In recent weeks, economists and analysts of all persuasions have been arguing about the nature of the recovery: V, U, W, L, all the letters have been used. Yet none of them seems to reflect my understanding of this crisis. In this article, I present my recovery scenario and explain why it is useless to hope for a rapid return to normal.

Summary

- Recovery V is out of the picture

- It’s trust, stupid!

- Emotions dominate our decision making

- The previous crises were radically different

- My recovery scenario in 4 steps

- Finally

In a Nutshell

- The scenarios for V or U resumption have been abandoned.

- Recovery is dependent on consumer confidence → down 30 points since March 2020

- Uncertainty is maximum → Emotional decision making (primary instinct)

- The summer holidays will allow you to return to a familiar environment and to get back to your old habits from the start of the new school year (hypothesis: no 2nd wave).

- September 2020 will mark the beginning of a weak recovery.

- From January 2021, the recovery will be more marked, but it will take 5 years or more to return to the 2019 level (see 2008 crisis).

Recovery V is a distant memory

I still remember my banker telling me at the beginning of April about the V recovery. This carefree attitude seems far away and makes me smile.

In BNP Paribas Fortis’ Eco Perspective rating of April 5, 2020, the optimism is still there: “According to an initial assessment by the OECD, the impact on eurozone countries, although temporary in principle, will nevertheless be very marked.”

At the beginning of the crisis, the Conference Board was not looking beyond October 2020 for recovery. Their most optimistic scenario (May Reboot) even predicted a comeback as early as May 2020 (in “V,” of course).

We all know that recovery V is now totally impossible. This scenario is, for example, totally ruled out in the United Kingdom. While confident about the recovery, the Governor of the Bank of Canada has also ruled out a quick rebound.

Of course, some people have shown moderate optimism, and these have produced analyses that I am in favour of today. Stephen Harris‘ analysis of April 8, 2020, was measured and contrasted with the opinion that Jérôme Powell issued 5 weeks later. In his press briefing on May 17, 2020, Jérôme Powell stated:

Assuming there is no second wave of the coronavirus, I believe you will see the economy recover steadily in the second half of this year.

I think Jerome Powell is seriously mistaken, and I’ll do my best to explain why.

It’s about Trust, Stupid!

The nature of the crisis was certainly different in 2008. But that is not the problem. The engine of growth is consumption and in particular the consumption of the United States, whose currency, a haven since the Bretton Woods agreements, allows them to finance their delirious appetite for consumption by increasing their external deficit.

For there to be a recovery, whatever the nature of the crisis, the American consumer must, therefore, recover in a credit-consumption cycle.

In a period of uncertainty, such as the one we are going through, human judgment is based essentially on primitive emotional mechanisms.

We are no longer capable of making rational decisions.

An economic recovery, therefore, presupposes that consumers (especially Americans) will start to consume again. And to do so, they must regain confidence in the future, since consumption is done on credit. But confidence is very subjective. In a period of uncertainty, such as the one we are going through, human judgment is essentially based on primitive emotional mechanisms. Conscious analysis, whose seat is the cerebrum, is eradicated. We no longer think with our primitive brain (the cerebellum), which controls our survival instincts through our emotions.

For a recovery to be successful, therefore, the emotional climate must be conducive. To do this, you need to stabilise yourself, that is to say, to find a rhythm that is known and that allows you to find your bearings again.

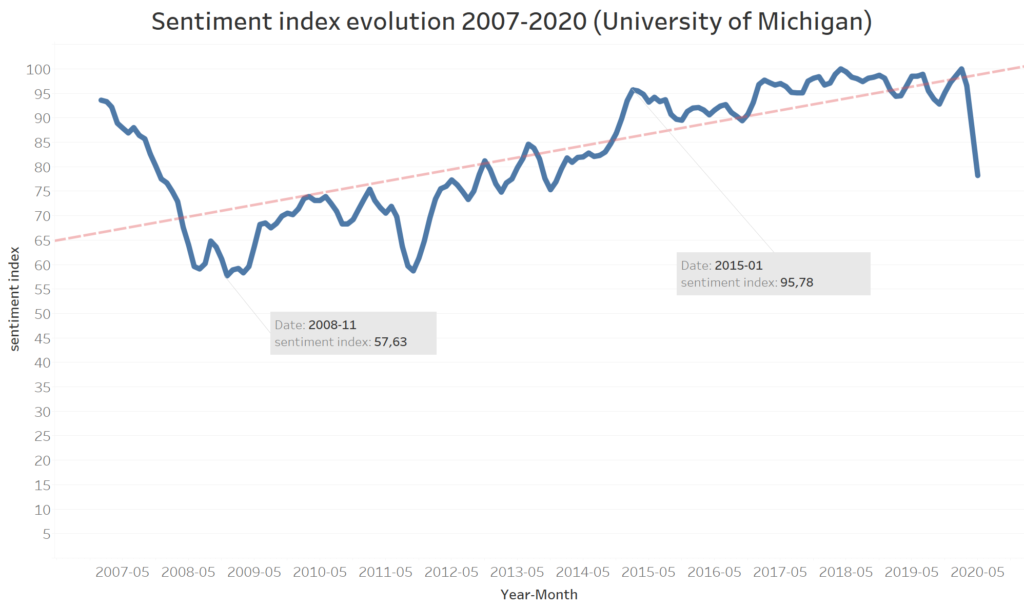

The collapse of confidence after the 2008 crisis was also brutal, and it took 74 months to return to pre-crisis levels (low point in December 2008 and first rebound in February 2015). This is why it is illusory to hope to reach post-crisis levels quickly. We are in a classic cycle of destruction – creation, but this time there is something different.

