We analyze the latest figures on business failures and their evolution over the past few years. We reveal the symptoms and root causes of bankruptcy and confirm the value of market research and a differentiated marketing strategy.

Since 2022, corporate bankruptcies in Europe have risen continuously. In 2025, France recorded a particularly high number of business failures, while Germany and Spain saw their indicators reach worrying levels. The first data for 2026 show no overall reversal of this trend. Behind these figures lie deep structural causes that neither a return to growth nor lower interest rates will be sufficient to erase. In this analysis, our consulting firm provides a comprehensive review of the situation as of mid-2026. We also devote significant attention to the impact on employment and to the distinction between visible symptoms and the root causes of the deterioration. Our conclusions converge in confirming the value of staying closely aligned with market developments (for example through a market reseintotheminds.com/…/marketing-strategy-and-trendsarch study) and implementing a differentiating marketing strategy.

Contact the IntoTheMinds Institute

Key Takeaways

- Globally, corporate insolvencies increased by approximately 10% in 2024, 6% in 2025, and a further increase of 3% is expected in 2026. This represents five consecutive years of growth.

- In Europe, 1.3 million jobs are threatened by insolvencies in 2026 (out of 2.2 million worldwide).

- France reached a historically high level of business failures in 2025, and the first quarter of 2026 has already set a new record for jobs at risk.

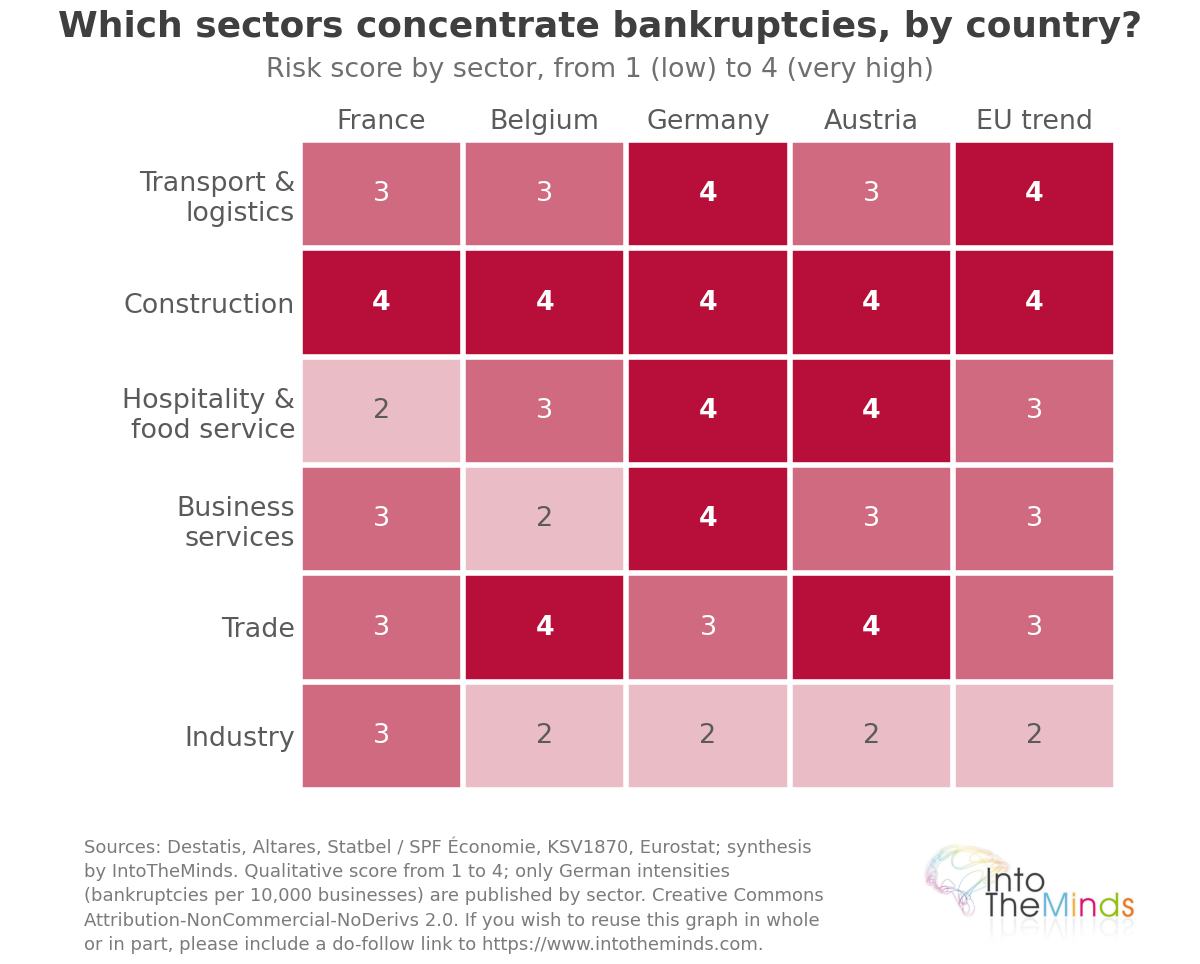

- The sectors most exposed in Europe are, in descending order of severity: transport and logistics, construction, hospitality and food services, and business services.

- The current wave is not the result of a single cyclical shock, but rather the combination of the end of Covid-related support measures, rising interest rates, and structural weaknesses that have accumulated over more than a decade.

- Signs of easing were observed at the end of 2025 in certain sectors (construction and hospitality): the peak may be near, but the underlying causes remain.

Overview of Bankruptcies in Europe in 2026

To understand the current situation, it is important to distinguish between two measures that are too often confused: the absolute number of bankruptcies and their intensity relative to the business population. These two geographical rankings do not coincide.

Evolution of Corporate Insolvencies

Since 2022, insolvencies have increased continuously in almost all European countries.

