The spirits market is struggling, but some segments, like the whisky market, are holding up. Projections for the whisky market up to 2034 are largely positive, but they mask significant disparities by country and product type, which we analyze for you in this article.

Le whisky remains the leading spirit sold in supermarkets and hypermarkets, but since 2022 the market has entered a phase of structural contraction confirmed by the latest available data. Between an aging customer base, fiscal pressure, accelerated premiumization, and the rise of local production, the global whisky market is undergoing profound reorganization. Our [market research agency provides a comprehensive analysis based on the latest available market data.

Contact the IntoTheMinds institute

Key takeaways

- The global whisky market was valued at USD 92.89 billion in 2025 and is expected to reach USD 180.20 billion by 2034, representing an average annual growth rate of 7.68%.

- In France, the whisky market in mass retail has recently declined to around €2 billion, marking a decrease both in value and volume.

- Scotland exported €6.55 billion worth of Scotch whisky in 2023, accounting for 77% of Scottish food exports.

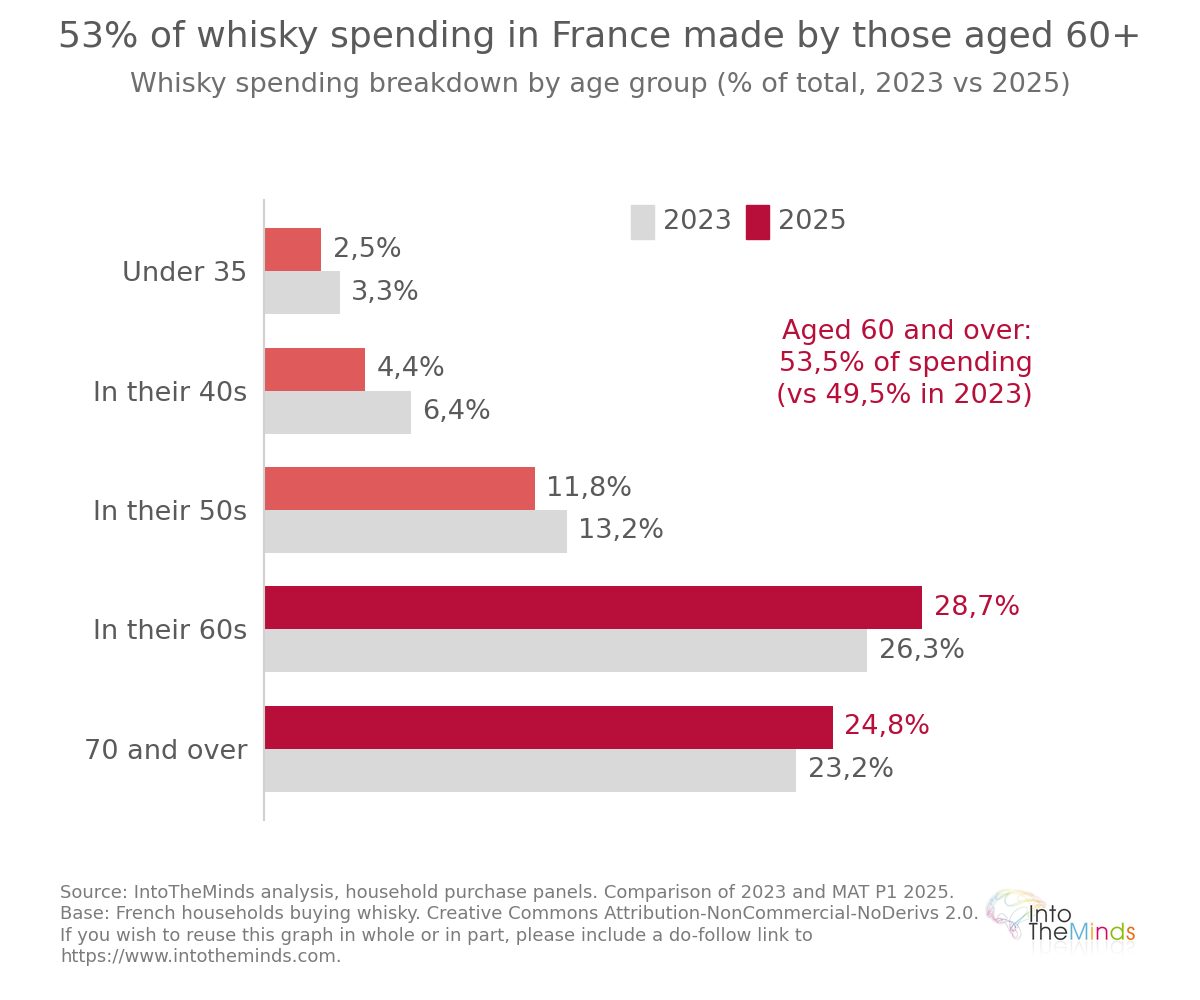

- Consumers aged 60 and over represent a dominant and growing share of whisky spending in France. The customer base is therefore aging.

- French whisky is experiencing double-digit volume growth in supermarkets and hypermarkets, although its market share remains marginal compared with imported whiskies.

