In this article, our firm analyses how Chinese car exports have disrupted the European economy. Based on the latest available figures, our analysis provides a comprehensive overview of a complex subject.

In less than a decade, China has moved from the status of a captive market to that of the world’s leading automobile exporter. Its car manufacturers, driven by massive subsidies and a vertical integration without equivalent, are now flooding European markets with electric and hybrid vehicles at prices that defy all competition. Our market research agency, drawing on its expertise in the automotive sector, offers you an in-depth analysis of this market using the latest available statistics.

Contact the IntoTheMinds institute

Key takeaways

- Chinese global automobile exports increased from 1.2 million units in 2019 to 6.4 million in 2024, then 8.3 million in 2025, an almost sevenfold increase in six years.

- Chinese car exports to Europe create an existential risk for European brands, which are simultaneously hit by slowing exports to China and the United States. The Porsche case and more broadly German manufacturers are highly illustrative.

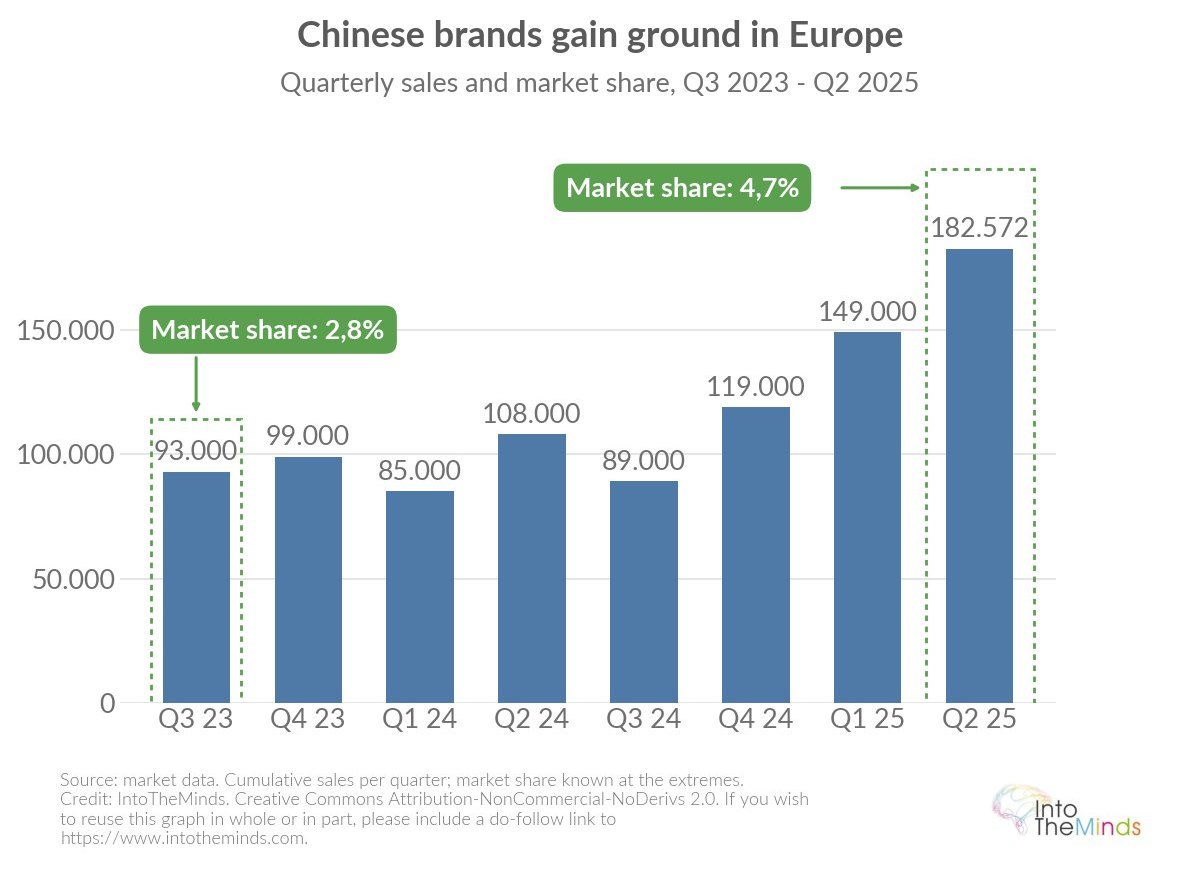

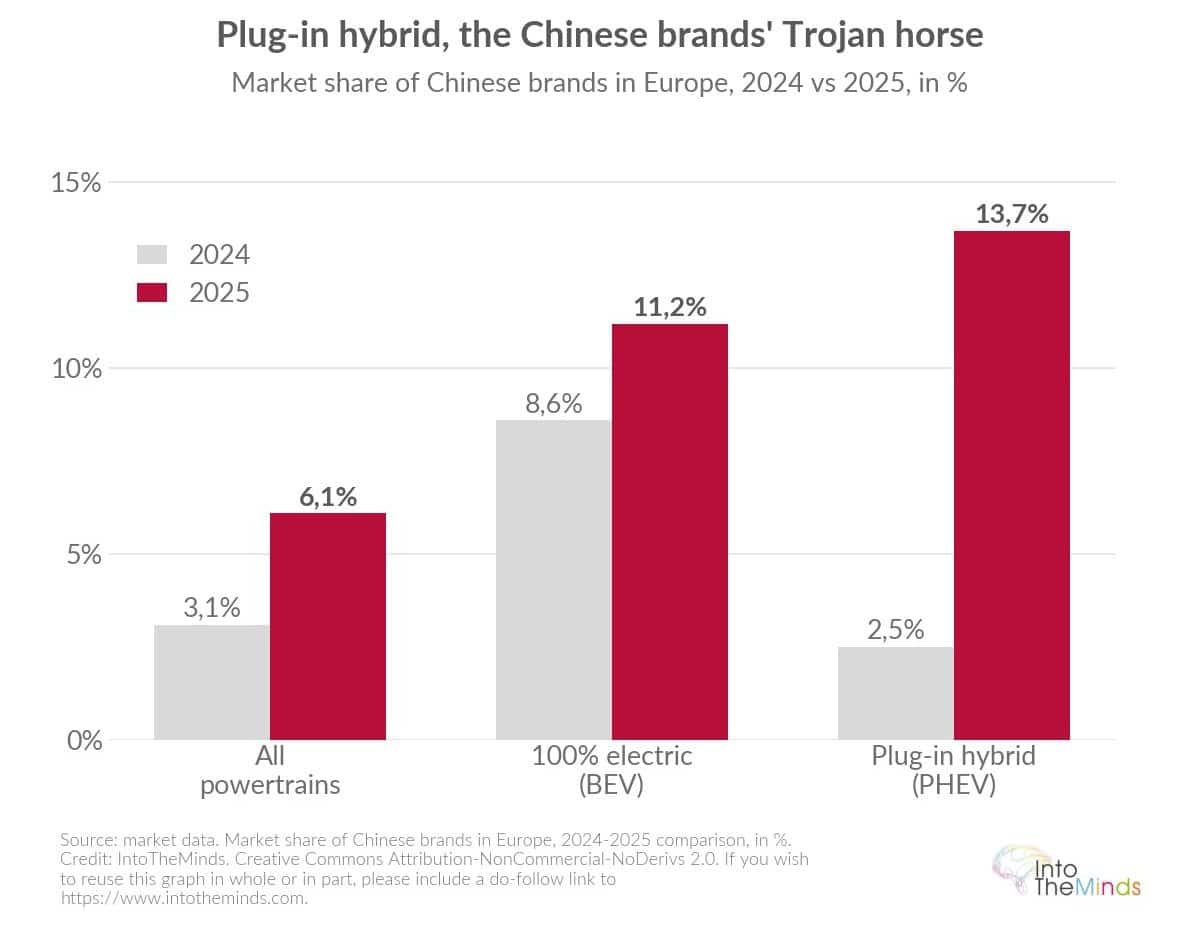

- In Europe, Chinese brands reached a market share of 6.1% in 2025, up from 3.1% in 2024, with 812,190 registrations.

- In plug-in hybrids, the share of Chinese brands in Europe jumped from 2.5% to 13.7% in one year. The BYD Seal U was the best-selling PHEV in Europe in 2025.

- European suppliers announced 104,000 job cuts over 2024–2025, and 19% of small suppliers were in a “critical zone” at the end of 2025.