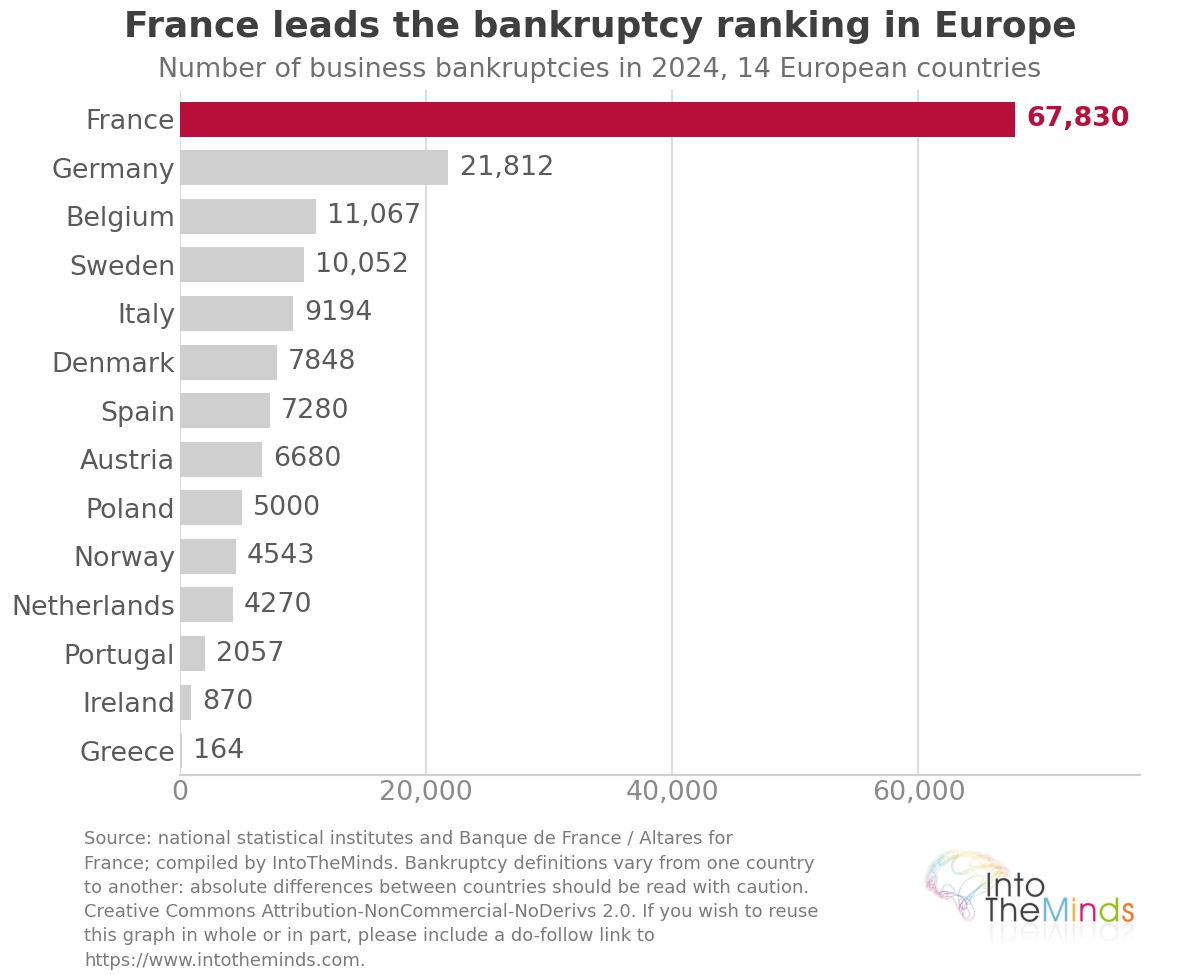

- In France, the number of business failures rose from 42,514 in 2022 to 69,957 in 2025 according to Altares, representing a cumulative increase of +64% in three years. The country thus came close to the symbolic threshold of 70,000 annual insolvencies, a level never reached before (the previous record dated back to 2009, at around 63,700).

- In Germany, Destatis recorded 24,064 corporate insolvencies in 2025, following annual increases of +22.1% in 2023 and +22.4% in 2024, the highest level since 2014.

- Spain reached 13,000 insolvencies in 2025, its all-time record, according to the Estadística del Procedimiento Concursal.

- The number of bankruptcies in Belgium reached 11,665 in 2025 according to Statbel, matching its historical record set in 2013.

Far from indicating a slowdown, the beginning of 2026 confirms the ongoing pressure. In France, the Banque de France recorded 68,961 restructurings and liquidations over the twelve months ending January 2026 (+4.1% year-on-year), while Altares reported 71,100 insolvencies over the twelve months ending March 2026, including 19,000 new proceedings in the first quarter alone (+6.4% compared with the first quarter of 2025). Since January 2026, more than 300 business owners have appeared before commercial courts every working day. According to an audit firm, however, the number of insolvencies could stabilize at around 65,000 for the whole of 2026.

On a global scale, bankruptcies increased by 10% in 2024 compared with 2023 and by 6% in 2025, according to Allianz Trade. In 2026, insolvencies are expected to rise by a further 3%, marking the fifth consecutive year of growth. In Europe, 1.3 million jobs are threatened by these corporate insolvencies in 2026, including 960,000 in Western Europe, out of a worldwide total of 2.2 million.

