An analysis of the latest figures on the spirits market highlights the challenges facing this sector. In this article, we identify four areas of innovation for companies operating in this market.

Le secteur des spiritueux traverse une période de transformation profonde. Après l’euphorie post-Covid qui avait dopé les ventes, l’industrie fait face à de nouveaux défis. La consommation d’alcool recule, particulièrement chez les jeunes générations, tandis que les tensions géopolitiques perturbent les échanges commerciaux. Dans le cas de nos market analysis activities, we had already highlighted the difficulties in the cognac market. In this article, we take a broader perspective and focus on the spirits segment as a whole.

Contact the IntoTheMinds institute

Key takeaways

- The global spirits market is slowing down after post-pandemic growth

- Major groups such as Pernod Ricard and LVMH are reporting significant revenue declines

- France remains a strategic market despite a 2.6% drop in consumption in 2024

- Innovation is focused on four areas: moderation, cocktailization, premiumization, and sustainability

- French spirits exports fell by 17% in 2025, to €3.7 billion

A spirits sector under pressure

It is no understatement to say that the spirits industry is going through a difficult period. The performance of leading companies in the sector illustrates this. Take Pernod Ricard, for example: its revenue fell from €11.5 billion in 2023/2024 to €10.96 billion in 2024/2025, a decline of 3%. The trend even accelerated in the first half of 2025/2026, with a 15% drop to €5.25 billion.

This deterioration also affects LVMH, whose wines and spirits division declined by 11% over the first nine months of 2024, reaching €4.193 billion. These figures can be interpreted as reflecting a normalization of the market after the rapid expansion observed during the health crisis.

Several factors explain this development:

- the decline in alcohol consumption, particularly among 18–34-year-olds. For example, in France, the share of young adults who do not buy alcohol for home consumption jumped by 50% between 2020 and 2024.

- the slowdown of the Chinese economy

- inventory adjustments in the United States

French exports under pressure

International trade in spirits is particularly sensitive to current geopolitical tensions. The French wines and spirits sector recorded export revenue of €14.3 billion in 2025, down 8% year-on-year. Spirits alone declined by 17% to €3.7 billion.

The United States, the leading export market, saw a 21% drop to €3 billion for all French wines and spirits. To make matters worse, China also disappointed with €767 million, a decline of 20%. Only the European Union held up better, with €4.1 billion and a limited decline of 1%.

| Export market | Revenue 2025 (€m) | Change vs 2024 |

|---|---|---|

| United States | 3,000 | -21% |

| European Union | 4,100 | -1% |

| United Kingdom | 1,600 | -4% |

| China | 767 | -20% |

| Japan | 648 | Stable |

However, some emerging markets offer encouraging prospects. South Africa grew by 22% to €182 million in 2025, while the Philippines jumped by 20% to €13 million. These more diffuse growth drivers only partially offset the difficulties in major traditional markets.

The French market is losing momentum

France remains strategically important in the global spirits industry. In 2025, Diageo recalled that it is the second-largest whisky-consuming country in the world, with whisky accounting for 33% of spirits consumed in the country. However, signs of fragility are accumulating.

In 2024, spirits consumption in France fell by 2.6% in pure alcohol terms. In retail, volumes dropped to 247 million liters (-3.8%) and value to €4.9 billion (-3.6%). In cafés, hotels, and restaurants, volumes decreased by 2% to 20.8 million liters.