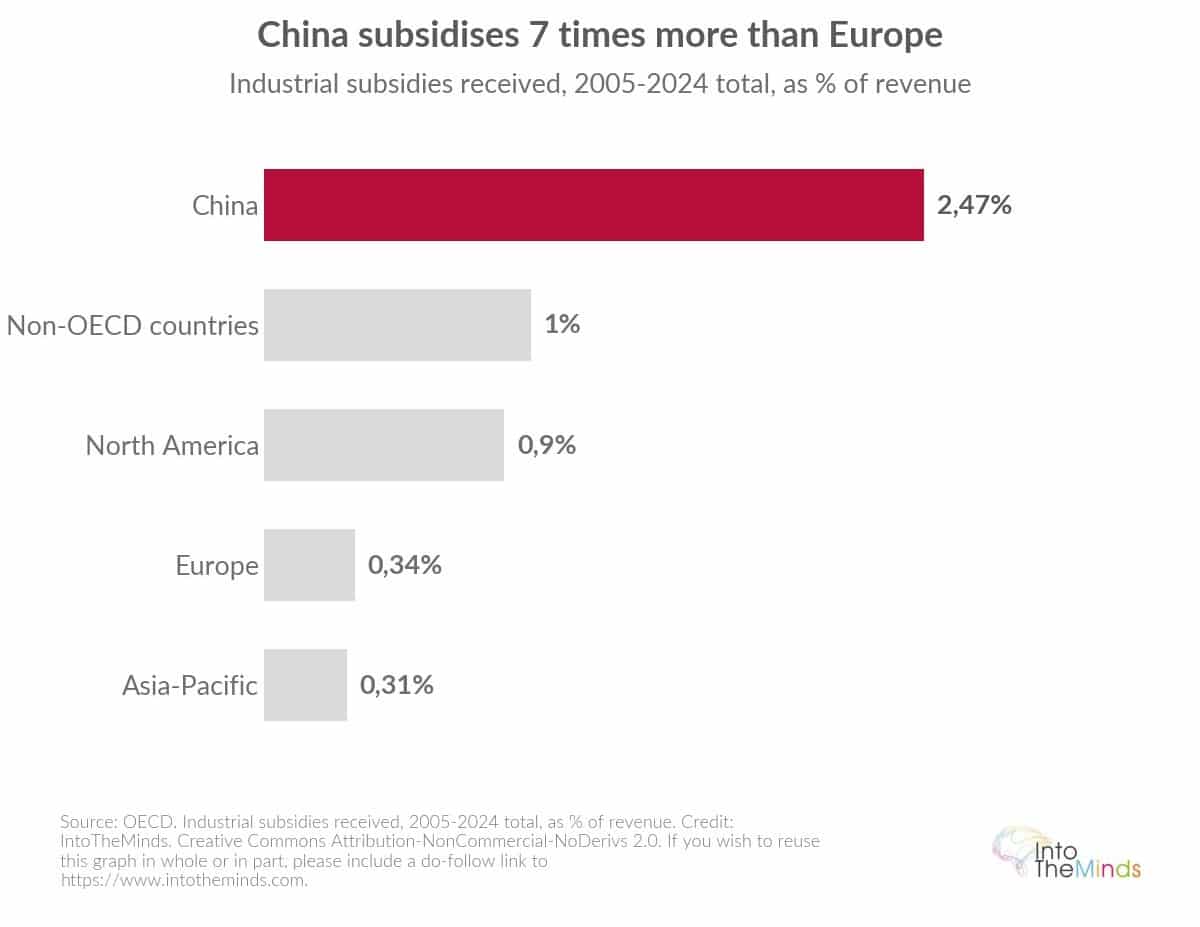

- Chinese companies received between 2005 and 2024 three to eight times more public subsidies than their OECD competitors, largely explaining their price competitiveness.

The boom in Chinese automobile exports

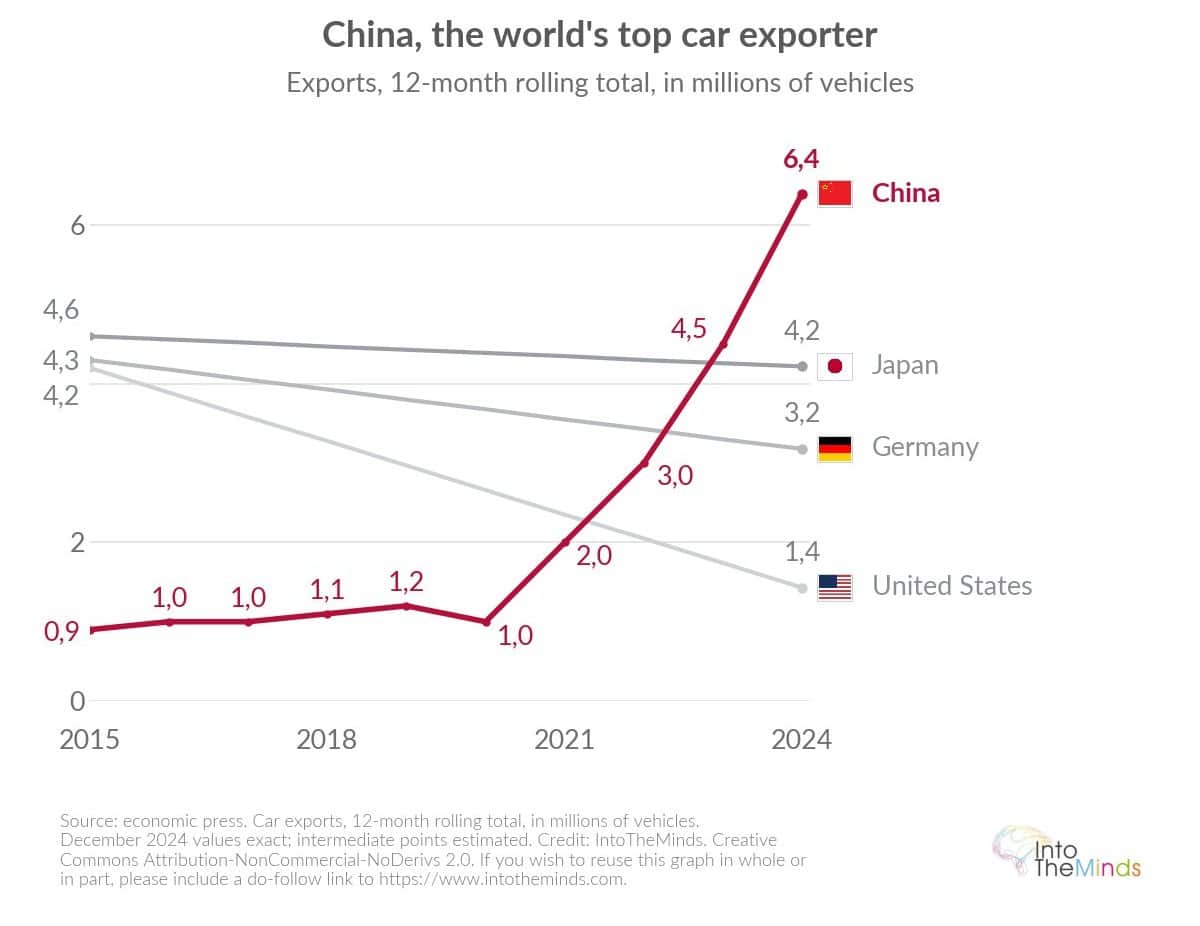

It is no exaggeration to say that the trajectory of Chinese automotive exports is unprecedented in the history of the automotive industry. In 2015, China exported around 0.9 million vehicles per year, far behind Japan, Germany and the United States. Ten years later, the balance of power has completely reversed.

Over the full year 2025, China exported 8.3 million vehicles compared with 1.2 million in 2019.

Figures and trends

In 2024, Chinese exports reached 6.4 million units, ahead of Japan (4.22 million), Germany (3.18 million) and the United States (1.43 million). Over the full year 2025, the total reached 8.3 million exported vehicles, compared with 1.2 million in 2019. The acceleration continued into early 2026: in March 2026, China exported 183,000 fully electric cars (+100.1% year-on-year) and 154,000 plug-in hybrids (+199.7%)! You can now grasp the scale of the tsunami unfolding.

This surge is based on a massive industrial base. In 2024, China produced 31.28 million vehicles and sold 31.43 million domestically, including 41% new energy vehicles. The domestic market, which represented 21.5 million sales in 2019, reached around 30 million in 2025. But this growth hides a more tense reality: around one hundred manufacturers are engaged in a price war that is eroding margins. Of 129 Chinese EV brands identified in 2025, only about fifteen are expected to be profitable by 2030. We speak of a massacre in Europe, but the scale is even greater in China.

