After years of success, Porsche finds itself in a very difficult situation. Its margin has been divided by 15, and the number of cars sold is declining. In this article, we analyze Porsche’s strategy and possible scenarios for the brand’s future.

![Porsche: Strategy and Scenarios for Overcoming the Crisis [Analysis]](/blog/app/uploads/porsche-taycan-carrera-911.jpg)

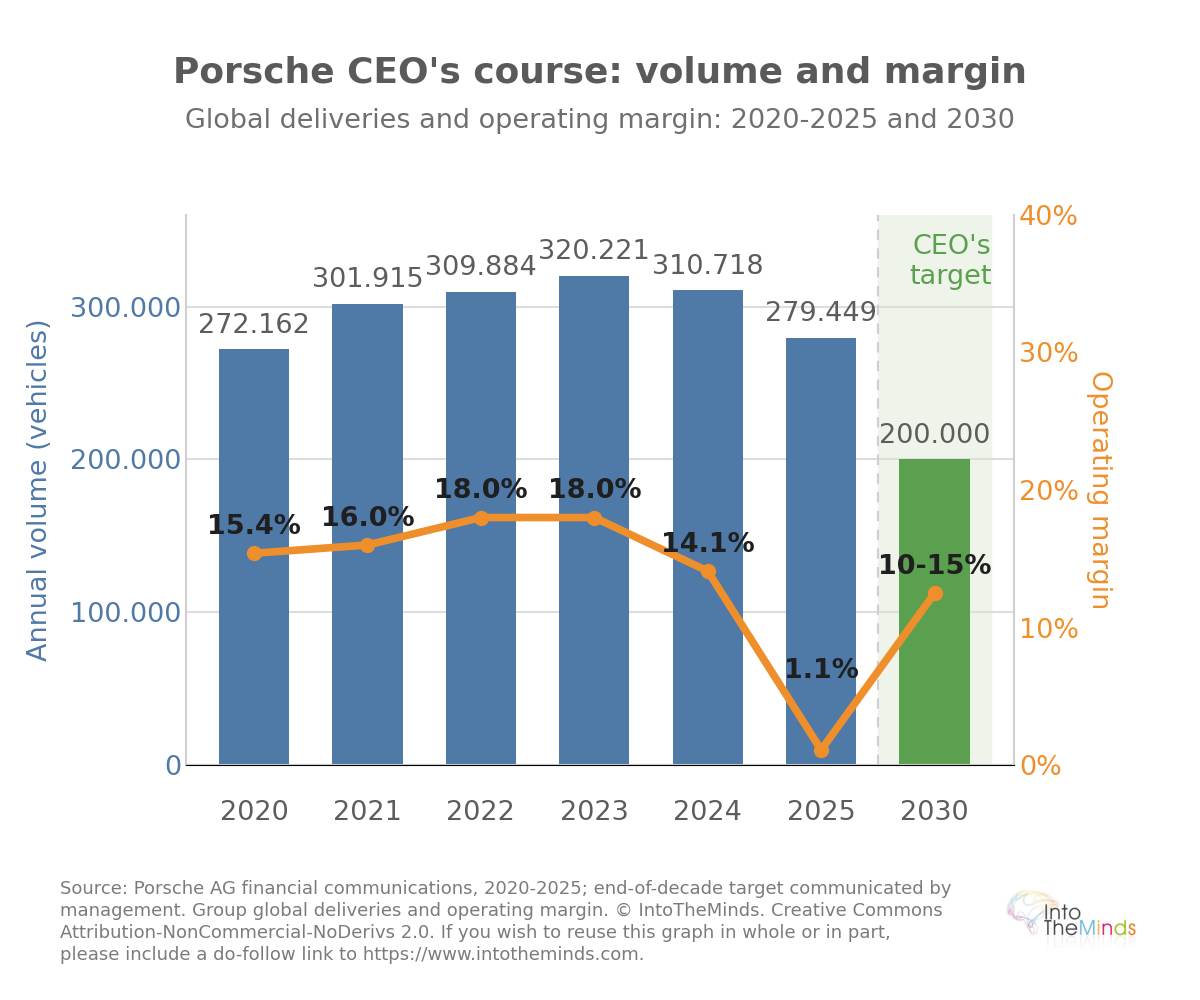

For 20 years, Porsche was an exception in the luxury car market: increasing production did not jeopardize its marketing positioning, and its margins were on par with the most premium brands such as Ferrari. This model broke down between 2024 and 2025, as operating margin fell from 18% to 1.1% in 3 years. Today, under the leadership of Michael Leiters, the company is trying to turn a forced contraction into a deliberate repositioning strategy. The stakes are high: proving that a company producing 200,000 vehicles can be more profitable than one producing 320,000. In this article, our marketing consulting firm analyzes Porsche’s trajectory and the different possible recovery scenarios, while also providing a comprehensive analysis of Porsche’s strategic evolution over the past 20 years.

Contact the IntoTheMinds institute

Key takeaways

- Between 2022 and 2025, Porsche’s operating margin fell from 18% to 1.1%, due to the combined effects of the collapse of the Chinese market, U.S. tariffs, and the cost of the electric transition.

- Global deliveries declined from 320,221 vehicles in 2023 (an all-time high) to 279,449 in 2025 (-10%), including a -26% drop in China to 41,938 units.