1.3 million jobs are threatened by these corporate insolvencies in 2026

Comparison by Country and European Region

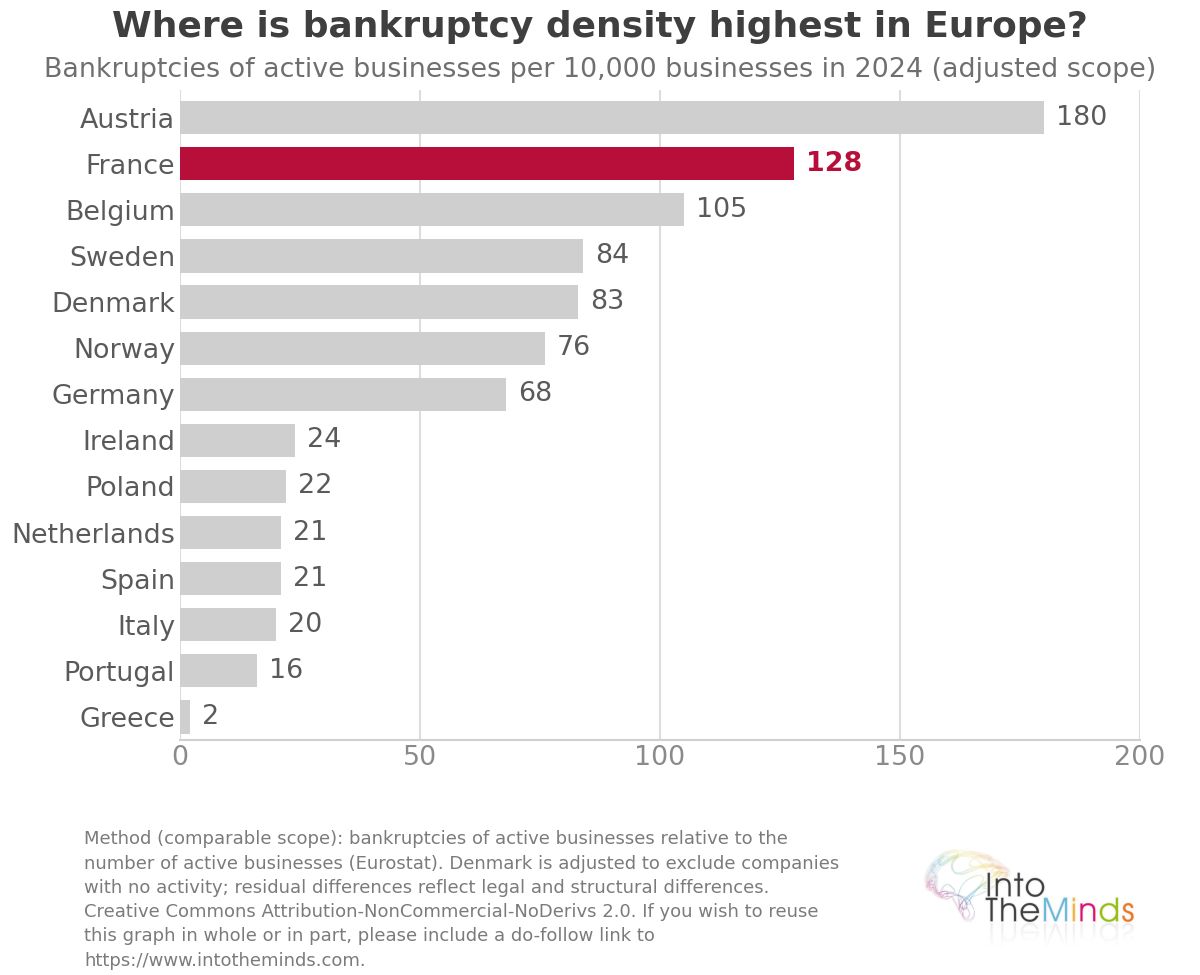

When adjusted for the number of companies, the 2024 insolvency rates (bankruptcies per 10,000 companies) reveal a ranking very different from that based on absolute volumes:

| Country | Bankruptcies per 10,000 Companies (2024) | Comment |

|---|---|---|

| Austria | 180 | Includes proceedings rejected due to insufficient assets |

| France | 128 | |

| Belgium | 105 | |

| Sweden | 84 | |

| Denmark | 83 | Includes dissolutions of inactive companies |

| Norway | 76 | |

| Germany | 68 | |

| Ireland | 24 | |

| Poland | 22 | |

| Netherlands | 21 | |

| Spain | 21 | |

| Italy | 20 | |

| Portugal | 16 | |

| Greece | 2 |

These differences partly reflect variations in statistical scope rather than actual risk. Austria counts proceedings rejected because of insufficient assets, whereas most countries do not. Denmark includes the dissolution of inactive companies. Cross-country comparisons should therefore be treated with caution, but the sectoral hierarchy within a given country remains reliable.

