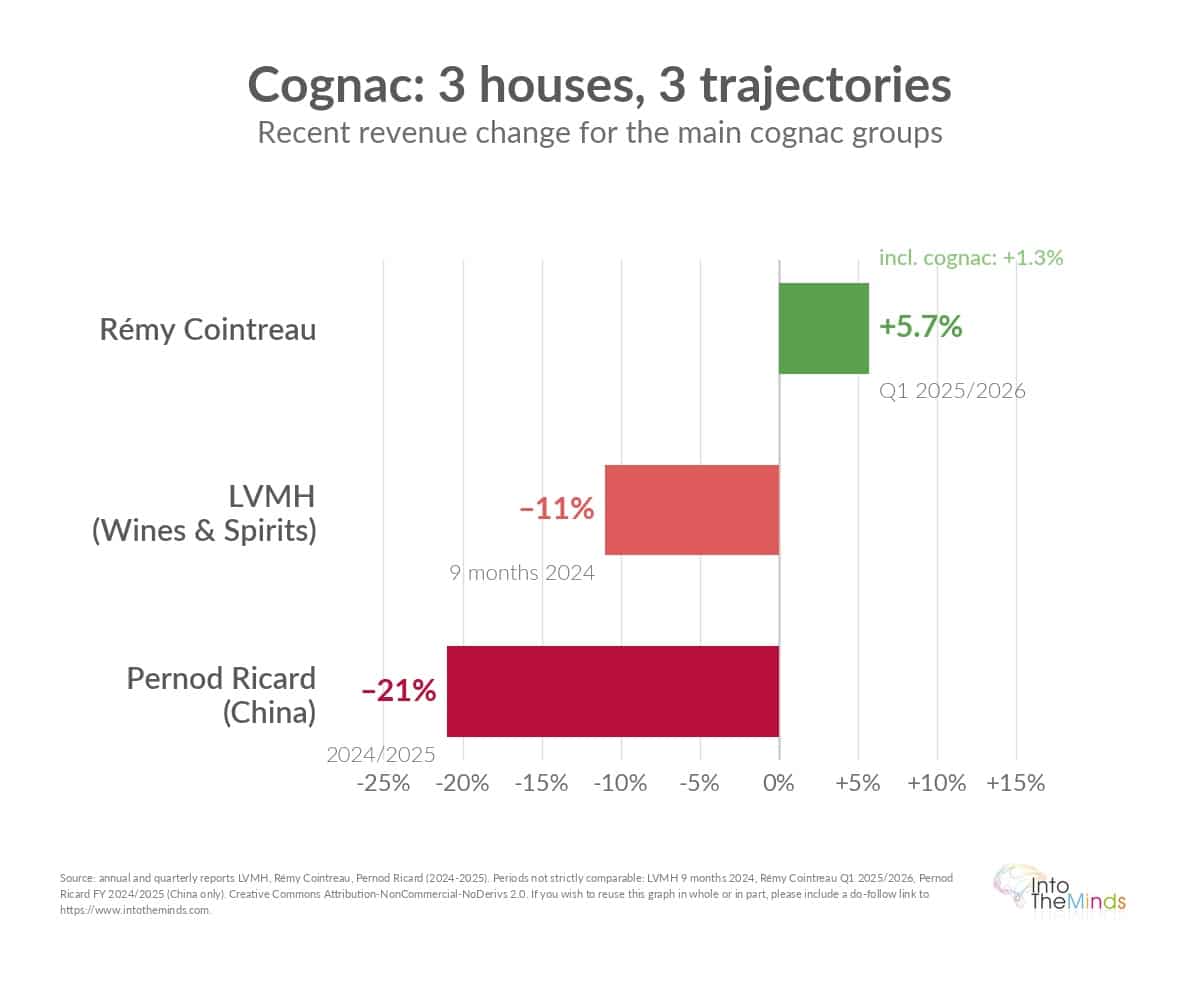

The performance of major groups illustrates different approaches to this crisis in the cognac market. Each player adapts its strategy according to its structure and sector dependency.

