For many of us, coffee is a daily ritual and a constant companion throughout the day. It is also a market that has weathered successive crises and is seeing consumption habits diversify. In this analysis, we provide a comprehensive overview based on the latest available figures.

Will coffee become a luxury product? Probably not to that extent, but it is clear that coffee prices have risen sharply in recent years and that some players (including Nespresso) are clearly moving upmarket to increase their margins. Drawing on our experience in market research, we have analyzed the latest available data to provide you with a concise overview of the current and future situation, as well as the sector’s key trends.

Key takeaways on the evolution of the coffee market

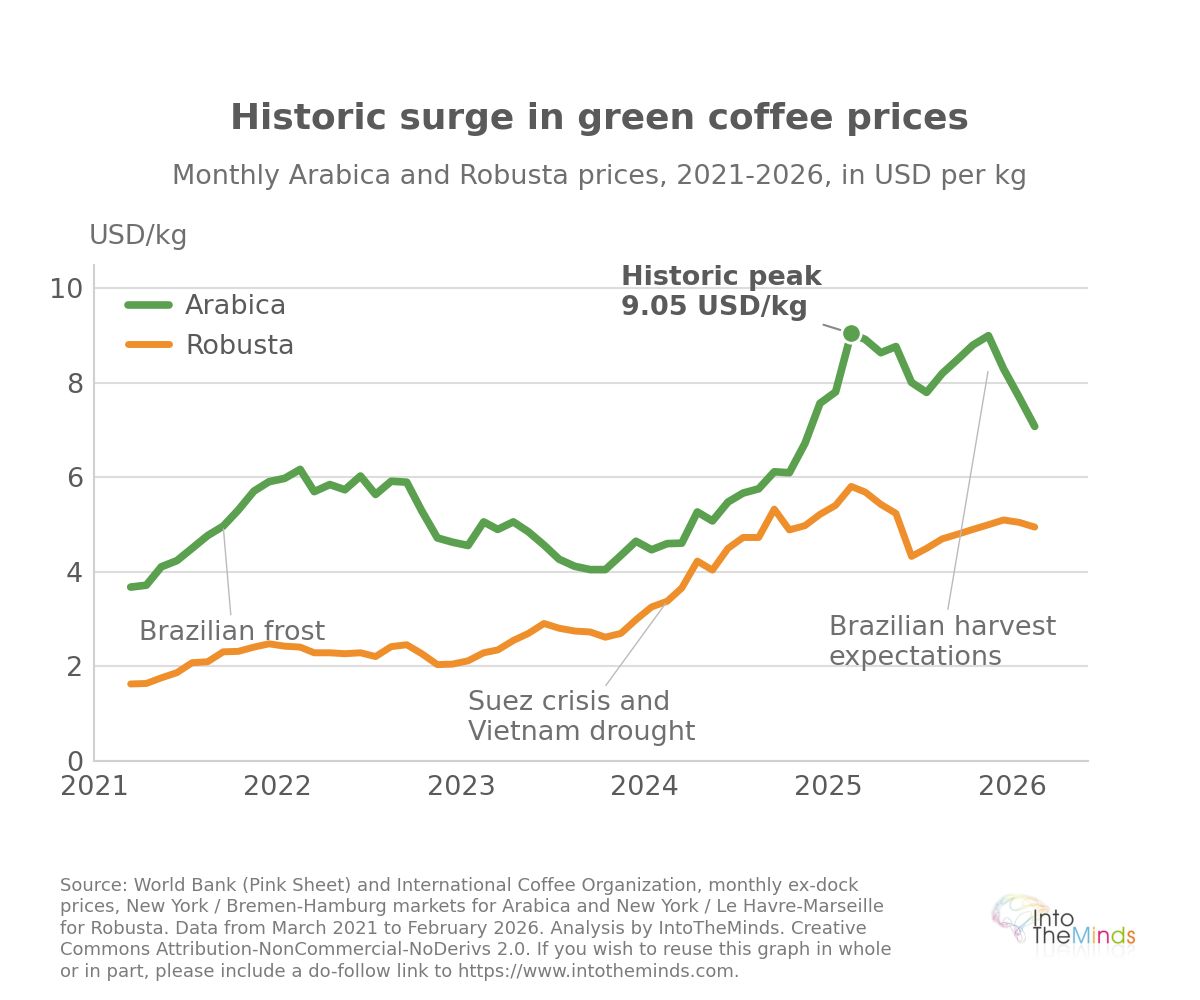

- Price surge: Arabica rose by 190% between January 2023 and December 2024, Robusta by 260%