The different nature of previous crises

While the cycle of destruction-creation is not unusual, what we are experiencing today is new for our time. Since the Great Depression of 1929, the crises we have experienced have been entirely within the control of Man. He was at the origin of evil but was also able to find a solution. The best example is the subprime crisis in 2008, a reflection of human greed. Except that today, if once again human stupidity is at the root of the disaster, the solution escapes us completely. The breakdown of confidence in the future could be more significant than in any episode we have experienced so far. In an article published at the very beginning of the crisis, I wondered about the changes in behaviour that could be expected. Jerome Powell also wondered a few weeks apart. In his latest press conference, he said:

“Until [consumers] are confident that the virus is under control, they are likely to be reluctant to engage in certain types of activities.”

I have never been more convinced that significant behavioural changes will be visible in the coming years. It’s a groundswell that will lead to a retreat into the family cocoon. The digitalisation of interactions will become the rule, as will remote working and the reduction of office space. The consequences on innovation will be terrible because it is illusory to want to innovate from a distance.

These bleak prospects lead me to outline a 4-step recovery scenario.

We are entering an era of mass extinction: those of non-learning companies rigid and without digital skills.

My recovery scenario as an entrepreneur

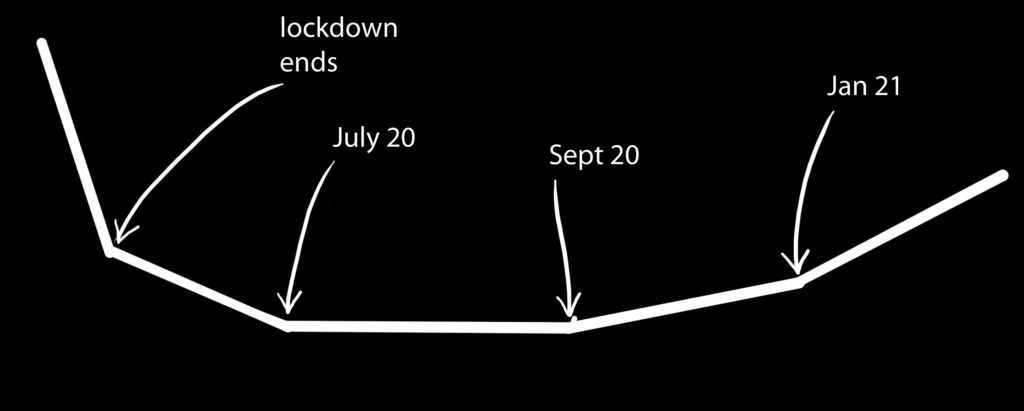

I’m not going to beat around the bush. 90% of the scenarios I’ve heard seem utterly crazy to me. There will be no V, U or W. I haven’t found a letter to describe it, but failing that, I’ve drawn it for you. And to make things even more complicated, I even added a timeline.

It looks a little like a wheelbarrow.

I distinguish 4 phases:

- The end of confinement: in Europe, the end of May should mark the end of confinement for most countries. The reopening (already effective) of some shops will allow the machine to be restarted, but this is still anecdotal.

- The summer period: some had counted on the fact that we would be deprived of summer holidays to hope for a quicker recovery. Today, it is reasonable to think that this will not be the case. The confinement has left psychological traces, a state of significant psychological fatigue, which we will compensate for this summer by taking some time off. And since June is close to the holiday period, don’t count on it to see a significant burst of activity.

- The beginning of September: The start of September will mark the first signs of a return to activity, but to a much lesser extent than before the crisis. The summer period will have enabled everyone to “get back on their feet” and to get back to their usual schedule.

- January 2021: from January 2021 new budgets will be available in companies. As long as a second wave has not swept through, we will return to the usual working mechanisms that are conducive to recovery. This is the “stabilising” pace I referred to in the previous paragraph. The recovery will be gradual, slower for specific sectors such as air transport, punctuated by social dramas (bankruptcies) that will take a long time to materialise (on average it takes 260 days in the United States for a business to be declared bankrupt). I don’t think we should expect to reach pre-crisis levels of activity in 2021.

Finally

I am aware that my predictions are not the most optimistic. Perhaps I wrote them down to forestall them. But deep down, I can’t help thinking that the world of tomorrow will not be the same from a business point of view. I plead for the versatility of individuals, for continuous learning, and I am increasingly convinced that we are entering a mass extinction: those of non-learning, rigid companies without digital skills.

Images : shutterstock