Of 129 Chinese EV brands identified in 2025, only around fifteen are expected to be profitable by 2030.

Chinese manufacturers dominating exports

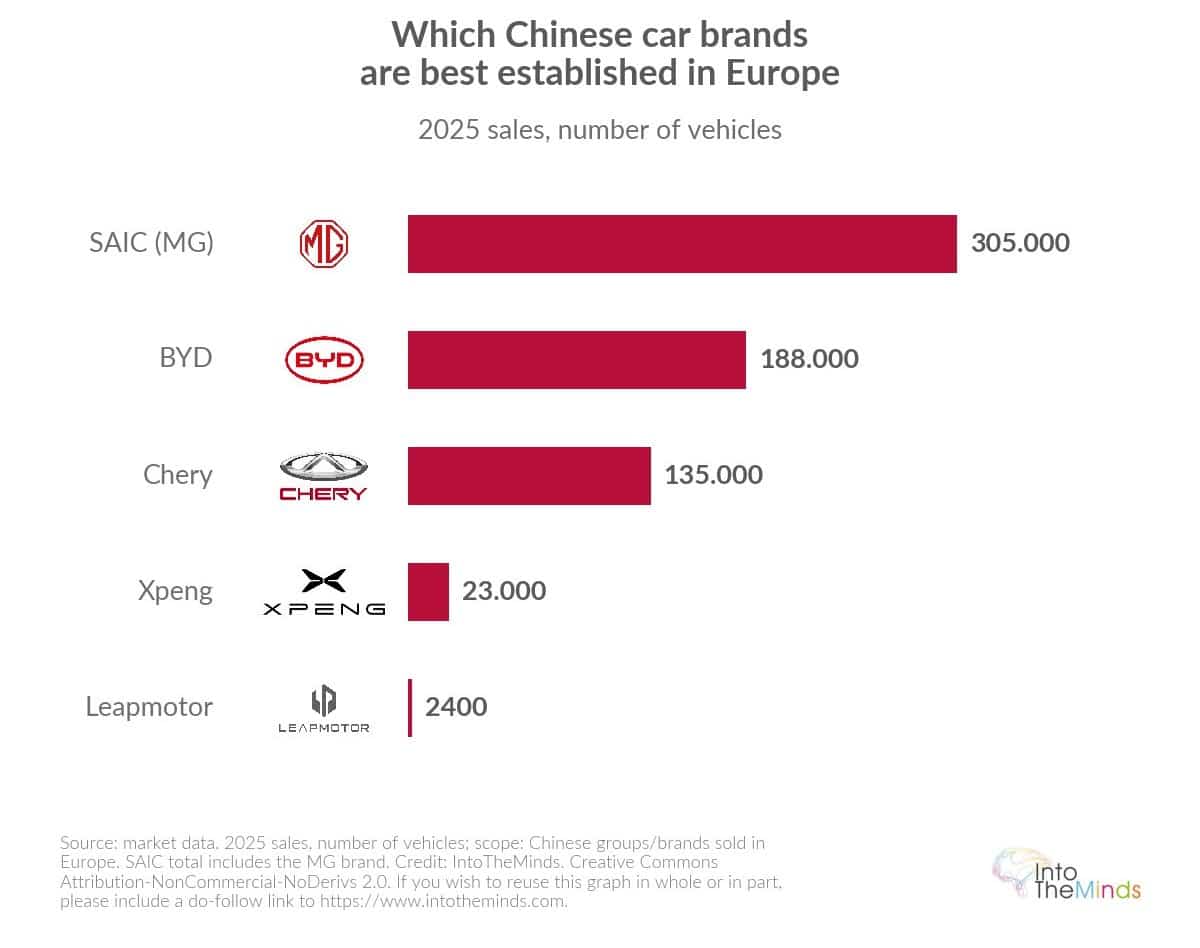

We analysed the latest data from ACEA and other sources to compile a ranking of the Chinese brands most present in Europe in 2025:

- SAIC / MG: around 305,000 sales in Europe in 2025 (+25% year-on-year), including 211,000 under the MG brand alone, the leading Chinese brand in Europe.

- BYD: 188,000 units in Europe in 2025, a threefold increase in one year. Its European registrations rose from 40 units in 2020 to 51,327 in 2024, then to 188,000 in 2025.

- Chery (Omoda, Jaecoo): 135,000 vehicles sold in Europe in 2025, with a target of 150,000 in 2026. As a side note, IntoTheMinds conducts the brand awareness surveys for Jaecoo 😋

- Xpeng: 23,000 sales in Europe in 2025, present in 26 countries, with around 430,000 global sales (+126% year-on-year).

- Leapmotor: still modest in Europe (around 2,400 registrations in July 2025), but 600,000 global sales in 2025, twice as many as in 2024.

- Geely: launched under its own brand in France in April 2026, with 4.12 million global sales in 2025 and a target of 6.5 million by 2030.

Target geographies and growth zones

The penetration of Chinese cars in Europe is highly uneven depending on the country:

- The United Kingdom is at the top of the ranking, so to speak. The share of Chinese brands there rose from 4.9% in 2024 to 9.7% in 2025, and is expected to reach 20% by 2030.

- In Spain, the market share of Chinese cars already exceeded 10% in 2025;

- In Italy, it exceeds 8%: BYD has become the number one electric brand there with around 25,000 units.

- In Germany, buyers are resisting, one could say. Only 5,000 Chinese vehicles were sold in the second quarter of 2025.