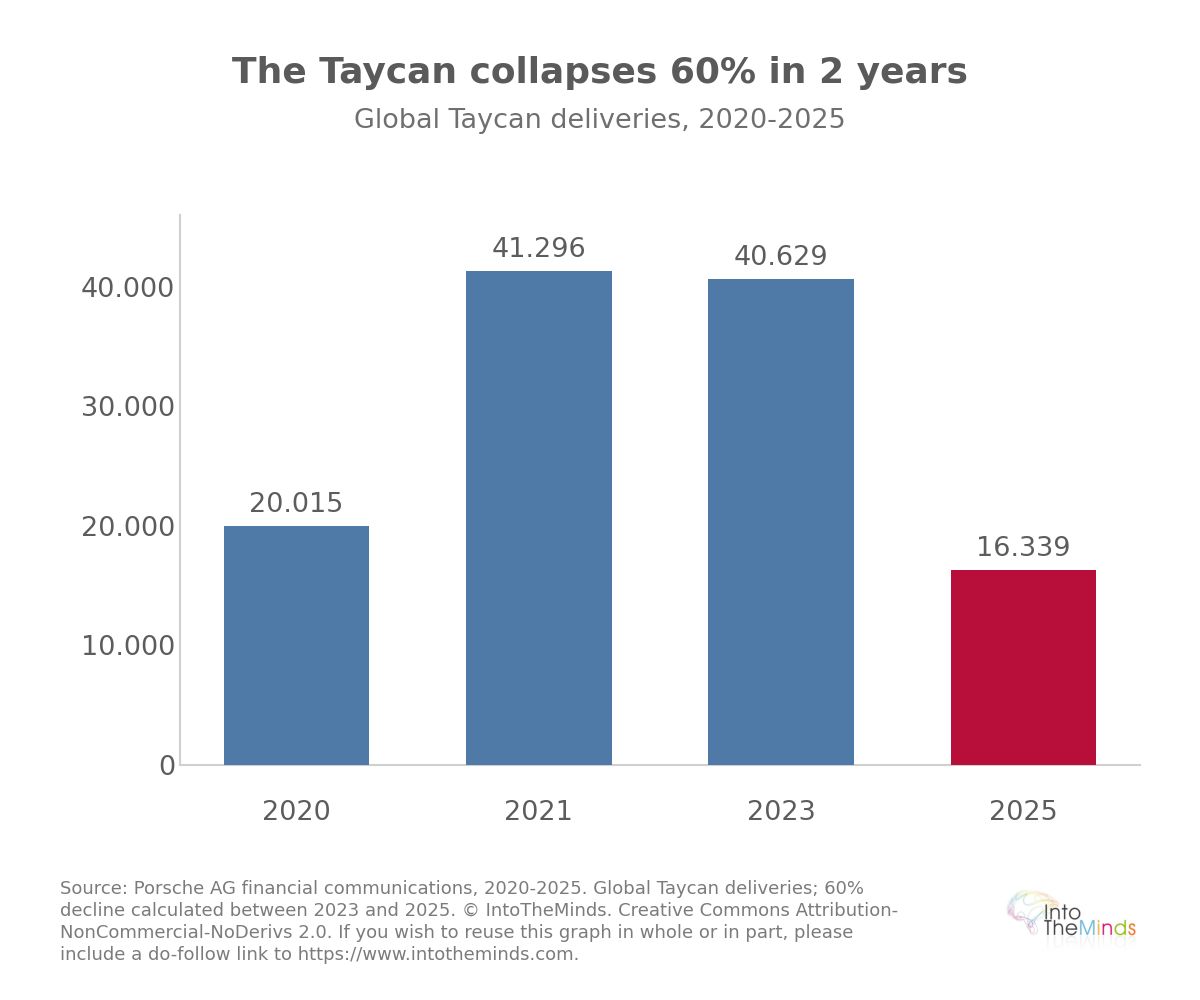

- The Taycan, the electric gamble launched in 2019, collapsed to 16,339 deliveries in 2025, a decline of nearly 60% compared with the 40,629 units sold in 2023.

- Management is now imposing structural downsizing: targeting a margin of 10 to 15% by the end of the decade, even with volumes reduced to 200,000 vehicles per year.

- Revenue for the coming fiscal years is expected to stabilize, with a slightly improving target operating margin, still far below pre-crisis levels.

20 years of Porsche strategy summarized

Porsche’s trajectory over the past two decades is that of a company that chose to grow without ever officially giving up exclusivity. The launch of the Cayenne in 2002 marked the beginning of this transformation: of the 66,803 cars sold worldwide that year, 20,603 were Cayennes. An SUV accounting for nearly one-third of a sports car brand’s sales sent a clear signal.

The Macan, launched in 2014, accelerated the trend. The Leipzig factory, inaugurated with an annual capacity of 50,000 units, sold 44,636 vehicles in just seven months of commercialization. In 2014, global deliveries reached 189,849 vehicles, of which 58% were Cayenne and Macan SUVs, generating revenue of €17.2 billion, up 20% compared with 2013.

The founding tension between volume and desirability

This growth carried an inherent contradiction that management itself articulated clearly as early as 2015: Porsche’s challenge was “to remain small.” The CFO at the time summarized the issue in a sentence that became emblematic: “if everyone drives a Porsche, it’s no longer exclusive.” Official policy openly embraced a voluntary limitation of availability.

If everyone drives a Porsche, it’s no longer exclusive.

Lutz Meschke, CFO Porsche (2015)

The cost of scaling up volume was nevertheless measurable. Global margin fell from 18% in 2013 to 15.8% in 2014, precisely because SUVs, sold at lower prices than pure sports cars, weighed more heavily in the sales mix. Management acknowledged that it earned less on the Macan than on the 911. Porsche then occupied a unique positioning: between the ultra-luxury segment of Ferrari or Aston Martin (voluntarily capped at around 7,000 to 10,000 units per year) and the premium segment of BMW or Mercedes-Benz.