- Declining volumes: the global market fell by 3.5% in volume over 2023–2024, then by 2.4% in 2025

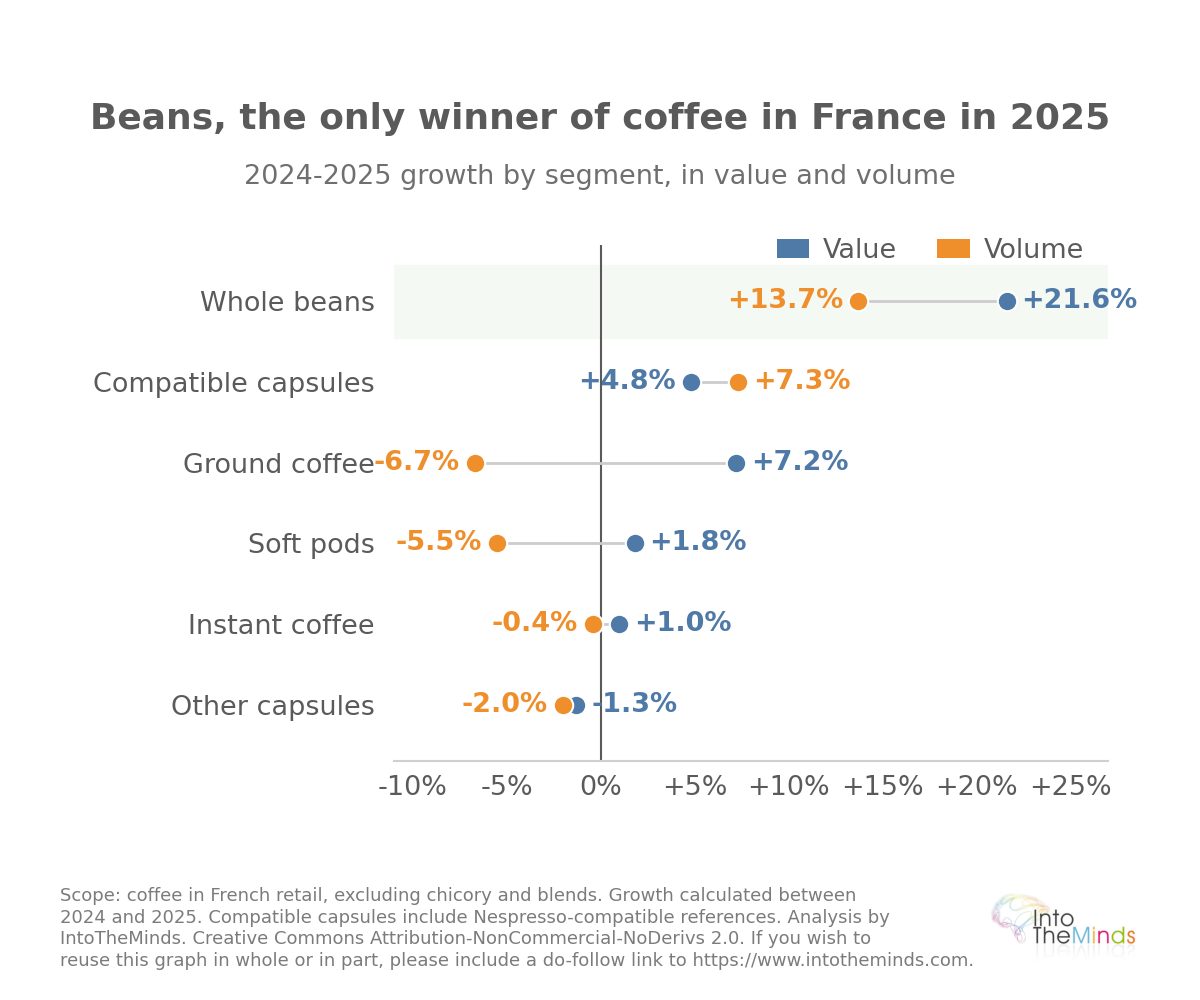

- France in transition: €3.80 billion in revenue in 2025 (+5.7%) but -1.1% in volume

- Whole bean coffee booming: +21.6% in value and +13.7% in volume in France in 2025

- New habits: 32% of out-of-home coffee was consumed cold in 2023 globally

Global coffee market analysis

A market under pressure from production costs

It is no exaggeration to say that the coffee industry is going through a turbulent period. Global prices have literally surged in recent years, and this spike is not driven by excessive demand but by a structural supply shock. The figures speak for themselves: since 2021, Arabica prices have risen by 230% and Robusta by 325%. This trend even accelerated in 2025, with additional increases of 20% for Arabica and 10% for Robusta.