- France is also resisting: BYD sold only 14,000 vehicles there in 2025 (0.8% of the market).

| Country | Share of Chinese brands 2024 | Share of Chinese brands 2025 | BYD sales 2025 |

|---|---|---|---|

| United Kingdom | 4.9% | 9.7% | 51,000 units (6% of the market) |

| Spain | n.d. | >10% | ≈25,000 units |

| Italy | n.d. | >8% | ≈25,000 units (electric #1) |

| France | n.d. | 0.8% (BYD only) | 14,000 units |

| Germany | n.d. | low | ≈5,000 (Q2 2025) |

| Europe total | 3.1% | 6.1% | 188,000 units |

According to the OECD, 22% of the global market share gains of the Chinese automotive industry over the past two decades are attributable to subsidies.

Why are Chinese cars so competitive?

Price is central to understanding the dynamics of Chinese car exports. The price gap does not come from a single factor, but from a combination of structural advantages.

State subsidies with no Western equivalent

According to several economic analyses, Chinese companies have received significantly more public support over the past two decades than their OECD counterparts: 2.47% of revenue in China, compared to 0.34% in Europe, 0.9% in North America, and 0.31% in Asia-Pacific. The OECD estimates that 22% of global market share gains over these two decades are attributable to subsidies, rising to 60% for Chinese companies. One quarter of Chinese firms operating in Europe are running at a loss, confirming a strategy focused on market share conquest over short-term profitability.

In addition to subsidies, there are:

- vertical integration (BYD manufactures internally nearly 70% of its value chain)

- an advance in production processes

- a currency (the yuan) structurally estimated to be undervalued against the euro, which mechanically supports exports.

In May 2025, BYD cut prices by up to 34% on 22 models, bringing its entry model down to €6,791! At a time when the cheapest European car sells for around €20,000, the gap is obvious.

Top-tier equipment and ultra-competitive pricing

Beyond price, Chinese cars rely on a technology-to-price ratio that is difficult to match. Large screens, advanced connectivity, driver assistance systems, and ultra-fast charging form the core of the offering. BYD recently announced ultra-fast charging technologies allowing significant range recovery in just a few minutes, and Xpeng claims 80% charge in twelve minutes.

Chinese manufacturers are no longer just copying—they are at the forefront of innovation in many areas.

These performances match the expectations of increasingly cost-sensitive European consumers. Long warranties (6 to 8 years) further strengthen the attractiveness of the offer. Interestingly, this long-warranty strategy—first designed by Japanese manufacturers, then adopted by Korean ones, and later by Chinese firms—has not yet been widely replicated by European automakers.

However, patriotic buying behavior still slows adoption: 48% of French consumers say they are willing to pay more for local industry in 2026, compared to a global average of 39%. But this effect disappears once the price gap exceeds 10% (see pricing sensitivity methods such as Van Westendorp).

In Germany, 29% of drivers would consider a Chinese car in January 2026, up from 25% a year earlier.

Chinese PHEV registrations in Europe jumped by 645% in 2025, while the European PHEV market grew only by 33%

Plug-in hybrids: the Trojan horse

The most significant strategic shift of 2025 is the massive pivot toward plug-in hybrids (PHEVs), taxed at only 10% compared to up to 45.3% for Chinese-made fully electric vehicles. Chinese PHEV registrations in Europe rose by 645% in 2025, while the European PHEV market grew by only 33%. As early as April 2025, volumes had increased by 546% year-on-year (from 1,493 to 9,649 units).