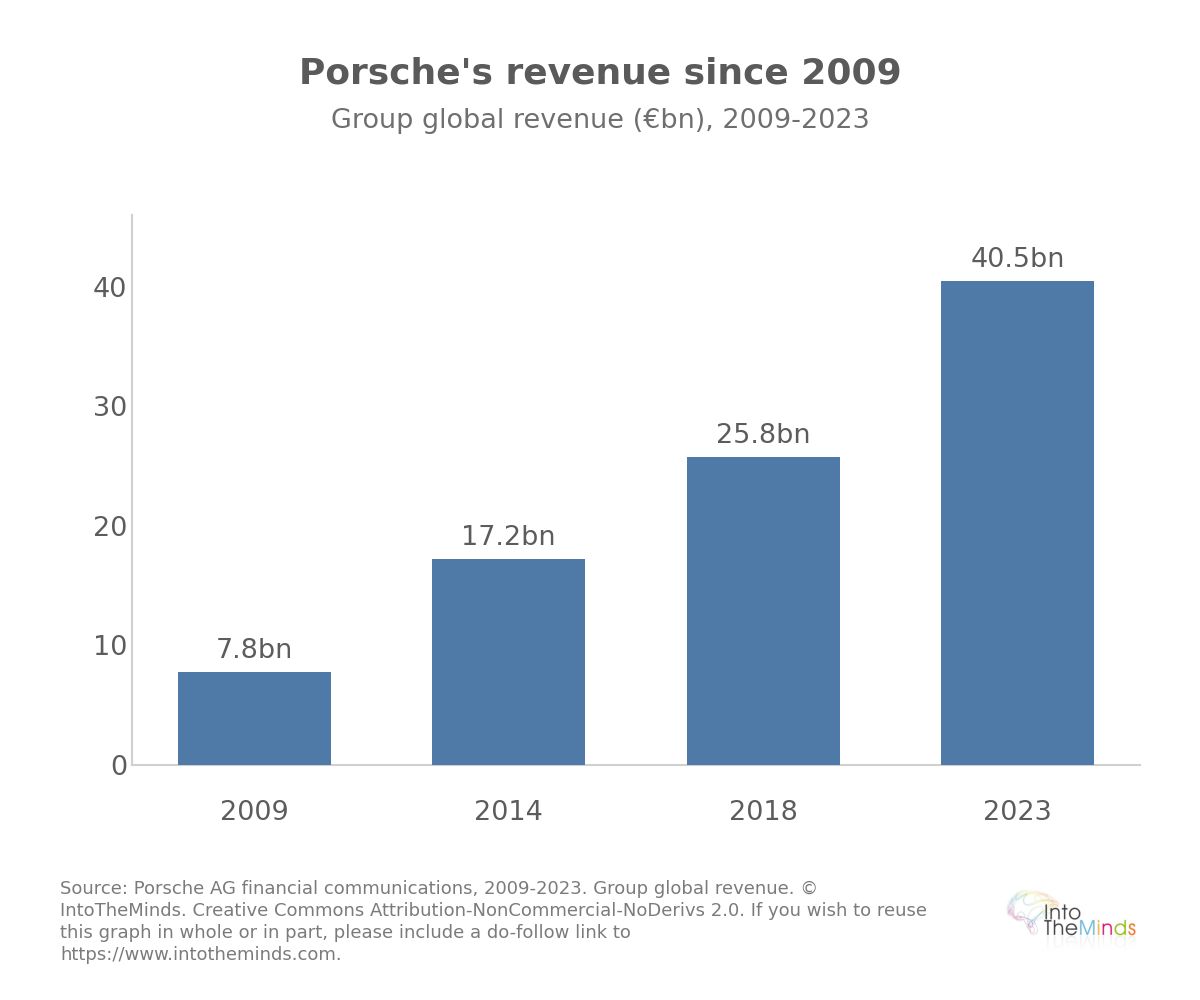

At the end of this expansion phase, in 2018, global revenue had reached €25.8 billion for approximately 260,000 vehicles, compared with €7.8 billion in 2009. In less than ten years, revenue had more than tripled.

The peak years: 2019–2023

At the end of the 2010s, Porsche established itself as the financial jewel of the Volkswagen Group. In 2019, while Audi and Daimler together announced nearly 20,000 job cuts, Porsche created 2,000 jobs, posted a 16.3% margin—the highest in the automotive sector—and grew revenue by 7%. The company set itself a dual objective: maintain a minimum 15% margin and become a “Zero Impact Company”.

The 2020 pandemic revealed the resilience of the model. In the first half of 2020, Porsche posted the best operating result among European carmakers, at €1.23 billion. For the full year, operating profit reached around €4 billion with a 15.4% margin, and 272,162 global deliveries. China already accounted for roughly 89,000 units, nearly one-third of global sales.

2021 marked a peak: revenue up 15% to €33 billion, operating profit up 27% to €5.3 billion, a 16% margin, and for the first time more than 300,000 vehicles delivered (301,915, +11%). Within the Volkswagen Group, Porsche posted a 16.5% margin, outperforming all other automotive brands except Lamborghini (20.2% on only 8,405 units), and far ahead of Audi (10.5%) or the VW brand (3.3%).

| Year | Revenue (€bn) | Operating profit (€bn) | Operating margin | Global deliveries |

|---|---|---|---|---|

| 2019 | ~28.0 | ~4.6 | 16.3% | ~280,000 |

| 2020 | ~26.0 | ~4.0 | 15.4% | 272,162 |

| 2021 | 33.0 | 5.3 | 16.0% | 301,915 |

| 2022 | 37.6 | 6.8 | 18.0% | 309,884 |

| 2023 | 40.5 | 7.3 | 18.0% | 320,221 (peak) |

| 2024 | ~40.0 | 5.64 | 14.1% | 310,718 |

| 2025 | 36.27 | 0.41 | 1.1% | 279,449 |

Porsche’s electric bet

Porsche’s shift to electric mobility was initiated early and presented as a deliberate strategic choice. Development of the Taycan began in 2015, later described by management as “one of the riskiest decisions” in the brand’s history. The technical argument relied on 800-volt architecture, enabling 5% to 80% charging in around 22 minutes—a first in mass production—and on driving dynamics derived from more than 70 years of sports car expertise.

The Taycan marks Porsche’s electric turning point.

The 2019 commercial launch confirmed strong market appetite: more than 30,000 pre-reservations (with a €2,500 deposit in Europe) and over 10,000 firm orders, for a vehicle starting at around €100,000. In Germany, the two highest-end versions—Turbo at €150,000 and Turbo S at €185,000—illustrated the ambition to move upmarket through electrification.

The rise and collapse of the Taycan

Initial momentum was strong. In 2020, 20,015 Taycans were delivered despite six weeks of production shutdown due to COVID, followed by about 41,296 in 2021—nearly a doubling. By Q3 2021, the Taycan (28,640 units) had even overtaken the 911 with its “flat-six” engine (27,972 units). For the first time in its history, Porsche had a new flagship model. In Europe, around 40% of Porsche sales were already electrified at that time.

The reversal was abrupt. In 2025, Taycan deliveries collapsed to 16,339 units, down roughly 60% compared to 40,629 units in 2023. This decline is explained by several factors:

- rising Chinese competition in the high-end EV segment

- slower-than-expected global EV market growth

- demand in China that has essentially dried up

Adjacent technological bets: batteries, software and e-fuels

Three major investments structured the pre-crisis technology strategy—arguably rational bets given Porsche’s strong financial position and commercial success:

- Batteries (Cellforce): Porsche invested in high-performance cells via the Cellforce joint venture (2021) with Customcells in Reutlingen. Capacity was scaled from 100 MWh to 1 GWh (about 1,000 to 10,000 vehicles per year), with €60 million invested and €60 million in public subsidies. In 2025, the battery strategy was reassessed, impacting planned production projects.

- Software: After internal failures via Cariad, Oliver Blume shifted toward US and Chinese tech partnerships, including cooperation with Apple and discussions with Google on Android Automotive in 2023. This external dependency proved difficult to manage.

- E-Fuels: Porsche invested around €500 million in a pilot plant in Chile with Siemens Energy to preserve the internal combustion engine of the 911. The goal was to bring costs below $2 per litre (vs. around $10 in pilot phase). The project, widely criticized for poor energy efficiency, remained marginal within R&D spending: of €2.6 billion total R&D, roughly three-quarters went to electrification and about €100 million to e-fuels.