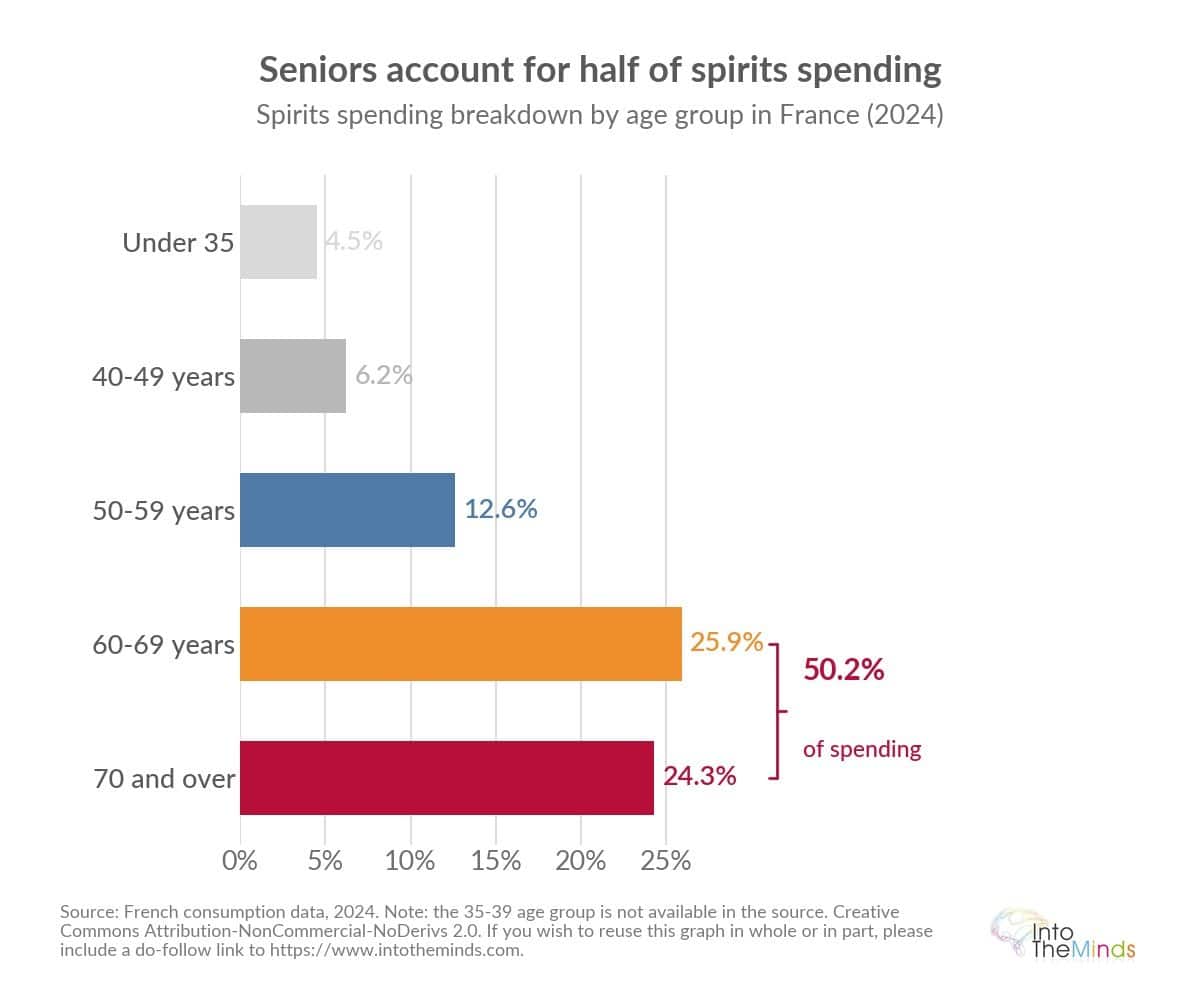

This transformation is accompanied by an aging customer base. Spending on spirits is highly concentrated among seniors: people in their sixties account for 25.9% of spending and those aged 70 and over for 24.3%, compared to just 4.5% for those under 35 in 2024.

Despite these challenges, the sector retains its economic importance. It generates €17 billion in GDP and supports more than 151,000 jobs in France. Across the wines and spirits sector, total revenue reaches €32 billion, including €16 billion in exports, supporting 600,000 jobs.

