In this analysis, we comprehensively examine the chocolate market, its developments, innovations, and trends, and we consider its prospects to 2035. This analysis is based on the latest available data, including data collected by our firm through various quantitative studies (surveys).

Chocolate is becoming a premium product. One could almost say that rising prices are gradually moving it away from the mass-market category. While this was understandable when cocoa prices had skyrocketed, they have now returned to normal levels. Yet retail prices have not fallen. The chocolate market is therefore facing a complex situation combining declining volumes in Europe and the United States, the rise of private labels, and increasing regulatory pressure. In this analysis, our specialized market research firm has compiled the latest available figures and statistics and provides an in-depth analysis of the chocolate market. You will also find a downloadable PDF presentation at the end of this article summarizing the key conclusions and main data.

Key takeaways

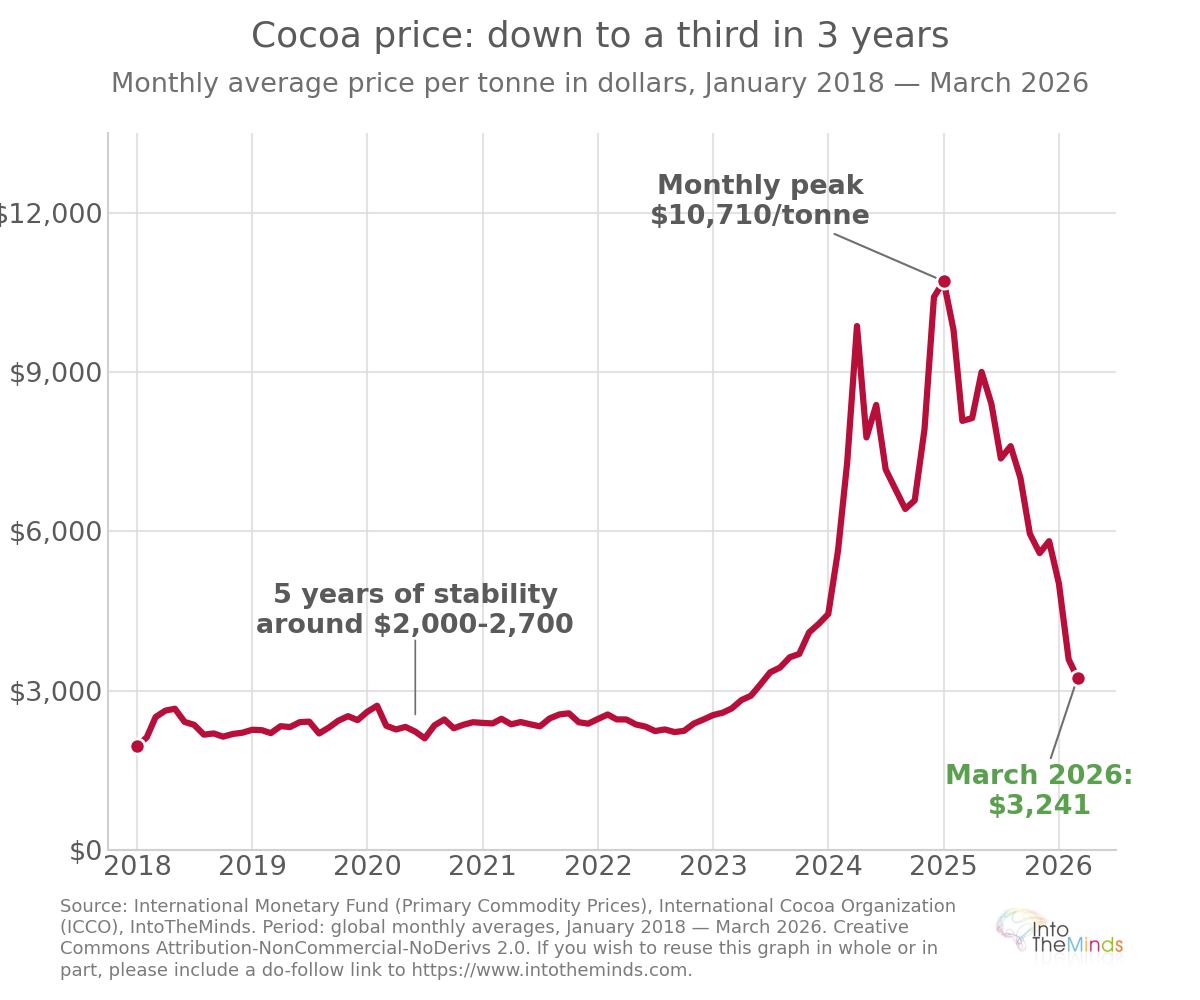

- Cocoa prices surged by 365% between January 2023 and January 2025 before collapsing below $3,000 per ton in February 2026, representing a drop of more than fourfold compared to the December 2024 peak.