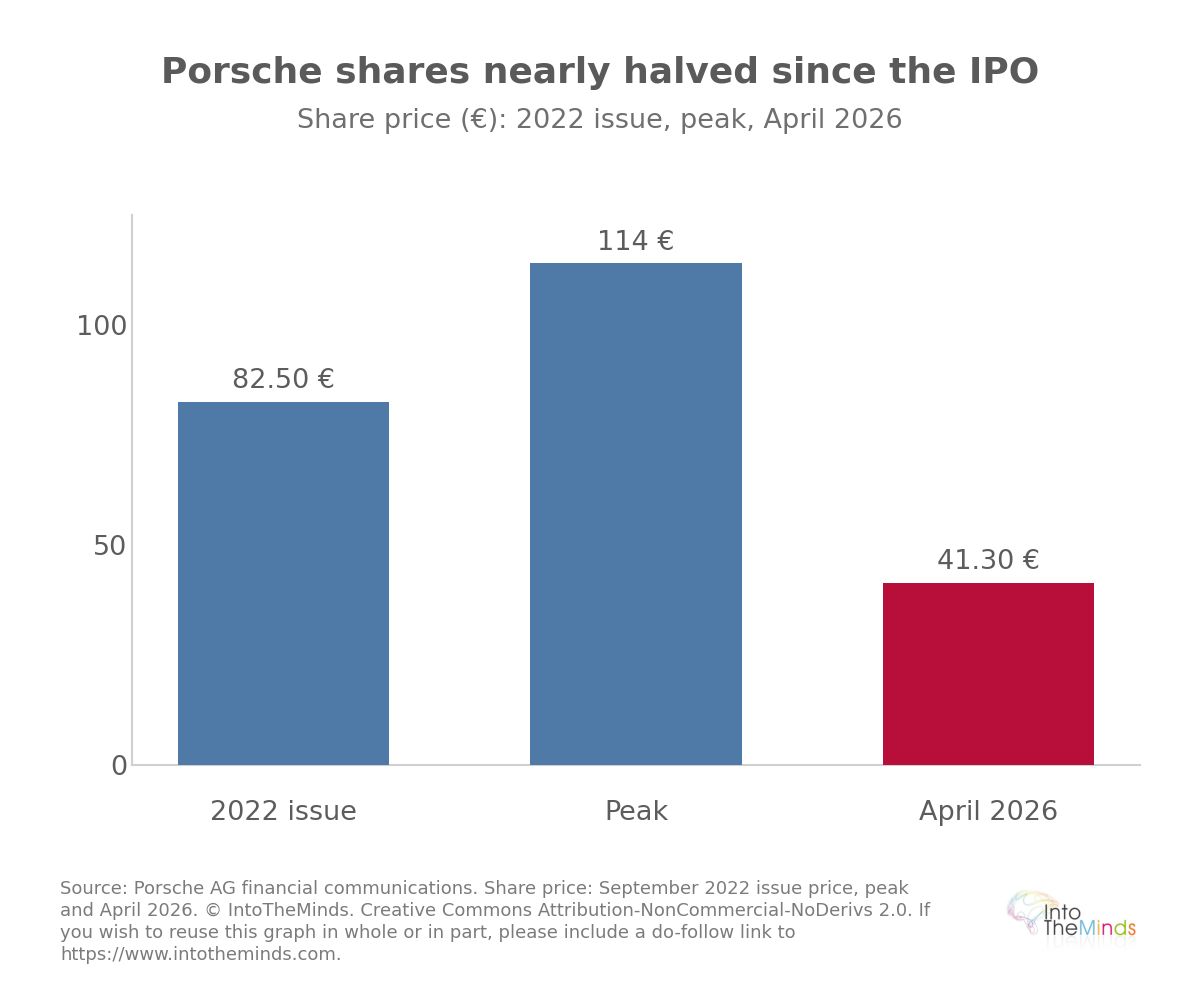

At its peak valuation, Porsche was worth more than the entire Volkswagen Group.

The 2022 IPO

The IPO on 29 September 2022 marked the culmination of a push for autonomy led by Oliver Blume since 2015. Despite a deteriorating macro environment (Ukraine war, inflation, rising interest rates), the deal was a major success. At an issue price of €82.50, Porsche was valued at $75 billion and raised €9.4 billion—the largest European listing in 11 years. The offering was roughly five times oversubscribed.

Four anchor investors secured nearly 40% of the deal:

- Qatar (up to €1.88 billion, ~5%)

- Norway (€750 million)

- Abu Dhabi (€750 million)

- a US fund (€300 million)

The Porsche-Piëch family bought back 25% plus one share of ordinary shares for around €10 billion, financed by ~€7 billion in debt. The stock climbed to €114, pushing market capitalization above €80 billion. Porsche was then worth more than the entire Volkswagen Group.

Analysts already highlighted governance weaknesses that later re-emerged during the crisis:

- Oliver Blume’s dual role as CEO of both Porsche and Volkswagen Group

- limited free float (12.5%)

- Volkswagen retaining at least 75% of capital and relying on Porsche cash flows to fund weaker brands

- potential conflicts of interest in investments, platforms and semiconductor sourcing

- a dual-class share structure reinforcing family control

The record 2022 results—€37.6 billion revenue (+13.6%), €6.8 billion operating profit (+27.4%), 18% margin and €916 million dividend—masked these structural weaknesses. Three years later, the share price fell to €41.30 in April 2026, roughly half the IPO level, reflecting a significant valuation correction.

Porsche now targets only 30,000 annual sales in China.

The anatomy of the crisis: China, tariffs and the electric transition

Le retournement began in 2024, which Porsche described as a “transition year.” The deterioration was rapid and cumulative, driven by three simultaneous shocks.