LVMH

Over the first nine months of 2024, LVMH’s wines and spirits business declined to €4.193 billion, down 11% reported and 8% organically compared to 2023. Hennessy was particularly affected by weak local demand in China. However, the group observed a return to growth in the United States from Q2 2024, illustrating geographical divergence.

Rémy Cointreau

With 60% of its sales linked to cognac, Rémy Cointreau shows the highest dependency. After a difficult year, Q1 2025/2026 shows improvement: revenue reached €220.8 million, up 5.7% organically. Cognac sales increased by 1.3% organically.

The group decided to reallocate part of its investments to China, indicating it sees the crisis as transitional. In April 2026, Rémy Cointreau announced its new strategy, focused entirely on profitability.

Pernod Ricard

Pernod Ricard’s strategy can be seen through its Martell cognac brand. In 2024/2025, China declined by 21% for the group. It expects duty-free recovery from Q2 2026 but remains cautious.

Innovation and transformation of the business model

Facing challenges, innovation focuses on two main axes that concern the ecosystem rather than the product itself.

Experiential innovation: spiritourism

In 2025, the sector is investing in spiritourism as a growth driver. With 2 million annual visitors across 327 sites, it can represent up to 30% of revenue and 50% in direct sales. For cognac houses, this lever enhances heritage and territory. Given these figures, I will conduct a dedicated analysis of spiritourism.

Environmental innovation

In June 2025, a coalition of 9 players including Moët Hennessy, Pernod Ricard and Rémy Cointreau launched a glass bottle reuse experiment across more than 300 retail outlets. This approach redefines premium positioning: the bottle becomes a sustainability symbol. A binding packaging regulation is also being deployed in Europe, as discussed in this article.

Outlook: stabilization rather than growth

The evolution of the cognac market between 2022 and 2026 is therefore not a smooth ride. It is more of a managerial and marketing challenge. The golden era of American rappers praising cognac is over. From a relatively robust export pillar, the sector has moved into a category under pressure but still capable of rebounding.

Three elements suggest stabilization rather than a long-term decline:

- Cognac remains strategically important enough for groups to reinvest as soon as a trade agreement allows it.

- Despite the crisis, the United States remains a key market where some houses are already seeing improvement.

- Minimum price agreements in China show that the cognac market still carries sufficient political and economic weight to be subject to specific negotiations.

The main medium-term risk is not only declining demand, but the dependence on a limited number of markets and distribution channels, in an environment that has become highly sensitive to customs decisions and high-end consumer sentiment.

Frequently asked questions about the cognac market

What are the main export markets for cognac in 2025?

China and the United States largely dominate the cognac market, accounting for 63% of exported sales of the French spirits industry in 2025. These two markets largely determine sector performance, creating both significant opportunities and risks linked to geographic concentration.

How do trade tensions affect the cognac sector?

Trade tensions have a direct and significant impact. In 2025, the Chinese anti-dumping investigation led to a 30% drop in shipments to this market. At the same time, the United States imposed a 15% tariff on European wines and spirits. These measures force producers to adapt their strategies and negotiate specific agreements, such as the minimum price agreement with China.

Is the French cognac market growing?

The domestic French market remains modest and slightly declining. Sales in mass retail fell by 9.49% in 2022 compared to 2021. However, cognac maintains a strong cultural presence: 47% of French consumers reported drinking it in 2024, and 15% use it as a digestif during festive meals. For in-depth market research on consumption habits, IntoTheMinds can support you.

What innovations are transforming the cognac industry?

Innovation is focused on three main axes: commercial (minimum price agreements), experiential (spirit tourism with 2 million annual visitors across 327 sites), and environmental (glass bottle reuse). These innovations do not concern the product itself but its economic ecosystem and value creation.

How are major houses adapting to the market crisis?

Each group is adopting a different strategy. LVMH is focusing on geographic diversification and already sees improvement in the United States. Rémy Cointreau, more dependent on cognac (60% of sales), is reinvesting in China despite the crisis. Pernod Ricard is taking a cautious approach with Martell, anticipating a gradual recovery. These contrasting strategies reflect different levels of geographic risk exposure. For analyzing these competitive dynamics, specialized market research can provide valuable insights.