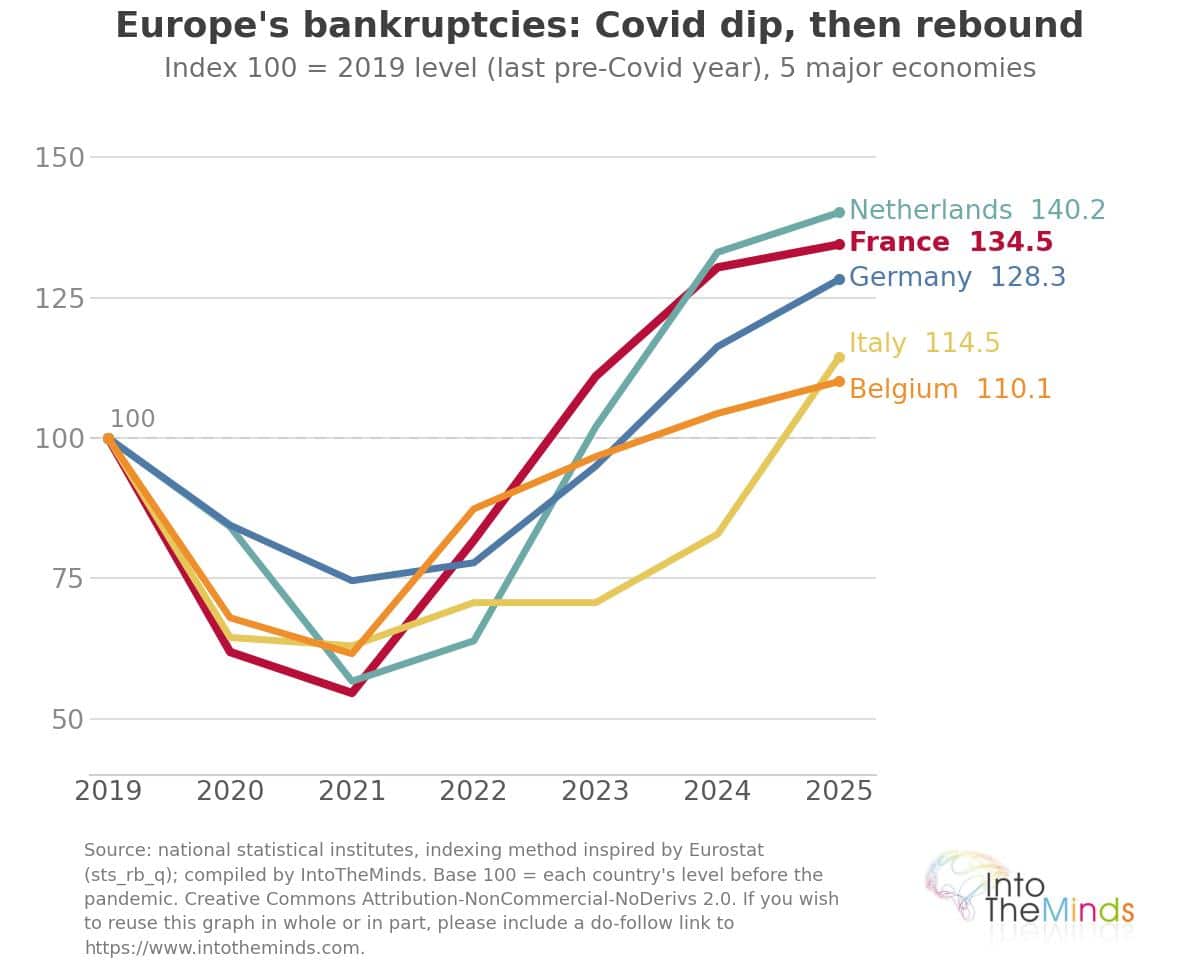

The base index (2019 = 100) confirms the pressure: in 2025, the level reached 140.2 in the Netherlands, 134.5 in France, 128.3 in Germany, 114.5 in Italy, and 110.1 in Belgium.

Another way to measure severity is to relate jobs at risk to the number of unemployed people in each country. In 2026, this ratio stands at:

- 11% in France

- 9% in the United Kingdom

- 7% in Germany

- 4% in Italy

- 1% in Spain

It is in France that the materialization of this risk would weigh most heavily on an already tight labor market. The year 2025 also saw marked accelerations in several countries, with increases in insolvencies of around 35% in both Greece and Italy, and an apparent surge in Switzerland (+40% to +54%) largely due to a legislative revision that expanded the statistical scope.

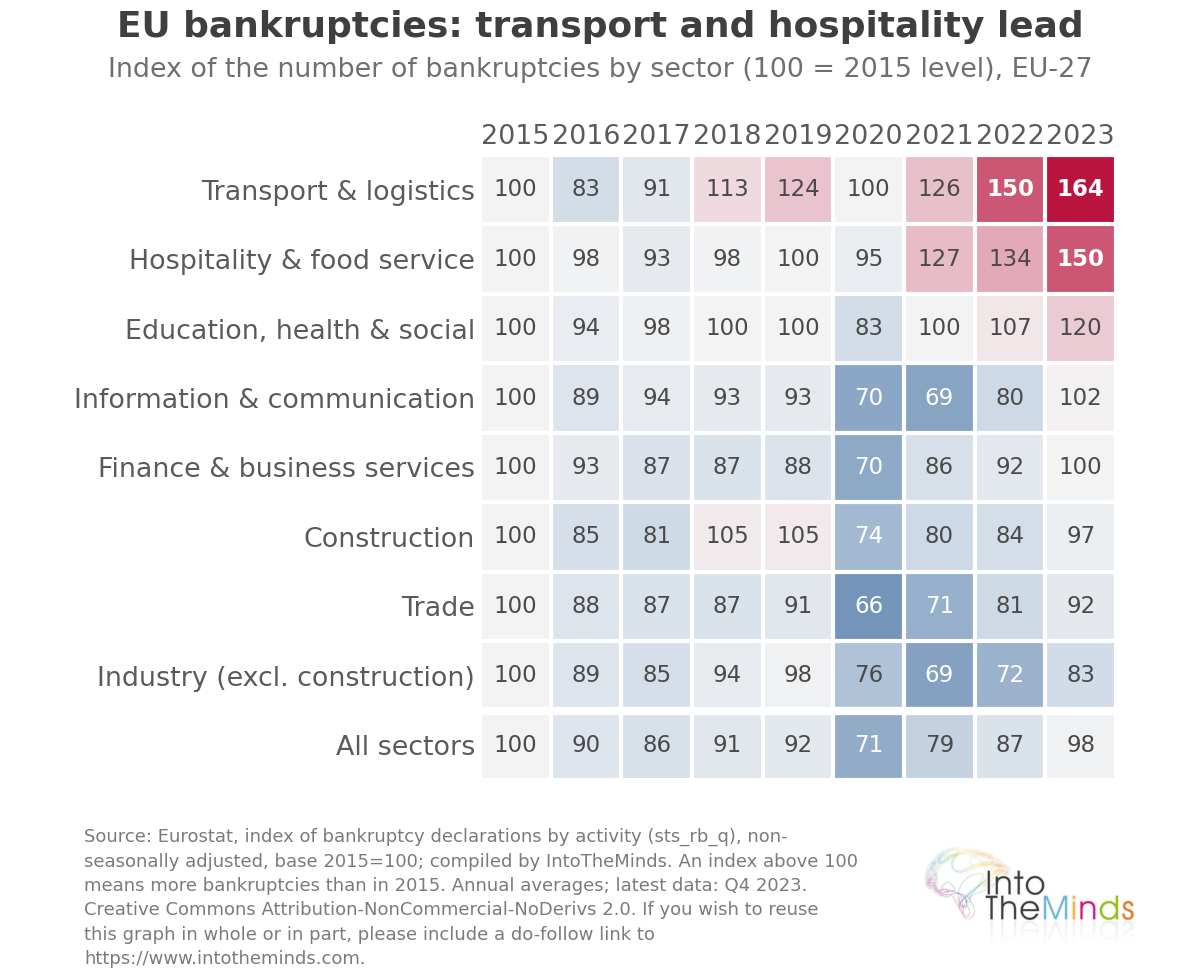

Sectors most affected by insolvencies

Regardless of the country, corporate failures are concentrated in the same activities. In terms of intensity, the 2024 European ranking places transport and logistics in first position, ahead of construction, hospitality and food services, and business services. In Germany, Destatis data for 2025 illustrate this order precisely: 133 insolvencies per 10,000 companies in transport and logistics, 108 in hospitality and food services, 104 in construction, and 100 in business services, compared with a national average of 69.