This situation results from a combination of factors that are structurally weakening the market balance:

- Climate disruptions affecting key production areas, notably Brazil and Vietnam

- Geographic concentration of Robusta production, making the market vulnerable to supply disruptions

- Financial speculation (coffee has unfortunately become a financial asset like any other)

- Rising logistics costs (likely to continue due to the conflict in the Middle East)

- Geopolitical tensions

Take the example of the Suez Canal. Its closure has lengthened some routes by 20 days and quadrupled transport costs. At the same time, the European Union, which represents 30% of the global coffee market, is tightening its regulations. Some industry professionals estimate that these new requirements could put up to 80% of global production destined for the European market at risk. As a reminder, the European regulation (EUDR), applicable from 2026, bans the sale in the EU of coffee sourced from deforested land.

| Variety | Increase 2023–2024 | Increase since 2021 | Increase 2025 (early year) |

|---|---|---|---|

| Arabica | +190% | +230% | +20% |

| Robusta | +260% | +325% | +10% |

Resilience in the face of the raw materials crisis

Despite significant pressure from rising raw material costs, major industry players have shown remarkable adaptability. Take Lavazza as an example. The Italian group spent €1.6 billion on green coffee purchases in 2024, compared to €600 million in 2019—a 2.7-fold increase. Yet its financial performance remains solid, with revenue of €3.9 billion in 2025 (+15.7%), EBITDA of €340 million, and net profit of €92 million.

This performance can be explained by several strategies:

- partial pass-through of cost increases into selling prices

- optimization of inventory management

- adaptation of the product portfolio (which will be discussed further in this article)

Major roasters have also invested in innovation and differentiation to maintain attractiveness despite inflation. I also invite you to read this article I wrote following my visit to the Lavazza Museum in Turin, which illustrates this drive for differentiation.

The outlook could improve with Brazilian production prospects. In 2026, Brazil could produce 30 million bags of Robusta compared to 28 million for Vietnam. This potential rebalancing of supply fuels hopes for price stabilization, although this outlook remains dependent on climate conditions and geopolitical tensions.

Analysis of the French coffee market

France provides a perfect example of this new market dynamic. According to the data we gathered, there is solid growth in value but a more concerning reality in terms of volume. In 2025, the French market reached €3.80 billion in revenue (+5.7%) but declined by 1.1% in volume. This reflects a market that remains essential in consumption habits but is increasingly subject to trade-offs. In other words, coffee spending is no longer as automatic as it once was.

French consumers are adapting their purchasing behavior in response to inflation. They compare more, switch formats, and become more sensitive to value for money. This leads to a shift toward solutions perceived as either more affordable or more premium. Value growth therefore reflects both price increases and the market’s ability to maintain relatively high consumption despite budget constraints.

The French coffee market is therefore mature. With annual consumption of 7.2 kg per capita in 2024 and presence in 93.3% of French households, volume growth potential remains limited. The focus is therefore shifting toward added value and differentiation.

Coffee at the heart of French habits

Despite all these transformations, coffee remains central to everyday life in France. In 2022, the hot beverages market reached €3.9 billion (+4.7%) even though the number of cups declined by 2.4%. Coffee accounted for 100% of the growth in this segment, making it the main driver of the category.

Its dominance at breakfast remains overwhelming. In 2023, coffee generated €3.658 billion in the breakfast segment in France, representing 54.1% of the total value. This position remains very strong, even as habits evolve across generations. Some key figures:

- 38% of under-34s associate coffee with an energy boost

- 56% of over-55s prioritize taste pleasure

- 30% of 16–25-year-olds say they do not drink hot coffee

- 60% of 16–25-year-olds have already prepared cold coffee at home

These changes show that coffee remains the reference hot beverage, but usage is increasingly segmented by age. From a marketing strategy perspective, this requires much more refined and differentiated approaches.