Winning and losing categories

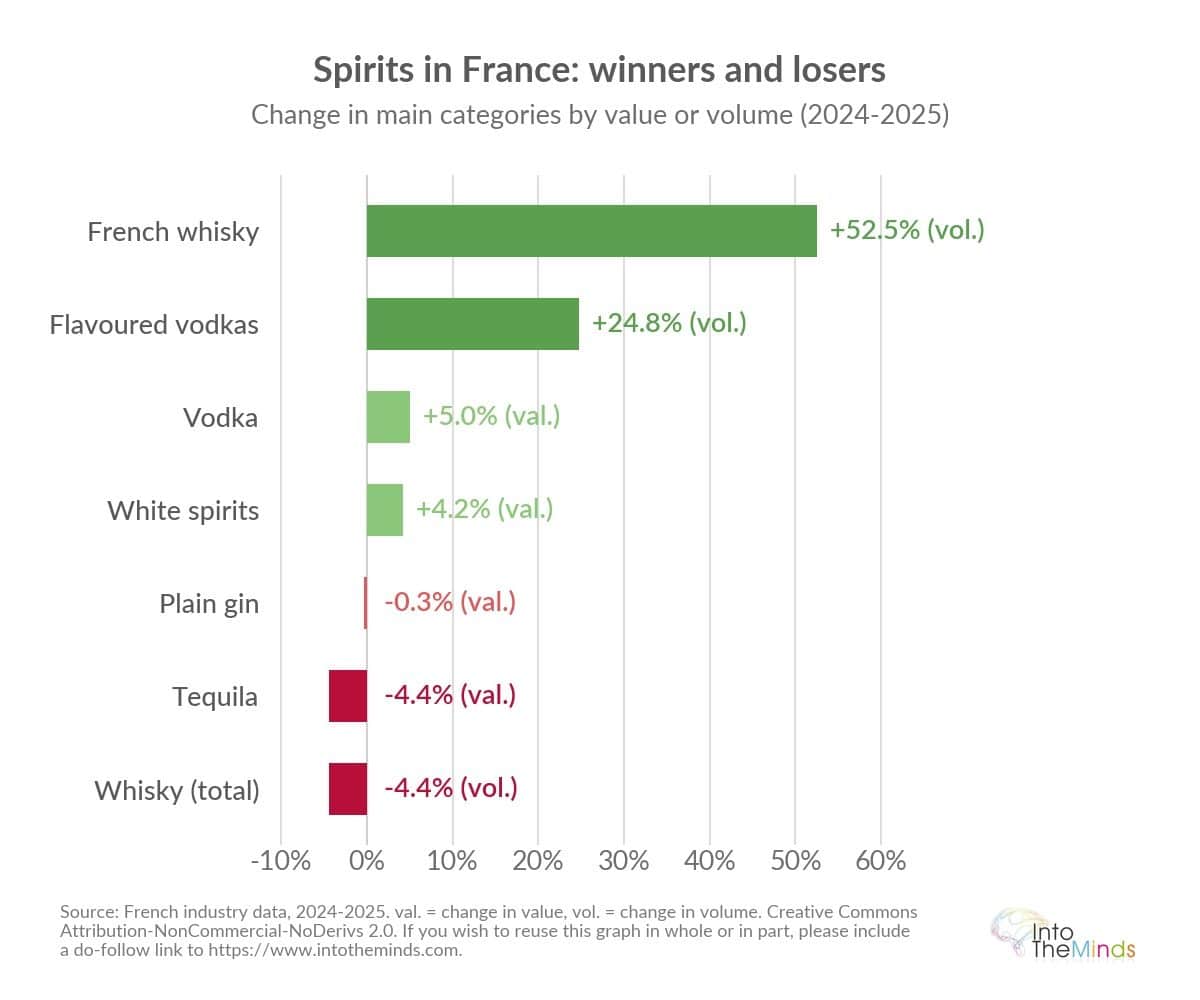

Analysis of the French market reveals contrasting dynamics depending on the spirits category. Whisky remains dominant with €2.3 billion in revenue in 2022, but its leadership is eroding. In 2025, the whisky market in retail declined again to 91.5 million liters (-4.4%).

The standout trend comes from French whisky, which reached 0.85 million liters and +52.5% in volume in 2025, with nearly 150 distilleries recorded. E-commerce is also growing, with €86.8 million in online whisky sales (+3%) in spring 2025.

The vodka and white spirits categories are more resilient. In 2025, white spirits excluding white rum accounted for €615.7 million and grew by 4.2% in both value and volume. Vodka alone reached €471.8 million (+5% in value and +5.3% in volume), now representing 28% of spirits volume.

Rum remains one of the biggest long-term winners. Between 2019 and 2023, the category grew by 16% in volume and 32% in value. Flavored rums surged by 197% in volume, aged rums by 38%, and amber rums by 32%. Rums from French overseas territories account for 50.9% of volumes, with Martinique leading at 28.7%.

Innovation at the heart of industry strategy

Innovation is, as often, a way for companies to maintain growth and protect margins. We have identified four main innovation drivers in the spirits market.

No-Low (alcohol-free or low alcohol)

The first area concerns reducing alcohol content. We have already covered this in our No/Low market analysis. In France, 12.5% of spirits revenue already came from alcohol-free or low-alcohol products in 2024. For example, Tanqueray 0.0 now represents 20% of the brand’s volumes.

Rémy Cointreau (via RC Ventures) took a majority stake in JNPR, a French alcohol-free pioneer, in 2025. This trend is even reaching traditionally high-alcohol categories. Maison Bellevoye launched in 2026 a whisky naturally at 20% ABV, using an innovative infusion process.

“Cocktailization” and flavoring

Cocktail culture is a key driver of innovation. Globally, nearly 50% of 18–29-year-olds prefer celebrating special occasions with a cocktail rather than champagne. Spritz leads their preferences at 37%, followed by Mojito (33%) and Piña Colada (21%).

In France, this dynamic now permeates all categories. In cafés, hotels, and restaurants, the Spritz saw its market share in value increase by 32% in 2024. As for flavored vodkas, they reached 1.8 million liters in 2025, up 24.8%. This “cocktailization” helps broaden the customer base beyond traditional consumption patterns.