The deterioration becomes clear when compared with the first half of 2024, when overall intensity was still only 31.2 per 10,000: transport and logistics were already in the lead (60.9), ahead of construction (47.4), business services (46.8), and hospitality and food services (40.8). In just one year and a half, the risk has therefore more than doubled in the most exposed sector.

Corporate failures are concentrated in the same activities: transport and logistics, construction, hospitality and food services.

The human impact: employment on the front line

Behind the volume of bankruptcies, employment is the real issue at stake.

In France, an estimated 267,000 employees and business owners saw their jobs eliminated or threatened in 2025, after around 255,737 jobs at risk in 2024. Not all of these positions are ultimately lost: according to CNAJMJ, of more than 150,000 jobs involved in collective proceedings up to October 6, 2025, 37,000 were in liquidation, while more than 93,000 were under restructuring and therefore temporarily preserved. In the second quarter of 2025 alone, Infogreffe recorded 54,147 jobs at risk, including 21,498 lost through liquidation and nearly 30,000 preserved through restructuring. The public safety net has been heavily mobilized: the wage guarantee scheme (AGS) paid a record €2.233 billion in 2025 for 250,000 guaranteed salaries, corresponding to an average advance of €8,800 per employee. And the trend is worsening: in the first quarter of 2026, more than 75,000 jobs were at risk in France, a record exceeding the previous peak of 73,000 in Q1 2009.

Belgium provides a useful regional breakdown: 27,187 jobs were lost due to bankruptcies in 2024, distributed across Flanders (15,553), Wallonia (7,297), and Brussels (4,233). In SMEs alone, retail accounted for 2,337 bankruptcies and 5,932 job losses, out of a total of 25,784 jobs according to the Federal Public Service Economy.

Austria, the country with the highest intensity, illustrates the scale of the social and financial impact: 29,600 employees affected in 2024 (+25% year-on-year) according to KSV1870, with liabilities rising by 35% to €18.9 billion and 50,300 creditors impacted.

Early signs of easing: is a peak in sight?

The picture is not uniformly bleak, and several signals observed at the end of 2025 are worth highlighting.

- In France, construction-sector bankruptcies fell by 8% in the final quarter of 2025, while failures in DIY/home equipment (see our market study here) and hospitality declined by 13% and 19% respectively over the year.

- In Germany, large insolvencies (cases involving more than €25 million in claims) decreased by 15.6%, bringing insolvency-related claims down from €58.1 billion in 2024 to €47.9 billion in 2025.

- In Austria, the number of employees affected in the first nine months of 2025 fell by around 20% year-on-year, to roughly 15,000 people. These inflections suggest that the peak of the wave may be approaching in certain sectors and countries, but they say nothing about the underlying causes, which remain unchanged.

25 years of bankruptcies in Europe: the 6 major waves

The historical series reveals not a linear trend, but three distinct waves driven by different forces, separated by an unprecedented inverted gap.

- 2000–2007: elevated levels without a systemic shock. Germany reached its historical peak with around 39,300 insolvencies in 2003–2004, before declining to 29,160 in 2007. Southern Europe remained at low levels (Italy at 6,131 in 2007, Spain under 1,000 cases per year). Notable failures were isolated, often industrial or fraud-related: Sabena in Belgium (7,500 jobs, 2001), Moulinex in France (5,600, 2001), Philipp Holzmann in Germany (23,000, 2002), and the Parmalat accounting scandal in Italy (36,000, 2003).

- 2008–2009: synchronized global shock. France jumped from 49,700 to 63,700 insolvencies, Spain increased fivefold in two years (from 988 to 4,984), and Germany rose to 32,687. The collapse of Arcandor/Karstadt-Quelle in Germany threatened 68,000 jobs (the largest of the quarter-century), followed by Olympic Airways in Greece (8,500) and the Dutch healthcare group Meavita (20,000).

- 2010–2014: sovereign debt crisis, north–south divide. Italy peaked at 15,705 insolvencies in 2014 (its historical record), Spain at 8,916 in 2013, while Germany declined to 24,085 in 2014. The divide was documented in real time: a market study estimated €340 billion in written-off receivables in Europe in 2012, with average payment delays of 91 days in the south versus 33 in the north, and Greece’s loss rate rising from 4.9% in 2011 to 5.9% in 2012. Major failures included Schlecker (25,000, Germany), Praktiker (19,500), Pescanova (10,000, Spain), Ilva (13,500, Italy), and BES in Portugal (10,000).

- 2015–2019: misleading downturn. Near-zero ECB interest rates kept structurally weak companies alive. Germany fell to 18,749 insolvencies in 2019, France to 52,002. Notable failures included Air Berlin (8,600, 2017), Imtech (22,000, Netherlands), Abengoa (24,000, Spain), V&D (10,000, Netherlands). These reflected idiosyncratic weaknesses rather than a systemic crisis.

- 2020–2021: artificial trough due to Covid. France dropped to 28,371 insolvencies in 2021, Germany to 13,993. These unprecedented levels—barely half the pre-crisis plateau—resulted entirely from emergency public support, including the French €110 billion plan (€80 billion in grants and roughly €160 billion in loans). Only a few major cases broke through the barrier, including Wirecard in Germany (1,800, 2020).

- 2022–2026: the major reversal, detailed below.

What the long history shows

Three key lessons emerge.

- First, Europe has experienced three distinct waves driven by different underlying forces (the 2008–2009 financial crisis, the 2010–2014 sovereign debt crisis, and the current post-Covid wave), separated only by the single true reversal of the period: the pandemic trough, entirely created by public intervention.