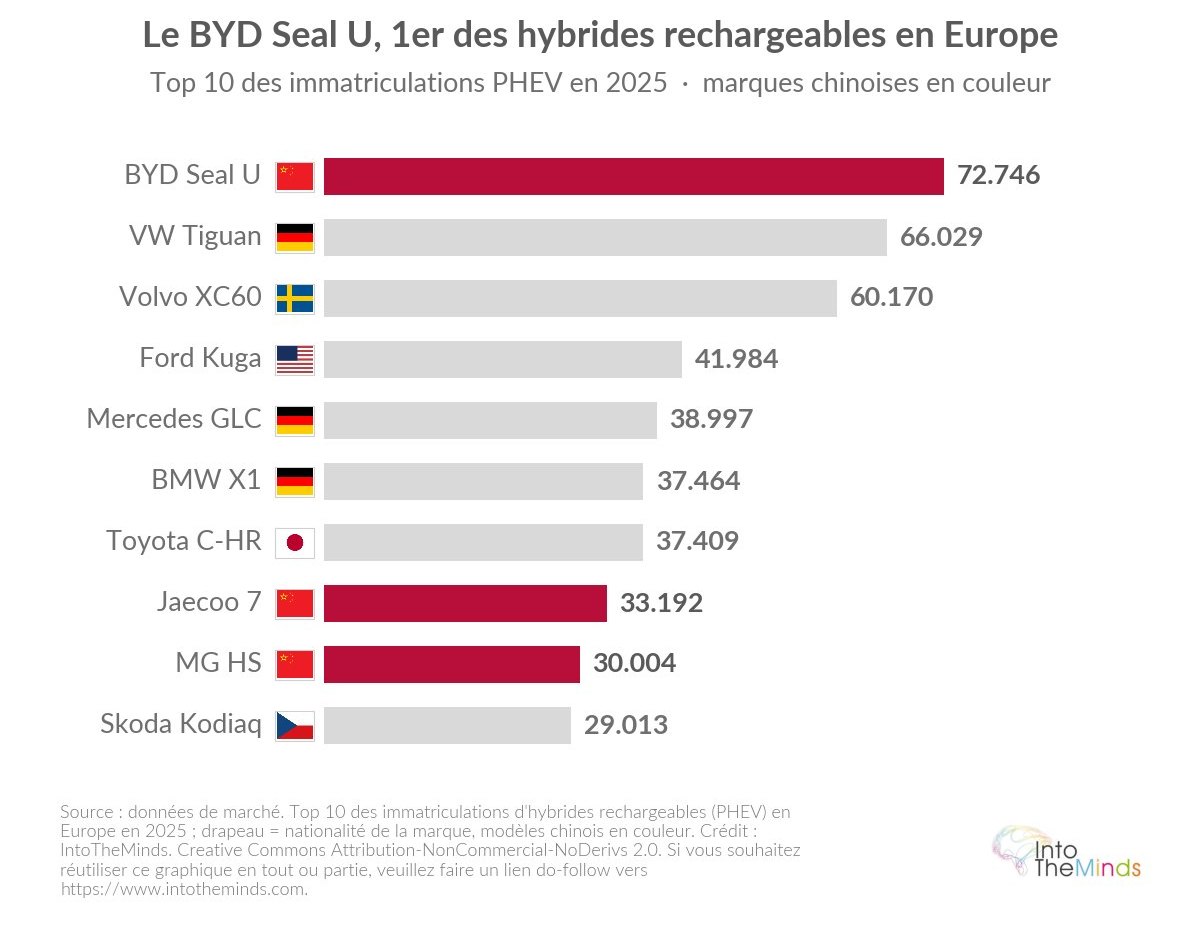

The result is striking: in 2025, the BYD Seal U became the best-selling PHEV in Europe with 72,746 registrations, ahead of the Volkswagen Tiguan (66,029) and Volvo XC60 (60,170). Two other Chinese models also appear in the ranking: Jaecoo 7 (33,192) and MG HS (30,004).

The market share of Chinese brands in this segment rose from about 3% to 14% in one year. The average import value of Chinese new cars also dropped by 27% in 2025, fully offsetting the tariffs introduced in October 2024.

Impact on the European automotive industry and suppliers

Pressure from Chinese car exports is translating into concrete effects on jobs and margins across the European automotive value chain.

Suppliers under pressure

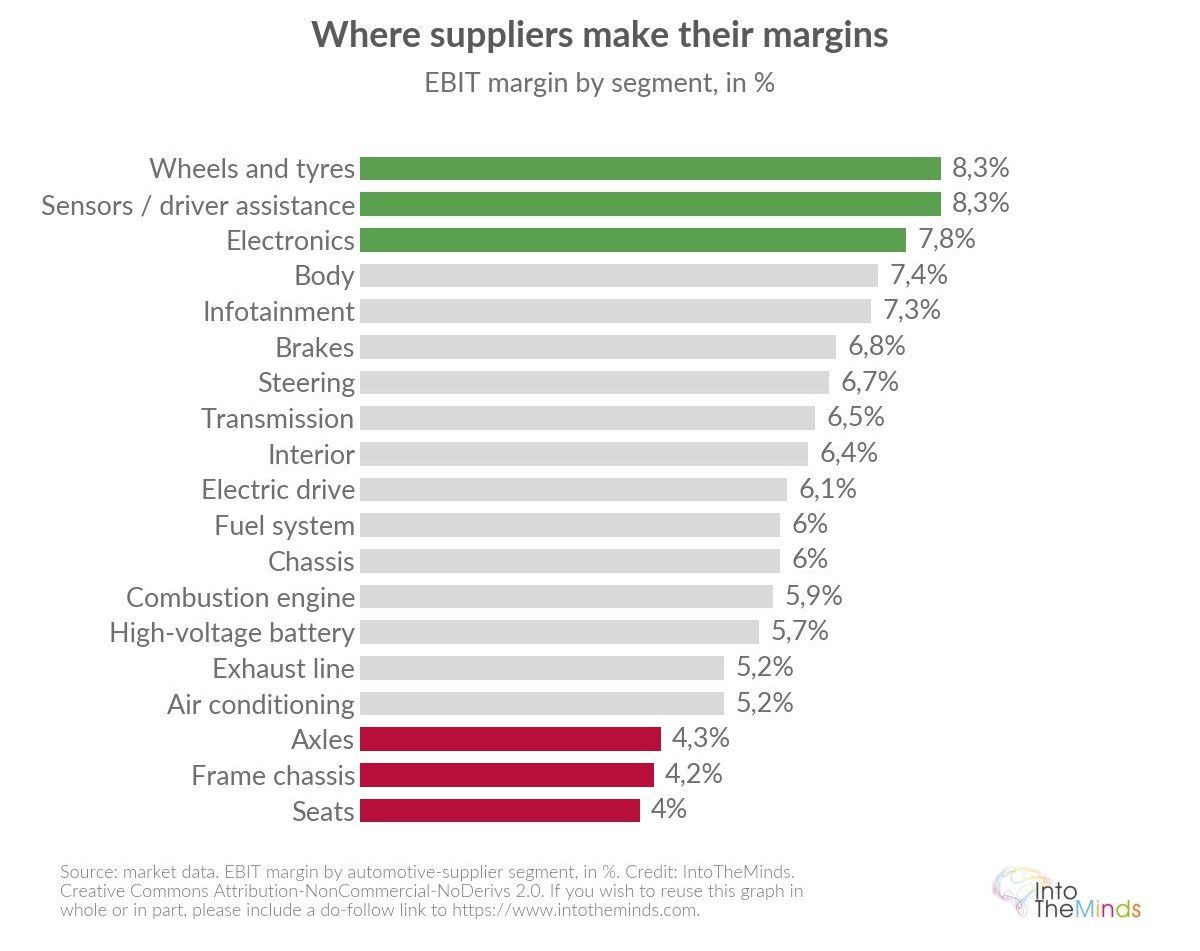

According to a December 2025 sector study, 12% of large suppliers and 19% of small ones were in a “critical zone.” The most exposed segments are:

- seats: 4.0%

- chassis: 4.2%

- axles: 4.3%

More profitable segments such as sensors and driver-assistance systems (8.3%) or electronics (7.8%) are faring better.