- Premiumization is driving value growth: premium whiskies contributed 43% of total growth contribution.

Analysis of the global whisky market

The global whisky market is one of the strongest segments within the spirits market. Its resilience is supported by several structural factors:

- sustained premium demand

- consumption geography expanding toward Asia and emerging markets

- the ability of major brands to maintain pricing power even during economic slowdowns.

Key figures for the global market

In 2025, the value of the global whisky market reached USD 92.89 billion. North America was the dominant region with a 32.97% market share that same year. The premium and ultra-premium segments are driving value growth across all geographies, while volume growth remains more modest.

The five players structuring global supply are:

- Diageo

- Pernod Ricard

- Beam Suntory

- Brown-Forman Corporation

- The Edrington Group

These groups control the most widely distributed brands internationally, from Scottish blends to American bourbons.

The table below summarizes the main size and growth indicators of the global whisky market:

| Indicator | Value | Year / Period |

|---|---|---|

| Global market value | USD 92.89 billion | 2025 |

| Global market value | USD 99.73 billion | 2026 |

| Projected global market value | USD 180.20 billion | 2034 |

| Projected annual growth | 7.68% | 2026-2034 |

| North America market share | 32.97% | 2025 |

| Scotch whisky exports | €6.55 billion | 2023 |

| Number of bottles exported from Scotland | 1.35 billion/year | 2023 |

Developments and projections through 2034

The 2026-2034 forecast period suggests a doubling of the global whisky market value in less than a decade. This scenario is mainly based on 3 drivers:

- the rise of Asian markets

- continued premiumization of product ranges

- product innovation (special cask finishes, limited editions, niche single malts).

China illustrates this trend particularly well. In 2024, national disposable income per capita reached USD 5,747, with annual nominal growth of +5.3% and GDP growth of 5%. These economic indicators are supporting stronger demand for premium whiskies, especially Scotch whisky, Irish whiskey, and Japanese whisky.