The collapse of the Chinese market

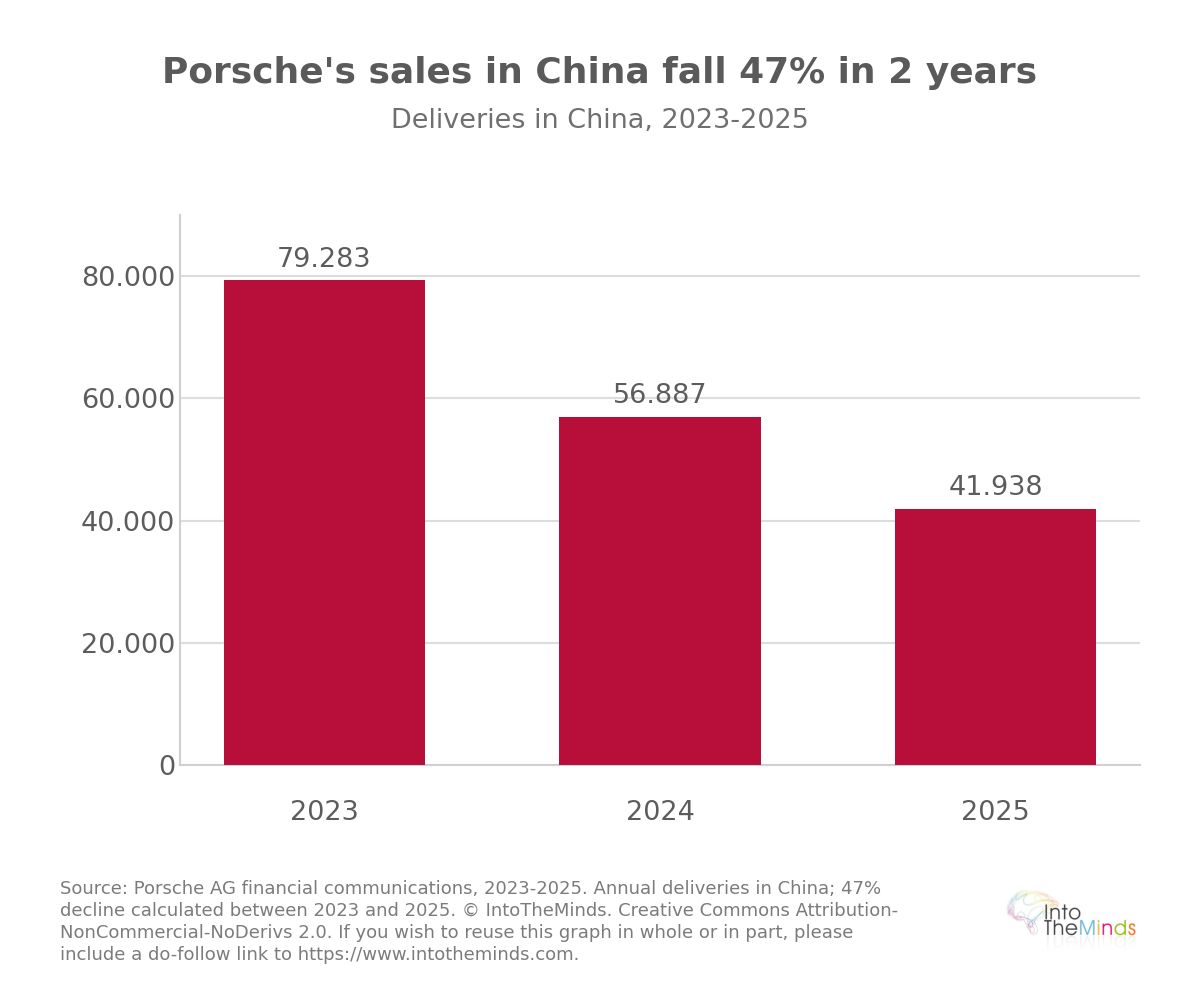

China had been Porsche’s growth engine for a decade. At its peak, the Chinese market accounted for nearly a quarter of global deliveries, with 79,283 units in 2023. The decline was dramatic and symptomatic of the problems facing the German automotive industry:

- 2023: 79,283 deliveries in China

- 2024: 56,887 deliveries (-28%), representing 12% of global sales

- 2025: 41,938 deliveries (-26%), with the market now ranking third behind North America and Europe

- First quarter 2026: 7,519 deliveries (-21%)

Management acknowledged a luxury market that had “literally collapsed” and aggressive local price competition. Porsche reduced its dealer network in China from more than 120 to around 80 locations and now expects annual sales in the country to stabilize at roughly 30,000 vehicles.

US tariffs and the vulnerability of a single production base

Porsche manufactures exclusively in Germany, in Zuffenhausen and Leipzig. This geographic concentration, which was not an issue during the era of free trade, became a major problem with US tariffs. In 2025, these tariffs cost more than €500 million by the end of September, and approximately €700 million for the full year! Despite this, North America became Porsche’s largest market in the first quarter of 2026 (18,344 deliveries), but this geographic shift comes with structural exposure to the uncertainties of US trade policy.

The cost of the electric transition reset

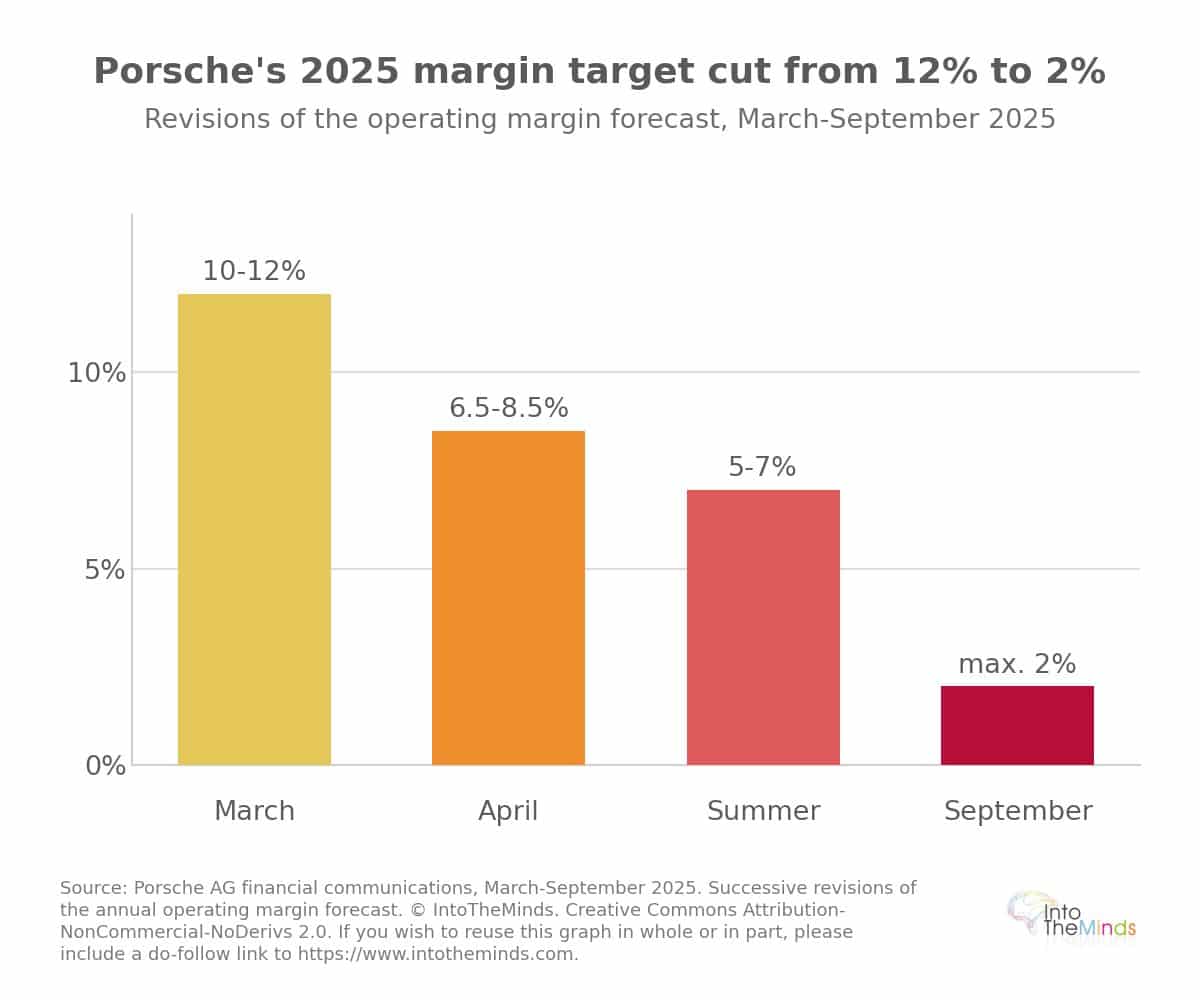

The deterioration in the operating margin forecast for 2025 was spectacular: initially expected to range between 10% and 12% in March 2025, it was revised down to 6.5–8.5% in April, then to 5–7% under the impact of US tariffs, and finally reduced to a maximum of 2% on September 19, 2025. This latest announcement included a €1.8 billion charge related to postponing the electric offensive: the new SUV series above the Cayenne, initially planned as fully electric, was shifted toward combustion-engine and plug-in hybrid versions. Total exceptional costs for 2025 reached approximately €2.4 billion for product realignment, plus €700 million related to batteries.