Nearly 70% of European suppliers face direct competition on components, with Chinese prices 20–30% lower. Transmission part imports have tripled. In total, 104,000 job cuts were announced across European suppliers in 2024–2025.

German automakers at the front line

Germany is experiencing the most visible impact. Around 51,500 automotive jobs disappeared in one year (nearly 7%):

- 35,000 at Volkswagen

- 13,000 at Bosch

- 7,600 at ZF

- 5,000 at Daimler Truck

German automakers’ share in China fell from 25% in 2019 to around 15% in 2025–2026, while their electric vehicle registrations in China dropped by 46% over the first nine months of 2025.

On the €200,000–€300,000 yuan segment, Xiaomi alone sold 225,023 EVs in China between January and August 2025—almost double the combined 114,682 sold by all German automakers.

In France, the automotive sector (around 560,000 related jobs) fell from 375,000 employees in 2019 to 336,000, with a projection of 261,000 by 2035—around 115,000 jobs lost over 15 years.

What Europe has tried and what it can still do

The European response has been late and only partially effective.

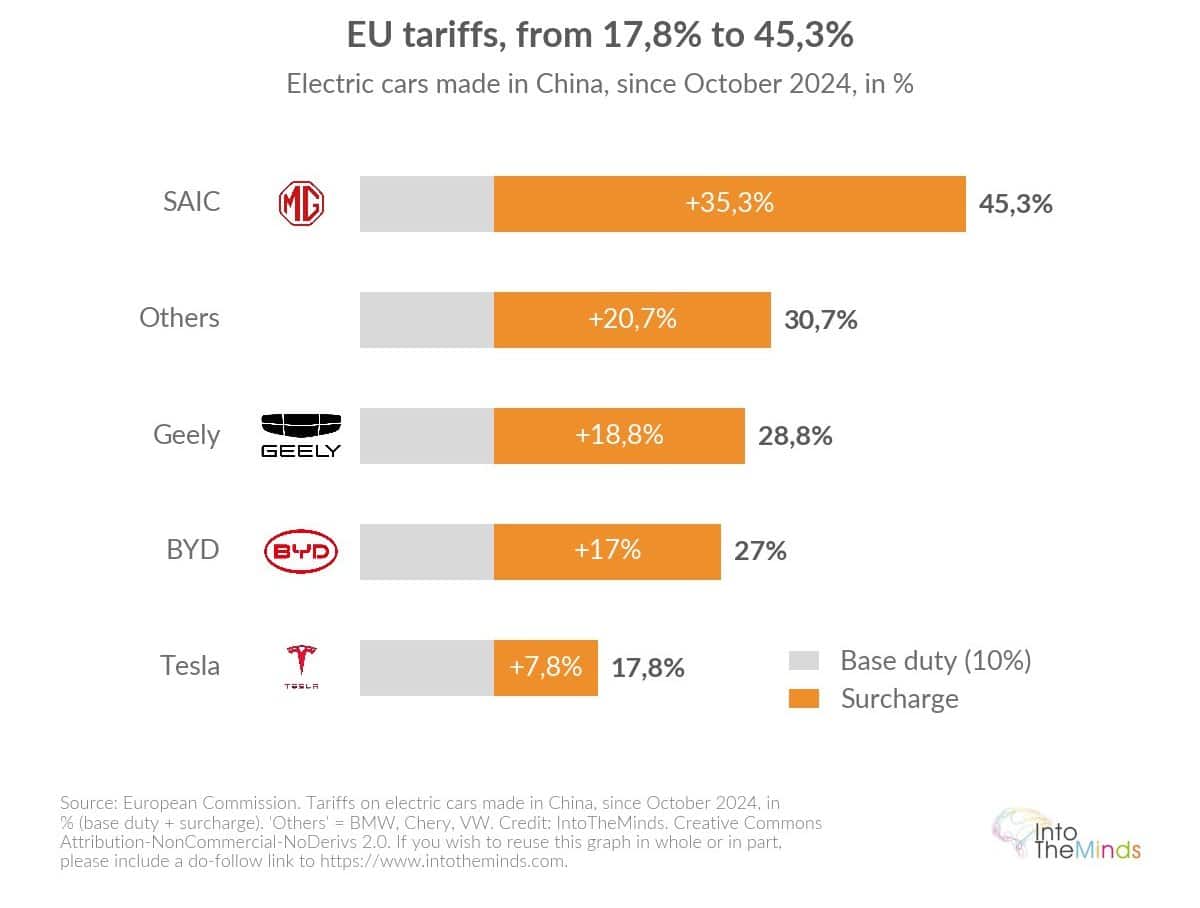

In October 2024, the European Union introduced additional tariffs on Chinese electric vehicles:

- 35.3% surcharge for SAIC (45.3% total)

- 18.8% for Geely (28.8%)

- 17% for BYD (27%)

- 20.7% for others (30.7%)

- 7.8% for Tesla (17.8%)

These tariffs were largely circumvented by the shift toward hybrids and local production. In January 2026, the Commission proposed replacing them with a minimum import price system, but this option was considered fragile.

Other levers have been activated or are under discussion :

- Easing of the CO₂ trajectory, with smoothing of penalties over 2025–2027 and authorization of hybrids beyond 2035.

- Allocation of €1.5 billion in loans to European battery manufacturers.