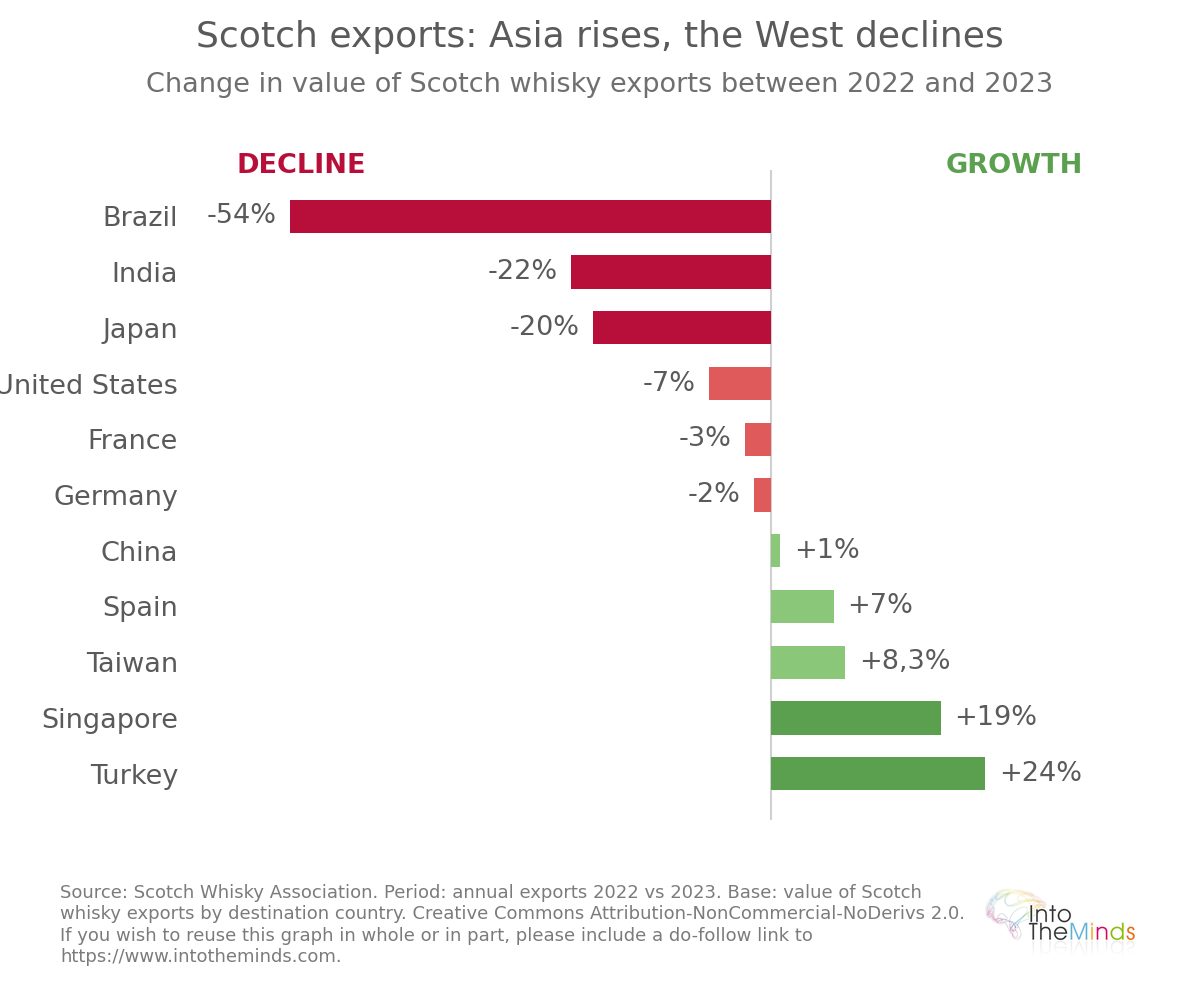

Singapore is also showing remarkable momentum (see chart below): Scotch exports to this market increased by +19% in 2023 compared with 2022, reaching €443.8 million. Taiwan, with €443.4 million (+8.3%), and Turkey (+31% in volume to 41 million bottles), confirm that the center of gravity of global consumption is gradually shifting toward Asia and certain emerging markets.

Whisky market segmentation

The diversity of whisky types is one of the market’s defining characteristics. Each geographical origin corresponds to distinct production standards, different consumer profiles, and specific pricing dynamics. This product-type segmentation is essential to understanding trade flows and brand strategies.

The different categories: Scotch, American, Irish, Japanese, and Canadian whisky

Scotch whisky remains the most powerful segment globally. Scotland had 147 distilleries in 2023 and generated 41,000 direct jobs and 25,000 indirect jobs, according to the Scotch Whisky Association. The earliest written record of Scottish malt spirit dates back to 1494, giving Scotch unique historical legitimacy. Appellation rules require a minimum aging period of 3 years in wooden casks and a minimum alcohol content of 40%.

American whiskey (mainly bourbon) recorded +10.5% revenue growth in the United States in 2022, making it one of the five fastest-growing spirits categories that year. In France, this segment represented 13% of sales in 2021, with +17.1% value growth, before slowing in 2022 (-10.5% in value, -12% in volume, down to €271 million). Jack Daniel’s holds 86% of the value market share among American whiskies in France. The United States also counted 200 whisky distilleries in 2022, reflecting a dense and diversified production landscape.

Irish whiskey and Canadian whisky occupy more modest but growing positions in several markets. In France, Canadian whisky represented 800,000 liters in 2021, with Sam Barton holding 90% of this sub-segment. Japanese whisky, meanwhile, enjoys strong premium appeal internationally, with sustained demand in Asia-Pacific and Europe.

The market is also segmented by flavor profile:

- Unflavored / smooth

- Smoky (peated)

- Spicy

- Botanical

- Fruits and berries

Impact of geographical origin on demand and pricing

Geographical origin directly shapes price positioning. In France, in 2025, supermarket prices vary depending on brands and origins: Ballantine’s (Scotch) is priced at €21.01/liter, Grant’s (Scotch) at €17.95/liter, and Label 5 (Scotch) at around €18/liter. The average whisky price per liter in French supermarkets and hypermarkets reached €20.61 in rolling annual sales in 2025, slightly up from €20.22 in 2021.

At the other end of the spectrum, premium and ultra-premium whiskies reach price levels incomparable with the mass market. In specialty liquor store chains such as Nicolas (France), prices ranged from €15.50 to €1,500 per bottle in 2025. This wide range illustrates the coexistence of two market logics: a pressured mainstream consumption base and a high-end segment that is more resilient during crises.

Major trends in the whisky market

Premiumization has been the most structuring trend in the global whisky market over the past decade. It is reflected in a shift of consumers toward higher-end offerings, and in market value growth that outpaces volume growth.

Moving upmarket: from standard to premium and ultra-premium

In France, premium whiskies contributed 43% of total market growth in 2021, according to data from William Grant & Sons. Single malts recorded +11.2% value growth in the same year. This trend affects all regions: in North America, Europe, and Asia-Pacific, affluent urban consumers and high-income young adults are gradually moving away from lower-cost spirits toward premium offerings perceived as connoisseur products.

Price segmentation distinguishes four levels:

- Economy: entry-level, highly promotion-sensitive (26% of 12-year blended whisky sales in France were on promotion in 2024)

- Mid-range: core mass market segment, under structural pressure

- Premium: strongly growing segment, driven by tasting culture

- Ultra-premium / luxury: most dynamic in value terms, including limited editions and aged single malts

Product innovation and specialized cask finishes

Producers are multiplying innovation strategies to generate additional value. Specialized cask finishes (sherry, port, Sauternes, exotic woods) create distinctive flavor profiles and justify higher price points. Limited series and small-batch releases respond to demand for exclusivity among highly engaged consumers.

Some distilleries are also launching whisky-based spirits with reduced alcohol content to meet new consumption expectations. This reflects the search for new consumption occasions, particularly among consumers less accustomed to high alcohol strength. The No/Low trend reshaping the entire alcoholic beverages market is discussed in detail in our article on the evolution of alcohol consumption and the de-alcoholization market.