On the social front, the first package announced in February 2025 planned 1,900 job cuts in Germany (approximately 4.5% of the company’s 42,000 global employees), later increased to 3,900 in the first cost-saving plan. The 2025 annual results confirmed the scale of the shock:

- 279,449 global deliveries (-10%)

- revenue of €36.27 billion (-9.5%)

- operating profit collapsing to €410 million (compared with €5.64 billion in 2024)

- operating margin at 1.1%.

The challenge facing the new CEO is substantial. Let us now examine his plan in detail.

The new CEO’s strategy and possible scenarios

The arrival of Michael Leiters, former executive at McLaren and Ferrari, as Porsche CEO on January 1, 2026, marks the beginning of the turnaround phase, which he detailed in a long interview with Handelsblatt. Leiters is implementing what he internally calls a downsizing: reducing size and complexity in order to restore profitability, even at a permanently lower volume than the 320,221 vehicles delivered in 2023.

The four pillars of Michael Leiters’ strategy

Since taking office, Leiters has established a coherent doctrine built around four pillars:

- Refocusing on the core business: “Porsche must refocus on its core business; this is the indispensable foundation of a successful strategic repositioning” (May 8, 2026). This principle drove the sale of stakes in Bugatti Rimac (45%) and Rimac Group (20.6%) for €411 million, as well as the closure of Cellforce, Porsche eBike Performance, and Cetitec, resulting in more than 500 additional job cuts in May 2026.

- Organizational streamlining: Leiters wants a company that is “leaner and faster,” through simplifying the management structure and reducing hierarchies and bureaucracy. The executive board, currently composed of seven members, could return to six. The integration of the Car-IT division into R&D is the first concrete example of this strategy.

- Profit before volume: The value over volume doctrine is embraced to the extent that the recalibration measures are expected to continue weighing on 2026 “in the upper hundreds of millions of euros.” The internal plan, summarized by the expression Downsizing mit Rendite, targets an operating margin of 10–15% by the end of the decade, with a break-even point allowing profitability even at volumes around 200,000 vehicles per year.

- Moving further upscale: By 2035, Leiters plans to expand the range into higher-margin segments by studying “models and derivatives both above the current two-door sports cars and above the Cayenne.” The product strategy maintains all three propulsion systems (combustion, hybrid, and full electric) across all segments until the late 2030s.

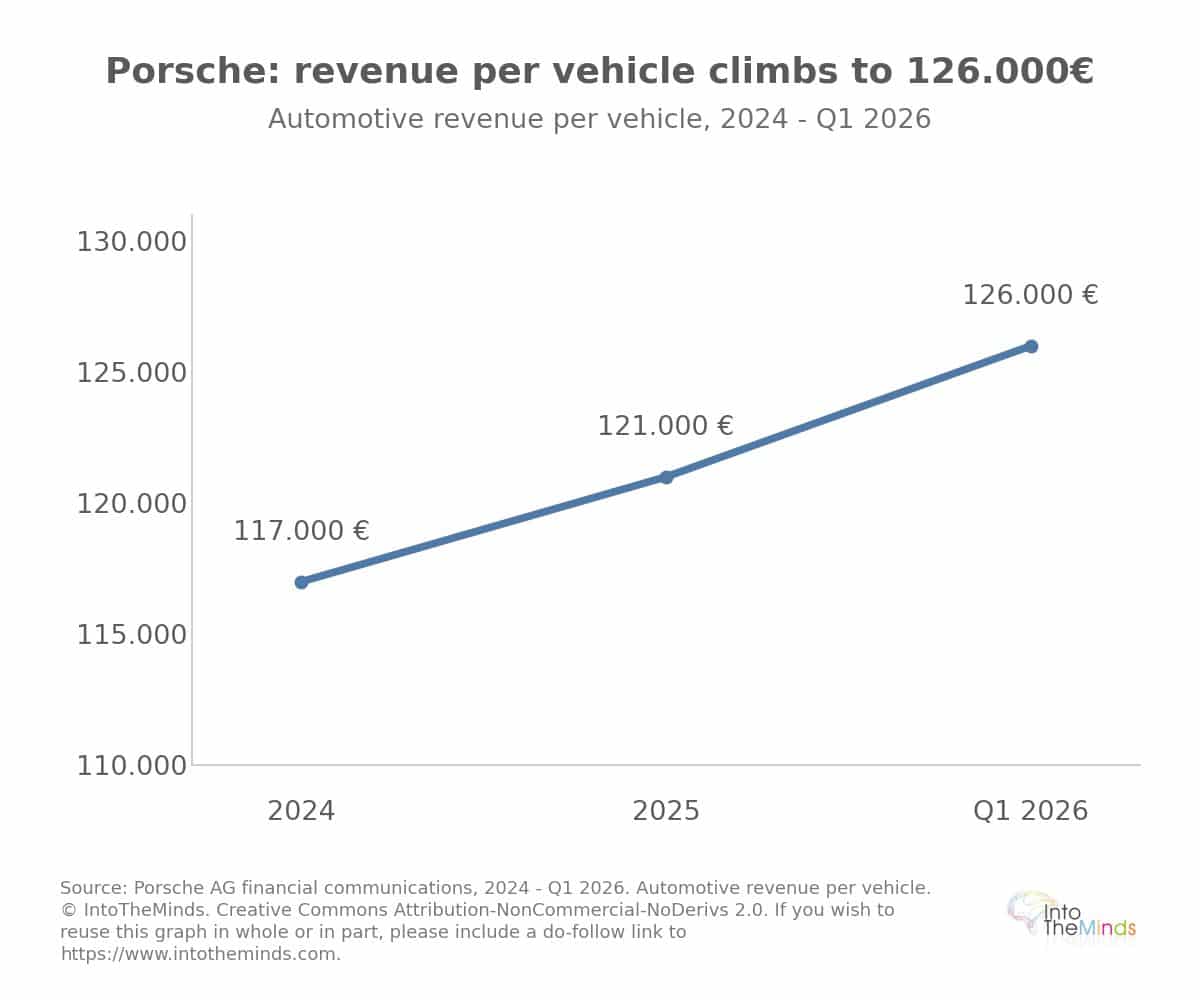

An early indicator supports this doctrine: automotive revenue per vehicle increased from approximately €117,000 in 2024 to €121,000 in 2025, then to €126,000 in the first quarter of 2026. The decline in volume is therefore accompanied by a rise in average transaction value.

Scenario 1: the “profitable manufacturer” succeeds

This is the trajectory Michael Leiters hopes to achieve. It involves transforming a forced contraction into a deliberate repositioning: accepting permanently lower volumes, possibly around 200,000 units, but with margins restored to between 10% and 15% by the end of the decade.