Premiumization

The market no longer simply contrasts entry-level products with luxury. It is becoming polarized between access, premium, super-premium, and niche innovations. Gin illustrates this evolution. In 2023, the category represented €148.5 million in France, up 17.4%. But in 2024, standard gins fell back to €110.5 million, remaining almost stable, while flavored gins continued to grow to €7.8 million (+6.4%).

Tequila is following a similar trajectory. Despite a 4.4% decline in 2024 to €13.7 million in French retail, industry players still see strong potential. Diageo highlighted a 14% growth in tequila sales in France in 2025.

Industrial and environmental innovation

Innovation is no longer limited to the liquid itself but also includes packaging, logistics, and carbon footprint. Absolut Vodka, which produces 600,000 bottles per day in Sweden, aims for zero impact by 2030. The brand has already reduced its water consumption by 30% since 2003 and its energy consumption by 50% since 2004.

Pernod Ricard has tested more than 3 million bottles of Jameson made from 100% recycled glass produced using biofuel, reducing the carbon footprint of the glass component by 90%. In France, a reuse coalition bringing together 9 stakeholders plans experiments in more than 300 retail outlets.

Outlook for the spirits market

Consolidation and sector reshaping

Faced with these changes, the spirits industry is moving toward increased consolidation. In March 2026, Pernod Ricard confirmed discussions with Brown-Forman, a group with €3.4 billion in revenue, regarding a potential merger described as a “merger of equals.”

This consolidation strategy is accompanied by geographic reallocation. Rémy Cointreau, following the agreement signed in June 2025 on a minimum price for cognac in China, has raised its outlook. The potential tariff impact in China has been reduced from €40 million to €10 million.

Players are also focusing on gaining more direct control over strategic markets. Diageo decided to gradually take back direct distribution of part of its brands in France starting in 2023. In April 2025, the group targeted a 12% market share in value within the next five years, compared to 8.2% at the time of presenting its strategy.

In search of a recovery strategy

The outlook for the spirits market is no longer based on mechanical growth driven by volumes. It now relies on more refined trade-offs across four dimensions:

- more moderate alcohol offerings

- better value communication

- more experiential consumption occasions

- more precise commercial execution.

The market is not shrinking uniformly but becoming segmented. Categories that rely too heavily on traditional consumption or a single geographic outlet are struggling. Those that combine product innovation, clear premium positioning, cocktailization, sustainability, and channel adaptation continue to create value.

This segmentation explains why the overall decline in consumption does not prevent acquisitions, product launches, or major industrial investments. The spirits industry is less in a phase of decline and more in a phase of deep reconfiguration.

Frequently asked questions about the spirits market

What is the current size of the global spirits market?

The global spirits market represents several hundred billion euros. Global rum exports alone reached €2.4 billion in 2021. In France, the wine and spirits sector generates €32 billion in revenue, including €16 billion from exports. For an in-depth B2C market study in this sector, IntoTheMinds can support you in analyzing consumption trends.

Why is spirits consumption declining among young people?

Several factors explain this trend. Younger generations favor healthier lifestyles and moderate their alcohol consumption. Between 2020 and 2024, the share of 18–34-year-olds who do not buy alcohol for home consumption increased by 50% in France. This shift is accompanied by a preference for cocktails and low-alcohol products. An opinion survey can help better understand these behavioral changes.

Which spirits categories are the most dynamic?

Vodka and white spirits are the most resilient, with 4.2% value growth in 2025. Rum also performs well over the long term, with +16% in volume between 2019 and 2023. Flavored rums surged by +197% over this period. French whisky is also emerging, with +52.5% in volume in 2025. To analyze these sector dynamics, a B2B market study can identify opportunities by segment.

How do geopolitical tensions affect the spirits market?

French spirits exports fell by 17% in 2025 to €3.7 billion. The United States (-21%) and China (-20%) are particularly affected by trade tensions. Only the European Union shows resilience, with a limited decline of 1%. This geographic fragmentation is pushing companies to diversify their markets toward South Africa (+22%) or the Philippines (+20%).

What are the main innovation drivers in the spirits industry?

Innovation is focused on four main areas: moderation, with 12.5% of French revenue coming from alcohol-free or low-alcohol products in 2024; cocktailization, with 50% of 18–29-year-olds preferring cocktails over champagne; premiumization segmented into access, premium, and super-premium; and environmental innovation, with initiatives such as 100% recycled Jameson bottles. To measure the impact of these innovations, a customer satisfaction survey can assess consumer response.

What is the future of the French spirits market?

Despite a 2.6% decline in consumption in 2024, the French market remains strategic. It generates €17 billion in GDP and supports 151,000 jobs. The future lies in adapting to new expectations: lower-alcohol products, premium experiences, sustainability, and innovation. Companies that successfully combine these dimensions will continue to create value. A brand awareness study can help companies measure their positioning on these new criteria.