Evolution of consumer behavior

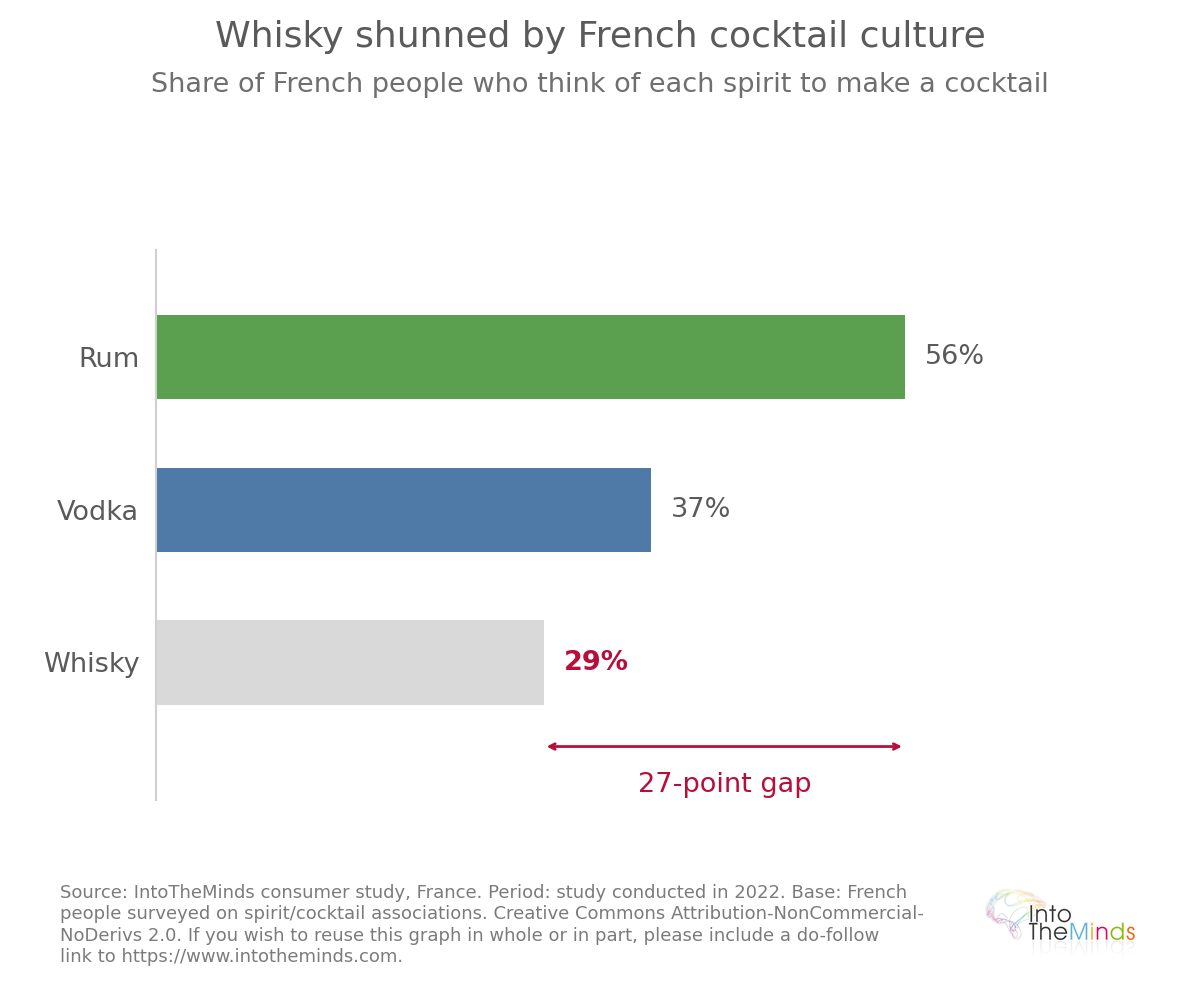

Whisky suffers from a weak image among younger generations. In 2024, a survey showed that only 29% of French consumers associated whisky with cocktails, compared with 56% for rum and 37% for vodka (see chart below). This disadvantage in cocktail culture partly explains the difficulty in attracting new consumers under 35. They accounted for only 2.5% of whisky spending in 2025.

The whisky market in France

France holds a unique position in the global whisky market: the world’s largest importer of Scotch whisky by volume in 2023 (174 million bottles), second-largest destination by value (€556.5 million), but also a domestic market in structural decline since 2022. This duality requires closer analysis.

A market in contraction since the post-pandemic peak

The pandemic artificially boosted retail sales, with around 60% of whisky consumption shifting from the on-trade (bars, restaurants) to the off-trade (supermarkets, hypermarkets, e-commerce).

The table below shows how rapidly sales have deteriorated over recent years:

| Period | Revenue (€bn) | Value change | Volume change |

|---|---|---|---|

| 2021 | 2.19 | +5.6% | +3.8% |

| 2022 | 2.30 | -3.5% | -8.8% vs 2021 |

| 2023 | 2.25 | -2.4% | -5.6% |

| 2024 | 2.04 | -3% | -5% |

| 2025 | 1.90 | -4% | -4% |

An accelerating aging of the customer base?