The most encouraging signal is the 911, up 22% in the first quarter of 2026 and reaching a record 51,583 units in 2025. If Porsche can replicate this desirability across new ultra-high-margin models, the value over volume doctrine may succeed. The opposite risk, inherited from the brand’s history, is that lower volumes could deprive Porsche of the economies of scale that, unlike Ferrari (around 11,000 vehicles in 2021), have always supported its margins. The Capital Markets Day in autumn 2026 will need to demonstrate that the break-even point can indeed be lowered without diluting the brand.

Scenario 2: the forced geographic shift toward North America

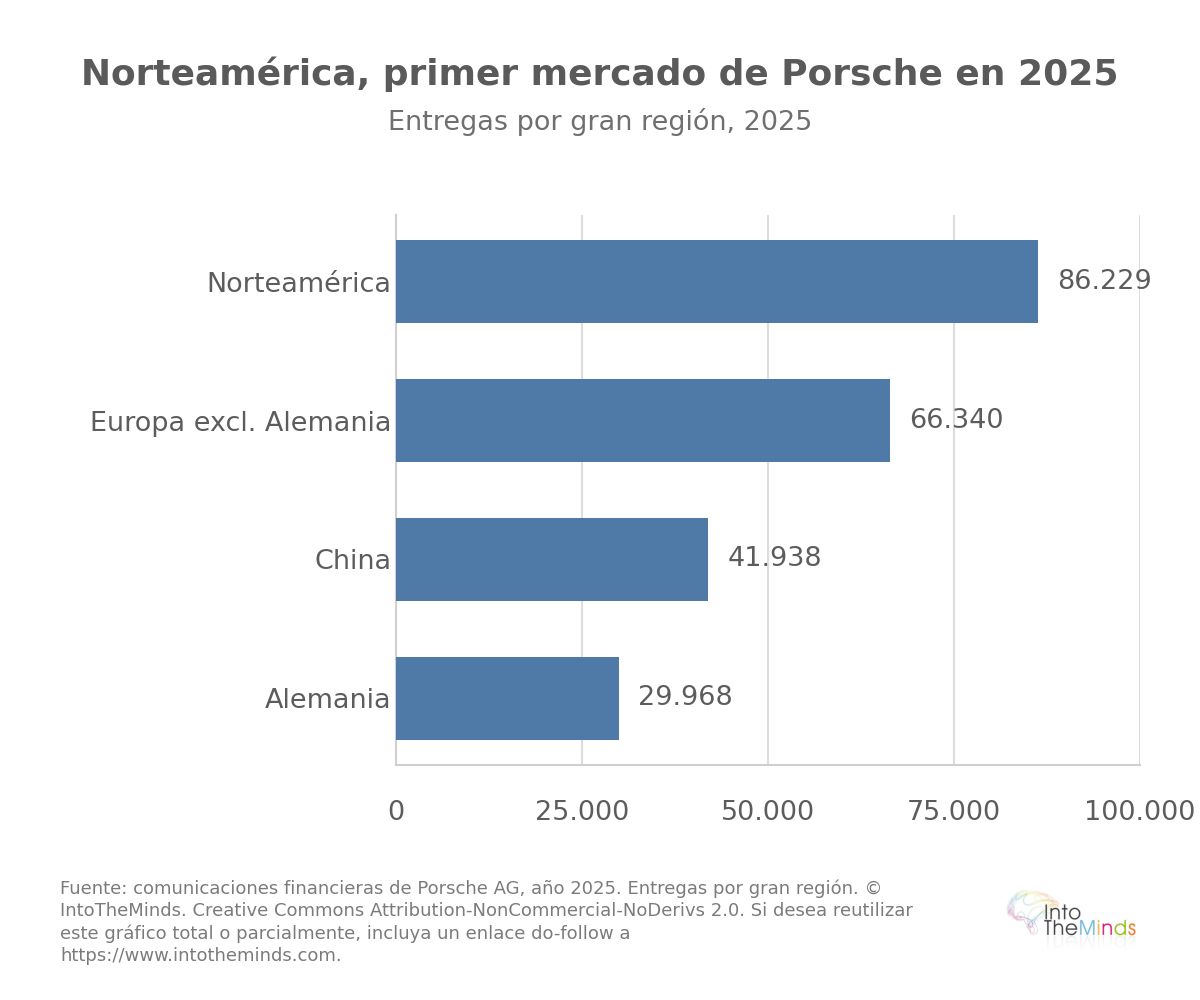

China, which represented nearly 100,000 vehicles at the start of the decade, accounted for only 41,938 units in 2025 and started 2026 with just 7,519 units in the first quarter. The implicit scenario is that China will remain permanently relegated to a niche outlet, at around 30,000 vehicles annually according to internal projections.

The corollary is the shift toward North America, which became the “default” leading market in 2025 with 86,229 vehicles. But this pivot exposes Porsche to structural vulnerability: the absence of any production in the United States had already cost more than €500 million in tariffs by the end of September 2025 and around €700 million over the full year. The success of this scenario will depend as much on the ability of North America and Europe to compensate for the Chinese losses as on the evolution of US trade policy, an external factor over which Porsche has no direct control.

Scenario 3: technological coverage across three powertrain types

The third axis is one of claimed flexibility: maintaining combustion, hybrid, and fully electric powertrains across all segments until the late 2030s, after postponing several electric models and extending the lifespan of combustion engines. This approach is a bet on uncertainty: unable to predict the pace of the transition, Porsche is keeping options open on all fronts.

The growth of electrification in the mix (approximately 34% of global deliveries electrified in 2025, including around 22% fully electric) shows that demand exists, but at a slower pace than anticipated. This scenario contains its own contradiction: maintaining three powertrain families runs counter to the objective of simplification and streamlining. Chinese competition is rising precisely in the premium electric segment that Porsche is slowing down in; players such as Xiaomi, whose SU7 openly draws inspiration from the Taycan, illustrate a new threat in the very field where Porsche pioneered 800-volt technology.

The overall interpretation: a bet on shrinking toward excellence

The three scenarios are not mutually exclusive. Leiters’ strategy is to pursue them simultaneously:

- refocusing and moving further upscale

- a geographic pivot toward North America and Europe

- a more cautious and rational technological coverage than before.

The common thread is a bet on shrinking toward excellence. It also means abandoning the race for volume that had transformed Porsche from a sports-car manufacturer into a “mainstream” automaker. Porsche must return to a logic centered on desirability and margins.

The main uncertainties remain execution in an unfavorable environment, social tensions linked to several thousand threatened jobs, and Leiters’ ability to build a management team aligned with his vision. Several executive board members are considered close to Oliver Blume, which weakens implementation coherence. The Capital Markets Day in autumn 2026 will be the first full-scale test of the credibility of this strategy.