- Second, the center of gravity has shifted: the crisis initially hit the Southern European periphery in the 2010s; today it affects the core of the continent (France, Germany’s industrial base) and long-resilient northern economies such as Sweden, reaching record levels.

- Finally, and this is the crucial nuance, the current wave is not everywhere a record in absolute volume: France and Spain reached historical highs in 2025, but Germany (24,064) remains below its 2003–2004 peak (around 39,300) and Italy (12,700) below its 2014 record (15,705). What distinguishes the present moment is less the raw volume than the intensity relative to the corporate base and the increasing size of individual failures.

A payment beyond 60 days increases bankruptcy risk by 25%, and by 40% beyond 90 days.

The underlying causes of current European bankruptcies

Liquidity pressures and payment delays are visible symptoms, not root causes. In France, a large majority of companies reported payment delays in 2025 (86% versus 82% in 2023), representing several billion euros in immobilized cash flow. A payment beyond 60 days increases bankruptcy risk by 25%, and by 40% beyond 90 days. But these symptoms are only fatal because deeper structural fragilities make them so.

Six main root causes combine:

- The end of cheap money: a decade of near-zero interest rates, extended by Covid support measures, kept structurally unprofitable companies alive. The rate hikes starting in 2022 exposed their latent insolvency.

- Undercapitalization of European SMEs: thin equity buffers and heavy reliance on bank credit mean that even small cash-flow disruptions can bring companies down. This is precisely why payment delays are so damaging.

- The persistent energy shock: energy costs remain significantly higher than those faced by US and Asian competitors, weighing on Europe’s industrial competitiveness.

- Structural transitions: the shift to e-commerce is eroding physical retail; the transition to electric vehicles is reshaping automotive and its suppliers (Northvolt, KTM); legacy formats are losing customers (department stores, traditional travel agencies).

- Post-Covid over-indebtedness: debt accumulated during the pandemic, including guaranteed loans and deferred charges, has permanently weakened balance sheets.

- Weak demand: low growth and consumption constrained by loss of purchasing power compress margins, further aggravated in France by political and fiscal instability that encourages wait-and-see behavior.

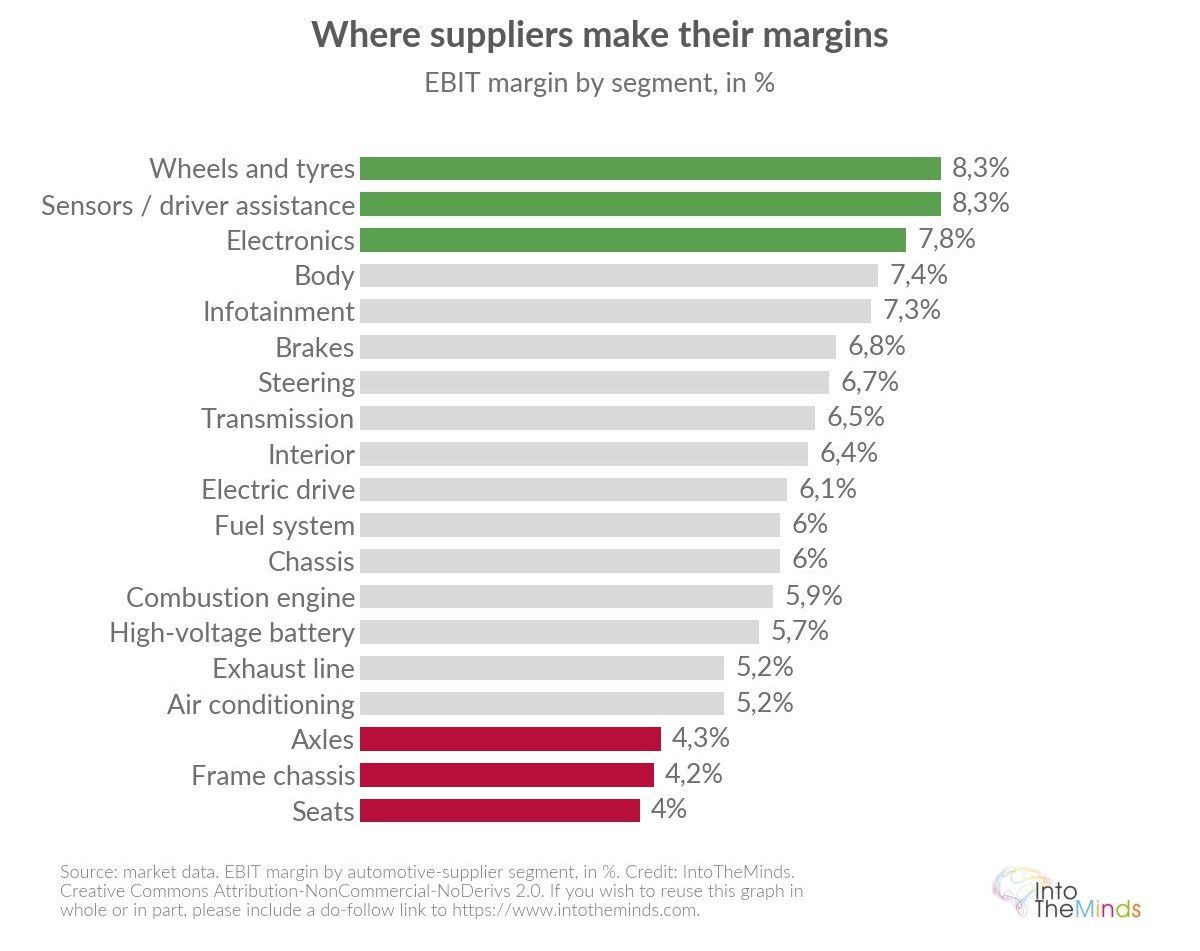

All this leads to a loss of competitiveness that some countries are exploiting to gain ground in the European market. The automotive industry is a particularly illustrative case. European regulations have destabilized legacy manufacturers, who have been overtaken by Chinese competition offering technologically advanced and heavily subsidized vehicles.