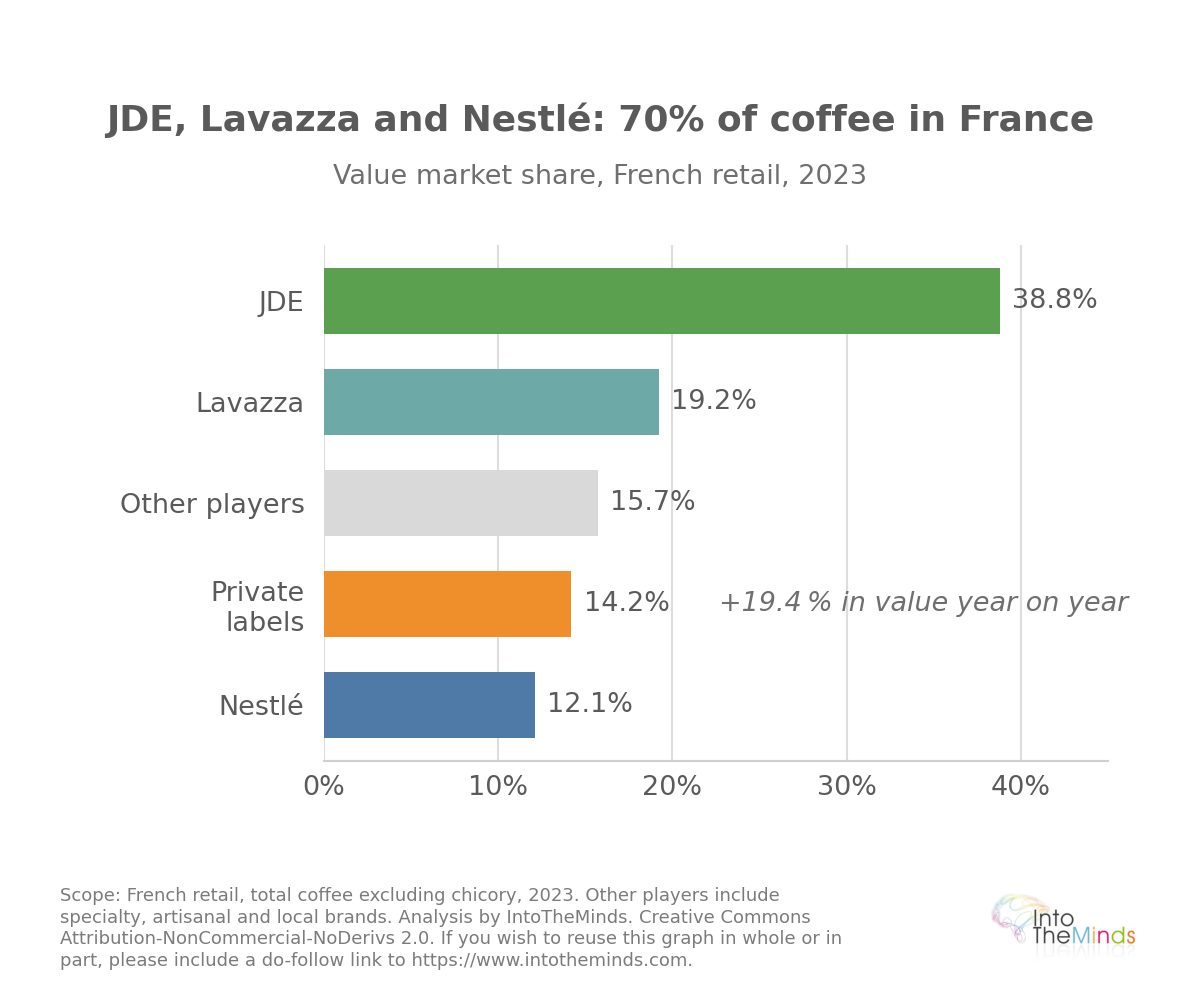

A concentrated but increasingly competitive market

The French coffee market remains structurally concentrated around a few major groups, but this dominance is increasingly challenged. Private label brands reached a 14.2% market share in value in 2023 and grew by 19.4% year-on-year. This performance illustrates how inflation has strengthened the search for more affordable options.