Here is the English translation, preserving HTML structure and all links/images:

FAQ: the questions you are asking

Why did Porsche’s operating margin fall to 1.1% in 2025?

Three factors combined in 2025. The collapse of sales in China (41,938 deliveries, -26% compared to 2024) deprived Porsche of its historic number one market. US tariffs represented around €700 million in additional costs over the year. Finally, the strategic shift in electric plans generated an exceptional €1.8 billion charge linked to the postponement of several all-electric models. Total exceptional costs in 2025 reached approximately €3.8 billion.

What is Michael Leiters’ strategy to turn Porsche around?

Leiters is implementing a structural downsizing: reducing the size and complexity of the company so that it remains profitable even at a volume of 200,000 vehicles per year. The internal target is an operating margin of 10–15% by the end of the decade. This involves divesting non-core assets (Bugatti Rimac, Cellforce, Porsche eBike Performance), streamlining the executive board and management structure, and moving upmarket toward higher-margin models above the Cayenne. A full strategic update is expected at the Capital Markets Day in autumn 2026.

Will Porsche abandon electric vehicles?

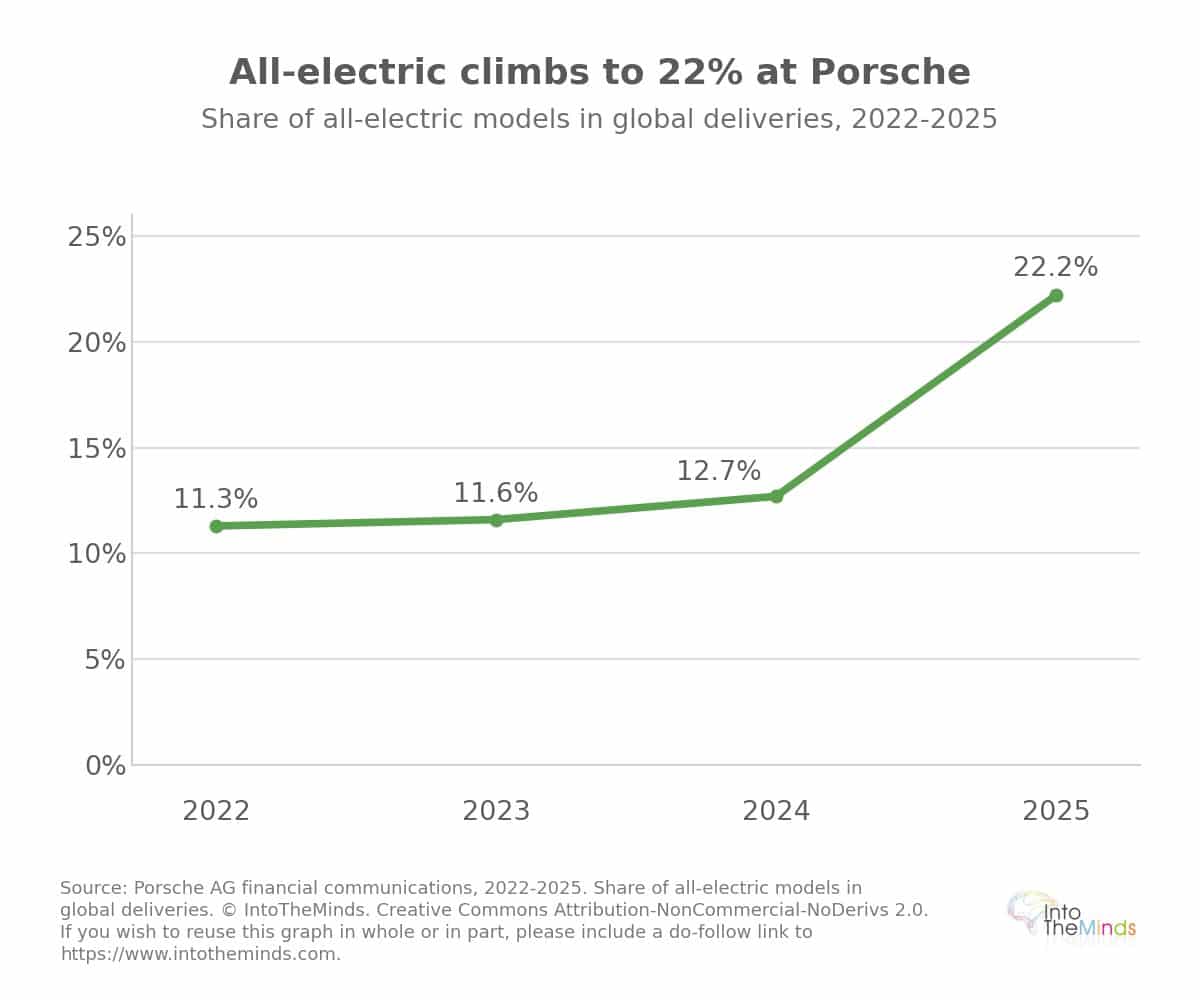

No. Porsche’s product strategy maintains all three propulsion types—internal combustion, plug-in hybrid, and fully electric—across all segments until the late 2030s. What Porsche has abandoned is the target of 80% fully electric sales by 2030, which was deemed unattainable. In 2025, around 34% of global deliveries were electrified, including about 22% fully electric. In Europe, electrified models exceeded 50% of deliveries for the first time in 2025.

How can a company analyze its own strategy in the face of such a crisis?

Porsche’s crisis highlights the importance of continuous strategic monitoring of key markets and a deep understanding of customer expectations by geographic segment. A B2C market study helps identify early warning signals of demand shifts before they translate into lost sales. In Porsche’s case, dependence on a single market (China accounted for up to a quarter of global sales) and a single production site in Germany represented measurable risks that regular market analysis could have quantified earlier.

What strategic lessons can other premium companies learn from Porsche?

Porsche’s case highlights several typical risks of volume-driven premium strategies. Geographic concentration of sales (China) and production (Germany) creates a dual vulnerability to external shocks. The pursuit of volume can erode brand desirability, a risk already identified by management as early as 2015. Finally, simultaneous technological bets (electric, batteries, e-fuels, software) disperse resources and increase organizational complexity. Regular B2B market studies and brand awareness surveys help objectively track brand equity before financial indicators become alarming.

What is the impact of the Porsche crisis on the Volkswagen Group?

The impact is substantial. Porsche historically accounted for around half of Volkswagen Group’s operating profit. Porsche’s restructuring cost the group €5.1 billion in operating result in 2025, reducing VW’s expected margin from 4–5% to 2–3%. In Q1 2026, the group reported €75.66 billion in revenue (-2.5%) and a 3.3% margin, with global deliveries down 4% to 2.05 million vehicles. The group aims to reduce production capacity by an additional one million units and cut around 50,000 jobs in Germany by 2030.

![Illustration of our post "Dark stores: statistical analysis and outlook [Study]"](/blog/app/uploads/dark-store-120x120.jpg)