More broadly, business mortality is also driven by structural issues such as a mismatch between supply and demand or a lack of managerial competence. For context, here are some interesting failure-rate statistics:

- Canada: 60% failure rate within the first 5 years. Source: Statistics Canada (PALE)

- France: 49.5% failure rate within the first 5 years. Source: INSEE

- Tunisia: 39% failure rate within the first 2 years. Source: BTS (Banque Tunisienne de Solidarité)

- Netherlands: 50% failure rate within the first 5 years. Source: CBS (Statistics Netherlands)

- United States: 50% failure rate within the first 4 years. Source: US Census Bureau (BITS)

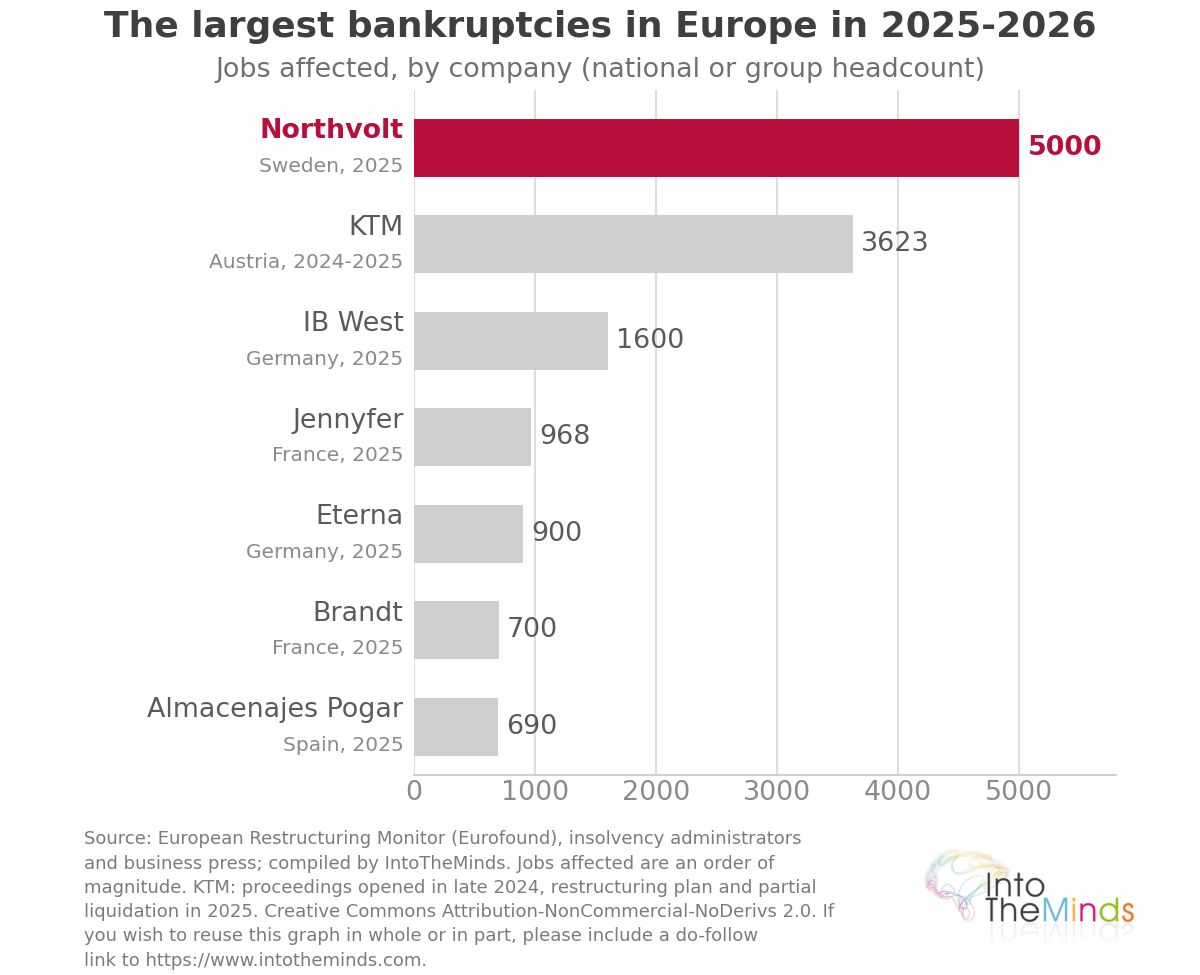

Major European bankruptcies from 2024 to 2026

The most widely reported corporate bankruptcies of the past two years reflect exactly these sectoral vulnerabilities.

| Company | Country | Sector | Date | Jobs affected |

|---|---|---|---|---|

| Northvolt | Sweden | Batteries / industry | March 2025 | approx. 5,000 |

| KTM | Austria | Automotive | Late 2024 | 3,623 employees |

| Van Hool | Belgium | Buses / transport | 2024 | 2,411 layoffs |

| Esprit | Europe (1,300 in Germany) | Clothing | 2024 | 1,650 jobs eliminated in Europe |

| IB West | Germany | Social services | November 2025 | 1,600 employees |

| Eterna | Germany | Textile | December 2025 | 900 employees |

| Brandt | France | Home appliances | December 2025 | 700 jobs eliminated |

| Jennyfer | France | Fashion | April 2025 | 729 of 968 jobs lost |

| Almacenajes Pogar | Spain | Logistics / transport | November 2025 | 690 employees |

These cases illustrate three structural dynamics: the energy transition putting pressure on entire industrial sectors (Northvolt in batteries, KTM in automotive), margin pressure in transport and logistics (Almacenajes Pogar), and the collapse of legacy distribution models (Esprit, Jennyfer, Brandt).

Europe is lagging behind and struggling to reinvent itself.

A concrete example is the margin structure in the automotive sector. The situation is highly uneven, and foreign competition is progressively moving up the value chain to capture market share. This makes entire industrial segments less profitable, leading—like in the case of KTM—to high-profile failures.

Numerical summary

This section presents the statistics used in the analysis, from global to local level.

World and Europe

- +10% / +6% / +3%: global increase in bankruptcies in 2024 (vs 2023), 2025 (vs 2024), and 2026 (vs 2025), Allianz Trade

- 2.2 million: jobs at risk worldwide in 2026; 1.3 million in Europe; 960,000 in Western Europe.