Major groups such as JDE, Lavazza, and Nestlé retain strong positions but must manage seemingly contradictory pressures:

- remain accessible while moving upmarket

- manage rising costs while continuing to invest in brand image

- respond to demand for simplicity while continuing to innovate

This complexity explains why the market is both structurally concentrated and yet far more open than it was 30 years ago. Today, the coffee market is dynamic and receptive to innovation, benefiting niche players focusing on premium or highly differentiated products. It can therefore be said that the market is fragmenting between volume-driven logic and value-added logic.

Analysis by format

Analysis by format

Coffee beans: the big winner

The most striking trend in the French market is the spectacular rise of coffee beans. This segment perfectly embodies new consumer expectations: quality, budget control, and consumption experience. In 2025, coffee beans account for €564.6 million and show exceptional growth of +21.6% in value and +13.7% in volume. Over ten years, volumes have literally surged, with an increase of 379%.

This performance can be explained by several competitive advantages. Beans offer a premium experience inspired by barista and coffee shop codes while remaining economically attractive. They cost at least 30% less than capsules for equivalent consumption, which is a decisive argument in the current inflationary context.

The enthusiasm for coffee is also reflected in the multiplication of physical formats. Here, the Tutto Capsule stand at the Franchise Expo 2026 in Paris. This Italian player offers 4 store formats where coffee beans and capsules coexist (hence the name).

The equipment of French households supports this trend. In 2024, 7.3 million households were equipped with bean-to-cup or ground coffee espresso machines, facilitating the adoption of this format. This growth suggests that France could foreshadow a broader European trend, where the search for high-quality yet economical coffee becomes a central trade-off.

| Segment | Revenue 2025 | Value change | Volume change |

|---|---|---|---|

| Coffee beans | €564.6M | +21.6% | +13.7% |

| Capsules | €1.35Bn | +2.1% | +2.2% |

| Ground coffee | €943.7M | +7.2% | -6.7% |

| Instant coffee | €350.4M | +1% | -0.4% |

Capsules: a mature and highly competitive segment

The capsule segment, long a growth driver in the French market, has entered a phase of strong consolidation. In 2025, it still represents €1.35 billion in revenue in France but now shows only modest growth of +2.1% in value and +2.2% in volume. This performance contrasts with the momentum of coffee beans, which benefit from price-sensitive consumer trade-offs.

The Maison Nespresso (here, the one opened in Paris) illustrates the brand’s premiumization strategy aimed at protecting its margins.

It is therefore logical that rationalization is underway. Capsules compatible with the Nespresso system continue to grow faster (+4.8% in value, +7.3% in volume) and generate €771.4 million in France. This performance reflects the premium placed on systems perceived as more universal and competitive.

Environmental issues are also weighing on this segment. The question is no longer just about convenience but about end-of-life packaging, collection, and recycling. This pressure does not condemn the segment but raises the bar of expectations. Capsules remain embedded in daily habits, but their dominance is no longer unquestioned.

Ground and instant coffee: resilience and repositioning

Ground coffee maintains its position as a cultural pillar of the French market, particularly in traditional home use. In France, it represents €943.7 million in 2025 with +7.2% value growth, but it shows a significant decline of -6.7% in volume. This evolution reflects resilience driven more by usage inertia than by expansion dynamics.

Instant coffee, meanwhile, retains a defensive position thanks to its accessibility. With €350.4 million in revenue in France in 2025 (+1% in value, -0.4% in volume), it meets expectations of convenience and budget control. In 2023, one in two French people still consumed it, with a cost per cup estimated at €0.07. In a pressured market, this affordability helps it maintain its position.

These two segments illustrate the growing segmentation of the market between experience-driven consumption and accessibility-driven consumption. They do not drive premiumization but contribute to diversification and the market’s ability to meet varied needs.

This coffee format, spotted at SIAL 2024, is very original and particularly popular in Turkey. It is an infusion-style coffee.

Trends in the coffee market

Cold coffee is trending

One of the most notable developments in the sector concerns the transformation of consumption patterns. Coffee is no longer limited to hot beverages (if you are a regular at Starbucks, you have likely already noticed this). In 2023, 32% of coffee consumed out-of-home was already drunk cold, roughly one cup in three. This 15% increase over four years confirms that it is a structural shift rather than a passing trend.