The demographic challenge of whisky in France is well documented. Consumers aged 60+ accounted for 49.5% of spending in 2023 (people in their 60s: 26.3%, 70+ : 23.2%), and as shown in the chart below, this share increased to 53.5% in 2025 (28.7% in their 60s, 24.8% aged 70+).

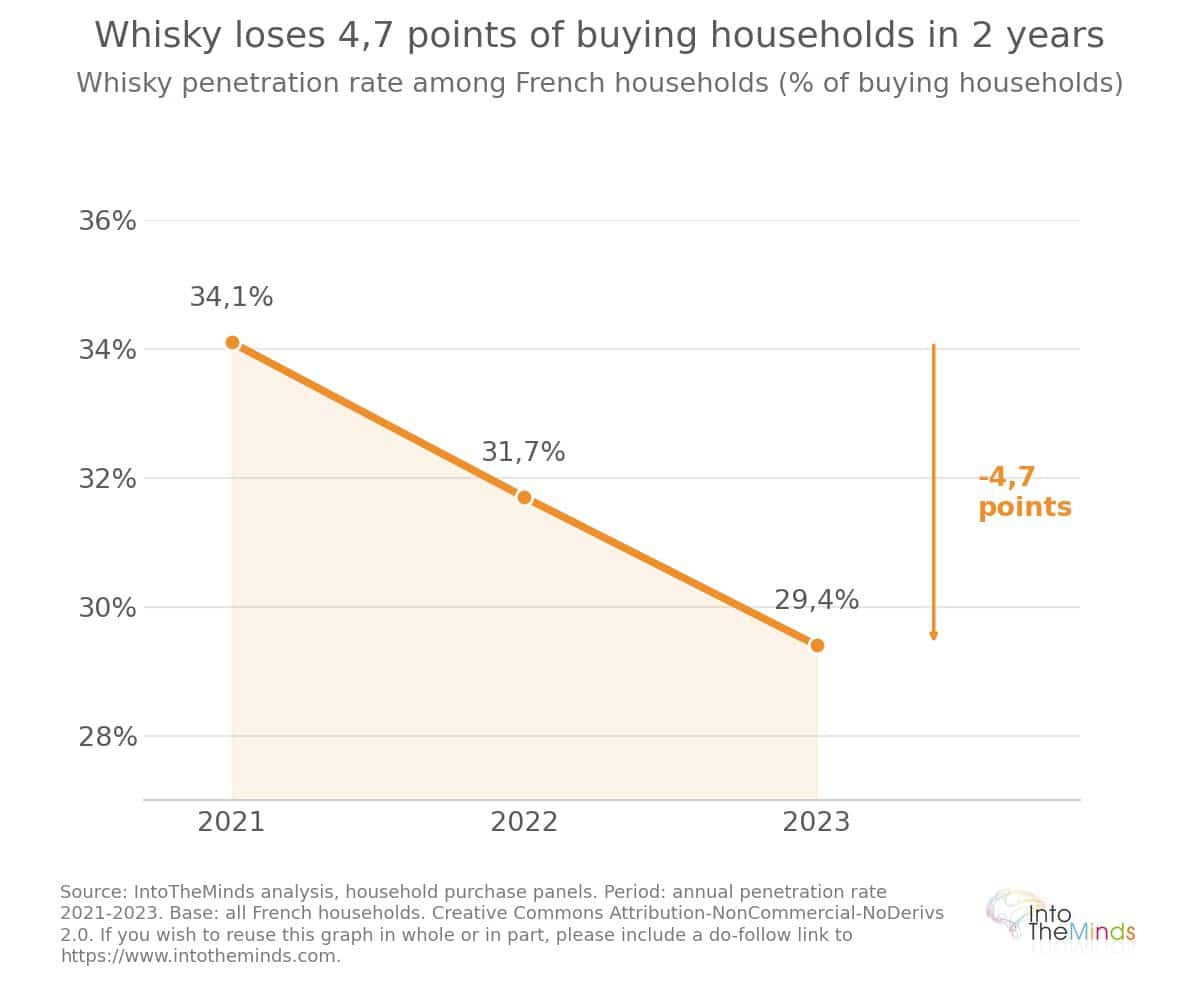

At the opposite end, consumers under 35 accounted for only 2.5% of spending in 2025, down from 3.3% in 2023. Overall penetration is steadily eroding: 34.1% in 2021, 31.7% in 2022, 29.4% in 2023. This trend is likely transferable to other mature European markets where white spirits are gaining share through cocktail culture.

Distribution channels and commercial strategies

Whisky distribution in France is dominated by mass retail, but the landscape is diversifying under the influence of digital channels and specialist networks.