- 11% / 9% / 7% / 4% / 1%: share of jobs at risk relative to unemployment in 2026 in France, UK, Germany, Italy, and Spain.

- Index base 2019 = 100, 2025 level: Netherlands 140.2, France 134.5, Germany 128.3, Italy 114.5, Belgium 110.1

- National volumes 2024: France 67,830, Germany 21,812, Belgium 11,067, Sweden 10,052, Italy 9,194, Denmark 7,848, Spain 7,280, Austria 6,680, Poland 5,000, Norway 4,543, Netherlands 4,270, Portugal 2,057, Ireland 870, Greece 164

Sector risk (intensity)

- Germany 2025 (per 10,000 companies): total 69, transport-logistics 133, hospitality 108, construction 104, business services 100

- Germany H1 2024 (per 10,000): total 31.2, transport-logistics 60.9, construction 47.4, business services 46.8, hospitality 40.8

- 30%: share of manufacturing in jobs affected by insolvencies in Germany

Historical benchmarks (annual volumes)

- Germany: ~39,300 in 2003–2004 (peak), 32,687 in 2009, 18,749 in 2019 (low), 24,064 in 2025

- France: 49,700 in 2008, 63,700 in 2009 (previous record), 28,371 in 2021 (Covid low), 69,957 in 2025 (all-time record)

- Italy: 6,131 in 2007, 15,705 in 2014 (record), 12,700 in 2025

- Spain: <1,000 before 2008, 8,916 in 2013, 13,000 in 2025 (record)

- Belgium: 11,740 in 2013 (record), 11,665 in 2025

- Sweden: 10,052 in 2024 (record)

Germany, Belgium, Austria (current)

- Germany: 24,064 insolvencies in 2025 (Destatis), 23,900 according to Creditreform; +10.3% vs 2024; €47.9bn losses vs €58.1bn in 2024; large insolvencies ≥€25m down 15.6%; 140 insolvencies with >250 employees; €57bn creditor losses.

- Belgium: 27,187 jobs lost in 2024 (15,553 Flanders, 7,297 Wallonia, 4,233 Brussels); +17% / +12% / +12% in construction, retail and logistics.

- Austria: 6,587 insolvencies in 2024; 29,600 employees affected (+25%); liabilities €18.9bn (+35%); 5,120 insolvencies Jan–Sept 2025 (+5.5%); 15,000 employees affected (-20%).

France (volumes & employment)

- 69,957: insolvencies in 2025 (+3.1% vs 2024); +34% in 2022, +33% in 2023, +18% in 2024

- 71,100: 12-month rolling figure as of March 2026; 19,000 in Q1 2026 (+6.4%); 68,961 end-January 2026; 65,000 expected in 2026

- 267,000: jobs at risk in 2025; 75,000 in Q1 2026 (record)

- 150,000: jobs affected up to 6 Oct 2025 (37,000 liquidations, 93,000 restructurings)

- 250,000: wages guaranteed by AGS in 2025; €2.233bn paid; €8,800 average advance per worker

- 27%: construction share of 2024 proceedings; employment split between construction (19%), services (19%), retail (15%), industry (13%)

- Late-2025 easing: construction -8%, DIY -13%, hospitality -19%

FAQ: Questions You May Have

Which European country shows the highest bankruptcy intensity?

In 2024, Austria ranks first with 180 bankruptcies per 10,000 companies, ahead of France (128) and Belgium (105). This Austrian position is partly explained by a broader statistical scope than in other countries: Austria also counts proceedings rejected due to insufficient assets, which most European states do not record.

Why are there so many business failures in France at the moment?

France combines several factors: the catch-up effect from bankruptcies artificially avoided during Covid (estimated at 50,000 cases between 2020 and 2023), the structural undercapitalization of SMEs, payment delays affecting 86% of companies in 2025, and a production structure concentrated in highly exposed sectors such as construction. It is also the country where threatened jobs weigh most heavily relative to unemployment (11% in 2026). A targeted B2B market study in a specific sector or region helps assess exposure to client or partner default risk precisely.

Which sectors are most exposed to bankruptcies in Europe?

By intensity (insolvencies relative to the number of companies in each sector), transport and logistics ranks first across Europe in 2024, followed by construction, hospitality, and business services. In Germany, Destatis data for 2025 confirm this hierarchy: 133 insolvencies per 10,000 companies in transport-logistics, compared with a national average of 69.

How many jobs are at risk from bankruptcies in Europe?

In 2026, 1.3 million jobs are at risk in Europe due to business failures, including 960,000 in Western Europe, out of a global total of 2.2 million. In France, 267,000 employees and business leaders were affected in 2025, and more than 75,000 jobs were at risk in Q1 2026 alone, a record. Not all are lost: of the 150,000 jobs under insolvency proceedings by late 2025, roughly one quarter were in liquidation, the rest in restructuring.

Will the wave of bankruptcies decline in 2026?

Several signs of easing appeared at the end of 2025: a decline in construction bankruptcies (-8% in Q4) and hospitality (-19% over the year) in France, and a drop in large German insolvencies (claims reduced from €58.1bn to €47.9bn). French bankruptcies could stabilize around 65,000 in 2026. However, these shifts are sector-specific and fragile, and the underlying causes (undercapitalization, energy costs, post-Covid debt overhang) remain: a sustained downturn is not guaranteed.

Is the current wave of bankruptcies in Europe the worst in recent history?

Not uniformly. France and Spain reached historic highs in 2025. But Germany, with 24,064 insolvencies in 2025, remains well below its 2003–2004 peak (around 39,300) and below its 2009 level (32,687). Italy, at 12,700 cases, is also below its 2014 record (15,705). What distinguishes the current wave is less its absolute volume than the increasing size of failing companies and the persistence of deep structural drivers.

![Illustration of our post "Porsche: Strategy and Scenarios for Overcoming the Crisis [Analysis]"](/blog/app/uploads/porsche-taycan-carrera-911-120x90.jpg)