In 2023, 32% of coffee consumed out-of-home was already drunk cold, roughly one cup in three

This consumption habit inevitably affects competition in the coffee market. The product is now moving closer to the world of premium beverages (as illustrated above by the “Maison Nespresso” photo reflecting this upmarket shift) and personalized consumption experiences. Iced, concentrated, or ready-to-drink formats are particularly appealing to younger consumers, which explains the multiplication of innovations around cold brew and indulgent recipes.

This diversification of consumption occasions is redefining market dynamics. It is no longer just about selling coffee volume, but about offering a sensory experience adapted to new lifestyles. Coffee shops and specialized fast-service concepts directly benefit from this trend, which significantly expands the market’s potential.

Even though the coffee market has diversified and many specialties are now accessible, one has not yet achieved the success it deserves: Bicerin coffee. It is a Turin specialty (very indulgent!) that I had the chance to taste in the gardens of the Palazzo Reale.

The rise of specialty coffee and premiumization

A fundamental shift is gradually transforming the coffee market: the rise of specialty coffee and the adoption of more premium codes.

This trend goes beyond specialized networks and is spreading into mass retail. Highlighted origins, flavor profiles, fermented coffees, and barista ranges are multiplying. Coffee is thus aligning with dynamics observed in other premium food markets, where the challenge is to sell an identifiable sensory experience rather than a simple stimulant. During my visit to the first Maison Nespresso in Paris, I also detailed the experiential aspects integrated into the point of sale.

This evolution is particularly interesting because premiumization coexists with strong purchasing power constraints. Consumers are simultaneously seeking higher quality and better cost control, which partly explains the success of coffee beans.

Conclusion and outlook

The overall analysis reveals that the coffee market is entering a phase of lasting transition that is redefining its traditional balances. Globally, pressure on supply, prices, and logistics is reshaping competitive dynamics. In Europe, regulatory and environmental challenges add another layer of complexity.

In France, consumption remains solid but is changing in form. Coffee beans are emerging as the clear winner, capsules are slowing down, ground coffee is declining in volume, instant coffee is holding steady, and cold coffee is expanding usage occasions. This diversification reflects increasing segmentation of expectations and behaviors.

The market no longer simply contrasts entry-level and premium. It now reflects multiple visions of the product: convenient coffee, pleasure coffee, experiential coffee, economical coffee, responsible coffee. This segmentation explains both its resilience and its fragmentation. France appears to reflect a broader evolution of the European market toward a mature model—still central to daily routines but increasingly heterogeneous.

Frequently asked questions about the coffee market

Why have coffee prices increased so much in recent years?

The surge in prices is mainly due to a supply shock rather than a demand boom. Climate hazards in Brazil and Vietnam, the geographic concentration of robusta production, geopolitical tensions, and rising logistics costs explain this situation. The closure of the Suez Canal, for example, multiplied transport costs by four. These structural factors are maintaining sustained pressure on global prices.

Will coffee beans continue to grow in France?

All indicators suggest that this trend will continue. Coffee beans perfectly meet new expectations: premium experience, significant savings (30% cheaper than capsules), and ease of use thanks to the spread of automatic machines. With 7.3 million French households equipped in 2024, growth potential remains strong. This trend could even extend across Western Europe.

How are companies in the sector adapting to rising costs?

Players are deploying several adaptation strategies: partial pass-through of cost increases to selling prices, optimization of inventory management, adaptation of product portfolios, and investment in innovation. The example of Lavazza shows that it is possible to maintain profitability despite a tripling of supply costs. Companies are also focusing on differentiation and premiumization to justify their pricing.

What are the outlooks for the global market?

The outlook could improve with Brazilian production prospects. Brazil could produce 30 million bags of robusta in 2026 compared to 28 million for Vietnam, allowing a rebalancing of supply. However, this improvement remains dependent on climate conditions and geopolitical tensions. The diversification of consumption, particularly with cold coffee, also offers new growth drivers.

How can IntoTheMinds support players in the coffee market?

IntoTheMinds offers several services tailored to the challenges of the coffee sector. Our B2B market studies analyze industry dynamics and identify development opportunities. Our B2C market studies help understand changing consumer behaviors. We also conduct customer satisfaction surveys to optimize the consumer experience in this evolving market.