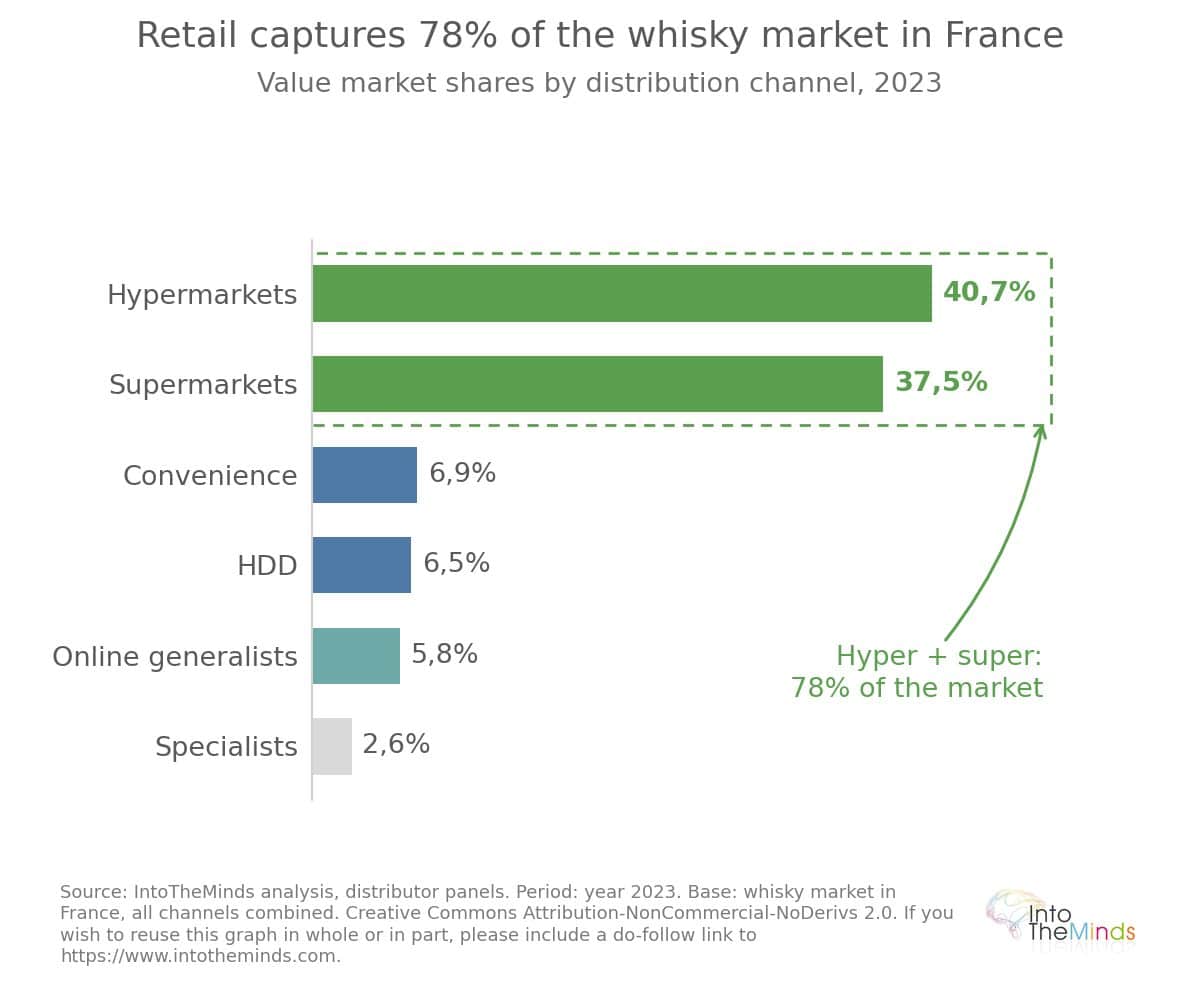

Mass retail: dominant but under pressure

In 2023, hypermarkets held a 40.7% market share in value (+0.4 pts), and supermarkets 37.5% (+0.9 pts). Convenience stores (6.9%), discount retailers (6.5%), online generalists (5.8%), and specialists (2.6%) complete the picture. Mass retail therefore captures 78.2% of value sales, making the market highly sensitive to promotional strategies.

Promotional pressure is significant: in 2024, 26% of sub-12-year blended whisky sales in France were sold on promotion, compared with 23% for all spirits. This dependence on promotions weakens brand value perception and erodes margins.

Online sales and e-commerce: a trend to watch

E-commerce and click-and-collect continue to grow in whisky sales in France, attracting a younger customer base than physical stores. Click-and-collect accounts for 90% of online sales. The online whisky buyer at Monoprix had an average age of 43 in 2025, compared with an older in-store clientele.

Specialist retailers provide an additional layer. The Nicolas chain, for example, listed 120 whisky references across 480 stores in 2025, with prices ranging from €15.50 to €1,500. Its website conversion rate reached 10% in 2025, with 60–70% of sales delivered. La Maison du Whisky counted 450,000 online customers in 2025, with 1.5 online purchases per customer per year, and e-commerce representing 8–10% of total sales.

For companies seeking to evaluate their positioning in these channels or measure customer satisfaction, a customer satisfaction survey can provide valuable insights into expectations across online and offline buyers.

Growth drivers and market constraints

The whisky market is shaped by opposing forces that explain the divergence between value growth (driven by premiumization) and volume contraction in mature markets.