- Debate on a local content threshold (70% to 75% of value excluding batteries), batteries representing 40 to 50% of the value of an electric vehicle.

- Proposal for a “Made in Europe” CO₂ bonus conditioning purchase subsidies and access to public procurement (supported by Stellantis and Volkswagen).

- Additional French bonus of €1,000 for vehicles with European batteries.

- Tariffs of up to 102.5% discussed in May 2026, following the US model (100% on Chinese electric vehicles).

The imbalance in industrial preference tools remains striking: according to a March 2026 study, the European Union applied only six industrial preference measures, compared with 983 in the United States, 315 in India, 131 in Brazil, and 112 in Russia. US pressure (100% tariffs) is also accelerating the redirection of flows toward Europe: Chinese exports to the EU jumped by 27.8% in the first two months of 2026, while Chinese imports into the United States fell by 20% year-on-year.

The strategy for conquering the European market

Chinese car manufacturers are deploying a methodical sequence to establish a lasting presence in Europe, far beyond simple exports.

The first step is the rollout of distribution networks. BYD went from 23 dealerships in France in 2023 to 90 by the end of 2025, with a target of 200 by the end of 2026 and more than 1,000 across Europe.

The second step is high-visibility event marketing:

- sponsorship of Euro 2024 football tournament;

- launch of the luxury brand Denza at the Opéra Garnier in April 2026 (with actor Daniel Craig as ambassador);

- launch of Geely at the Carrousel du Louvre;

- launch of Chery with Jean Reno.

The third step is local industrial implantation, facilitated by the difficulties of European manufacturers, who see this as an opportunity to save their factories:

- BYD: plant in Hungary (end of 2025, 150,000 vehicles per year, capacity potentially doubling) and plant in Turkey (early 2027).

- SAIC: plant in Spain in A Coruña (target of 120,000 units by end of 2028, 2,300 jobs, initial investment of €200 million).

- Chery: production site near Barcelona (target 200,000 units per year).

- Xpeng: assembly in Graz, Austria.

- Leapmotor: production in Stellantis’ Spanish factories.

- Dongfeng: entry into the Stellantis plant in Rennes (May 2026).

Chinese production capacity in Europe is estimated at 1.1 million cars per year by 2028. R&D centers have been opened in Munich, Paris, and Gothenburg. This local production will allow companies to bypass tariffs while benefiting from the European label for purchase incentives, significantly complicating Brussels’ regulatory response. European factory overcapacity, estimated at 50% in April 2026, makes this strategy even more attractive for players seeking to produce locally without building entirely new capacity.

In the short term, this calculation may indeed provide a breathing space. But in the medium and long term, the establishment of Chinese manufacturers at the heart of Europe will erode Europe’s century-old expertise and give Chinese players immense negotiating power over Europe. One could say that European factories have become another Trojan horse of the Chinese automotive industry.

FAQ: Questions you may have

What are the main Chinese automotive exporters to Europe?

In 2025, the European ranking is dominated by SAIC (via MG, around 305,000 sales), followed by BYD (188,000 units), Chery (135,000 units under the Omoda and Jaecoo brands), Xpeng (23,000 units across 26 countries), and Leapmotor. Geely launched its direct presence in France in April 2026. These brands target both electric and plug-in hybrid segments, with ranges specifically designed for the European market.

Why are Chinese electric cars cheaper than European ones?

The price gap is due to several cumulative factors: public subsidies three to eight times higher than those granted in the OECD area (2005–2024), strong vertical integration (BYD produces nearly 70% of its value chain in-house), an estimated undervaluation of the yuan of at least 40% against the euro in January 2026, and a deliberate margin-sacrifice strategy to gain market share. In May 2025, BYD reduced prices by up to 34% across 22 models.

Which European countries import the most Chinese cars?

The United Kingdom is the most penetrated market, with a 9.7% share for Chinese brands in 2025 and a projection of 20% in 2030. Spain (>10%) and Italy (>8%) follow. France and Germany resist more strongly, notably due to ecological bonus schemes excluding vehicles produced outside Europe. Niche markets such as Denmark also represent favorable outlets for brands like Xpeng.

Have European tariffs slowed Chinese car exports?

The tariffs introduced in October 2024 (up to 45.3% for SAIC) have been largely bypassed through two mechanisms: the shift toward plug-in hybrids (taxed at only 10%) and the establishment of factories in Europe. Chinese PHEV registrations in Europe surged by 645% in 2025, and the average unit value of Chinese imports fell by 27%, fully offsetting the tariffs. Chinese exports to the EU increased by 27.8% in the first two months of 2026.

How can a company analyze the impact of Chinese cars on its sector?

Faced with this market reshaping, industry players (suppliers, distributors, corporate fleets) need a precise understanding of their competitive exposure. IntoTheMinds conducts B2B market research and B2C market studies to assess competitive dynamics, consumer purchase intentions, and substitution risks. Brand awareness surveys can also measure perceptions of Chinese brands among European buyers.

What is the impact of Chinese car exports on jobs in Europe?

The impact is already massive and well documented. European suppliers announced 104,000 job cuts between 2024 and 2025. In Germany, around 51,500 automotive jobs disappeared in one year (nearly 7%), including 35,000 at Volkswagen. In France, employment in the sector fell from 375,000 in 2019 to 336,000, with a projection of 261,000 in 2035—around 115,000 jobs lost over fifteen years. These figures reflect both direct Chinese competition and the transition to electric vehicles.

![Illustration of our post "Digitization: food & beverage industry companies lag far behind [Research]"](/blog/app/uploads/marche-alimentation-bio-long-120x90.jpg)

![Illustration of our post "75% of backlinks come from translations [Research]"](/blog/app/uploads/langues-langages-talen-120x90.jpg)