Growth drivers: global exports and premium consumption

Key positive drivers include:

- Rising disposable incomes in emerging markets (China, India, South Korea, Turkey), supporting demand for higher-quality products

- Growing interest in aged expressions, limited editions, and high-value single malts

- Expansion of Scotch whisky exports: 43 bottles shipped every second to 160 markets in 2023

- Development of e-commerce, expanding access to premium ranges

- Cultural appeal of whisky as a tasting and gifting product, especially in Asia

- Product innovation (cask finishes, flavored whiskies, low-alcohol formats)

Major constraints: aging cycles, regulation, and taxation

Structural constraints are equally significant. The first is inherent to the product: minimum aging requirements of 3 years (often much longer in premium segments) limit supply flexibility. Producers cannot quickly adjust output to demand shifts, creating inventory pressure and working capital intensity.

Taxation heavily impacts retail prices. In France, taxes (excise duties, VAT, social contributions) account for around 74% of the retail price of whisky. Across the European Union, total tax burdens exceed 50% of retail prices for spirits in many member states. This reduces affordability and limits volume growth. For comparison with similar spirits categories, our analysis of the cognac market provides additional context.

Environmental pressures are a third constraint. Distillation is energy-intensive, and climate variability affects grain yields. The world’s leading malt producer, generating €2.2 billion in revenue in FY 2024–2025 across 41 malt houses in 20 countries, is diversifying beyond beer and whisky (which still represent 99% of sales), exploring alternatives such as cocoa substitutes and malt-based soft drinks.

Regional outlook and expansion opportunities

The whisky market geography is shifting. Mature markets (France, UK, US) are consolidating, while new growth drivers emerge in Asia and parts of the Middle East.

The rise of French whisky: a fast-growing niche

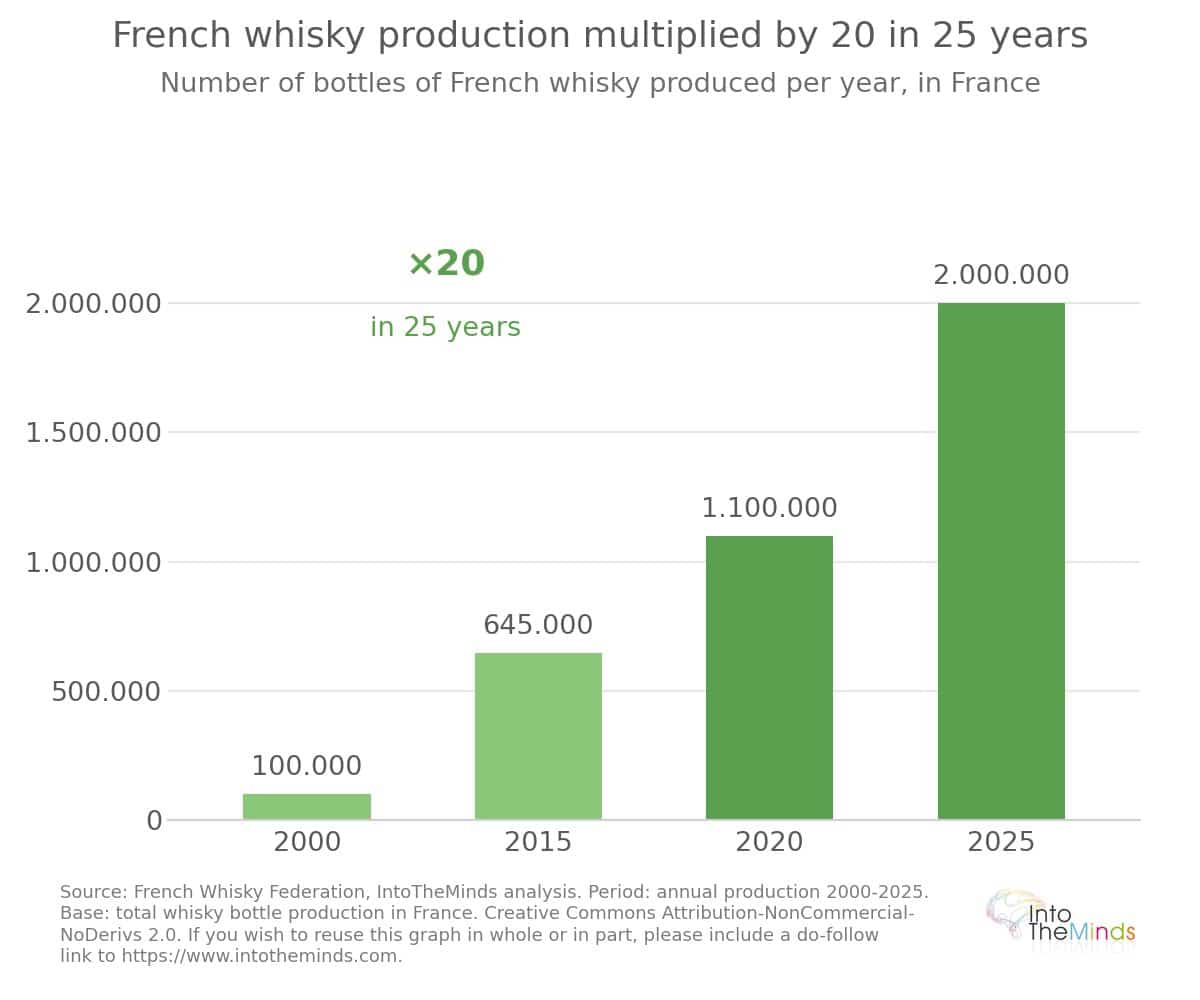

France is no longer only a consumption market; it is now a whisky-producing country. The number of distilleries grew from around ten in the early 2000s to roughly 150 in 2025 (70 registered by the French Whisky Federation in 2023). As shown below, production has steadily increased over the past 25 years:

- 100,000 bottles in 2000

- 645,000 in 2015

- 1.1 million in 2020

- 2 million in 2025, including 1.2 million sold in mass retail

In 2025, French whiskies accounted for 0.85 million liters in mass retail, with +52.5% growth over 12 months, in a market that overall declined by -4.4%. Their market share remains small (1% of volume), but the momentum is unmatched within the category. Whisky consumption in cafés, hotels, and restaurants increased by +9.4% between 2023 and 2024.

French distilleries largely adopt a premium strategy. Warenghem (370,000 bottles annually, 60% sold in supermarkets) and Maison Bellevoye (market leader in the segment) illustrate two different models: one anchored in mass retail, the other focused on specialist channels and innovation.

Emerging markets and global growth potential

Asia-Pacific offers the highest growth potential for the global whisky market. Singapore (+19% Scotch import value in 2023), Taiwan (+8.3%), Turkey (+31% volume growth), and China (+1% value despite a challenging macroeconomic context) illustrate this trend.

India deserves special attention: with 167 million bottles of Scotch imported in 2023 (second globally by volume), it represents a massive market, although volumes declined by 24% that year compared with 2022. Rising disposable incomes and rapid urbanization continue to support long-term structural demand.

For companies seeking to assess positioning or enter new segments, a B2B market research study or a B2C market research study conducted by IntoTheMinds can support data-driven decision making.

FAQ: Questions you may have

What is the whisky market in France?

The whisky market in France was worth €1.90 billion in 2025, down 4% in both value and volume compared to the previous period. France is the world’s largest importer of Scotch whisky by volume (174 million bottles in 2023) and the second-largest market by value for Scottish exports (€556.5 million in 2023). Whisky accounts for 43% of spirit sales in French grocery retail in value terms, making it the dominant category ahead of rum, aniseed spirits, and vodka. For a deeper analysis tailored to your business, IntoTheMinds offers bespoke B2C market research.

How large is the global whisky market?

The global whisky market was valued at USD 92.89 billion in 2025 and is expected to reach USD 99.73 billion in 2026, and USD 180.20 billion by 2034. The compound annual growth rate (CAGR) over 2026–2034 is projected at 7.68%. North America is the dominant region with a 32.97% market share in 2025, while Asia-Pacific shows the strongest growth outlook in the medium term.

Is the whisky boom over?

In mature markets such as France, the whisky market has been undergoing a structural contraction since 2022. Penetration in France fell from 34.1% in 2021 to 29.4% in 2023, and retail turnover has declined annually since the post-pandemic peak. Globally, however, growth remains positive, driven by premiumisation and expansion in emerging Asian markets. The market is not stagnating overall; rather, it is restructuring: value growth exceeds volume growth, and entry-level segments are losing share to premium and ultra-premium categories.

What factors influence whisky prices?

Several factors determine whisky pricing. Ageing time is primary: a 18-year-old single malt ties up capital for nearly two decades, justifying significantly higher prices than no-age-statement blends. Geographic origin (Scotch, bourbon, Japanese whisky) and production type (craft vs industrial distilleries) also matter. Taxation is highly significant: in France, taxes account for approximately 74% of retail price. Finally, scarcity (limited editions, single cask releases) and brand reputation are key price drivers in premium and ultra-premium segments. A survey study can help measure consumer price sensitivity in a given market.

How does French whisky perform compared to Scotch and bourbon?

French whisky is the fastest-growing segment in France in 2025, with +52.5% volume growth over 12 months in retail distribution. Its market share remains small (1% of volume versus around 80% for Scotch), but its trajectory is unmatched in the category. French distilleries generally position themselves in the premium segment, with prices ranging from €9.90 for entry-level blends to over €150 for prestige expressions. Scotch, by contrast, declined by -4.4% in volume over the same period. US bourbon, after strong growth in 2021, declined in 2022 and is now seeking recovery through mixology and premiumisation. To analyse your brand positioning, an brand awareness study by IntoTheMinds can provide precise consumer perception insights.

What are the main distribution channels for whisky in France?

Large-scale retail dominates with 78.2% market share in value terms in 2023 (hypermarkets 40.7%, supermarkets 37.5%). E-commerce represented 4.5% of sales in 2025 (€86.8 million), with click & collect accounting for 90% of online purchases. Specialist retailers (such as Nicolas with 480 stores and La Maison du Whisky with 450,000 online customers) complement the market, focusing mainly on premium and ultra-premium segments. Online now accounts for around 24% of spirits purchasing in France (2022), a share that continues to grow.

![Illustration of our post "Human resources: state of process digitalisation [Study]"](/blog/app/uploads/concept-shapes-120x90.jpg)