- Europe accounted for 48% of global chocolate sales in 2024 and absorbed 58% of global cocoa production, making it the world’s leading market.

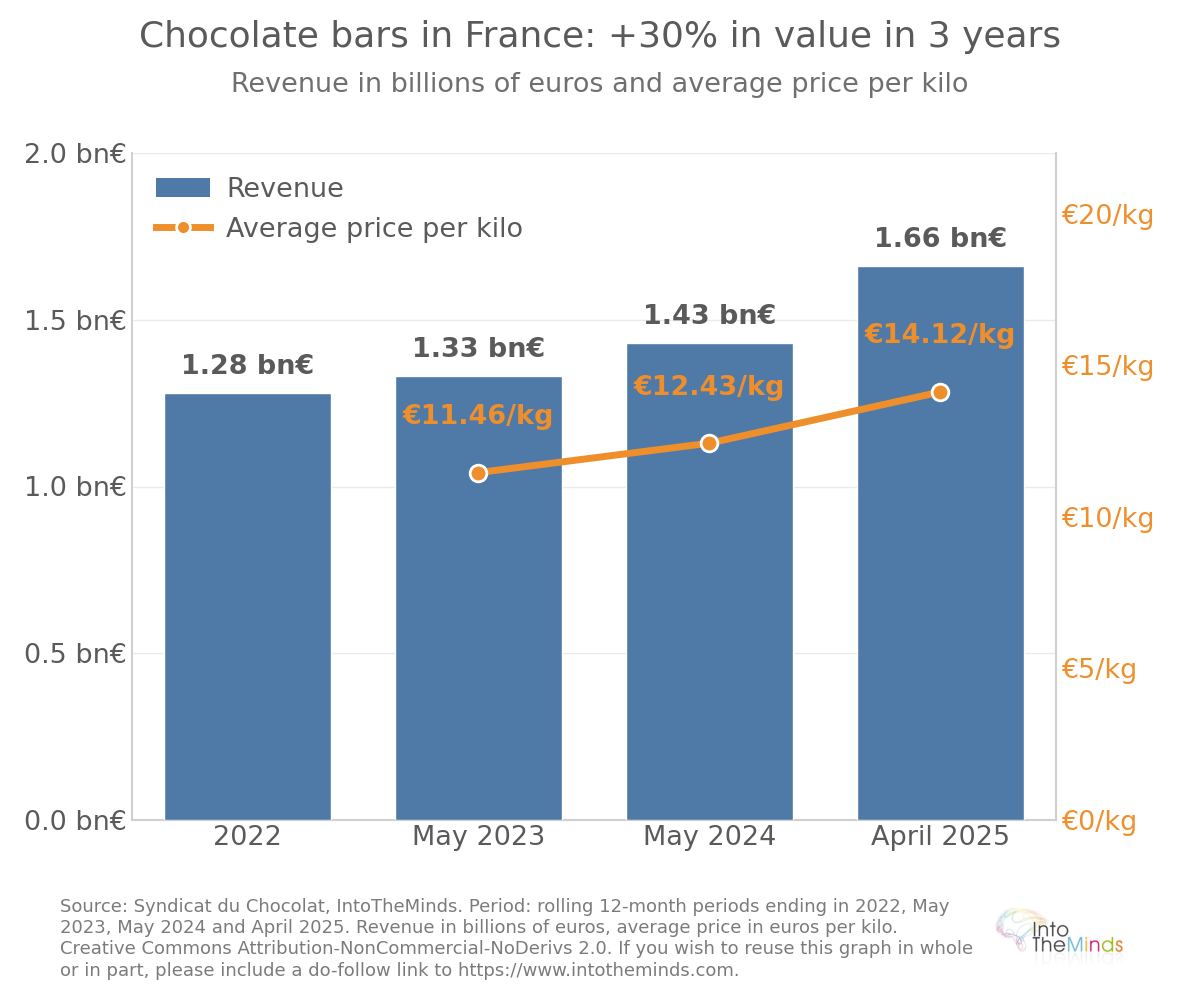

- In France, chocolate bar sales reached €1.66 billion by the end of April 2025, up +17.3% in value, driven more by price increases than by volume growth.

- Private labels are gaining ground: their value market share in chocolate bars reached 27.6% in 2025, with growth of +29.3%.

- The European Union Deforestation Regulation (EUDR), which came into force at the end of 2024 for large companies, imposes stricter traceability requirements, with fines of at least 4% of annual turnover in case of non-compliance.

Overview of the chocolate market

The global chocolate market is showing structural resilience that the 2023–2026 cocoa crisis has not fundamentally undermined. However, this cocoa crisis (see the chart below showing price trends) has reshuffled the cards between regions, players, and price segments. Inflation has forced consumers to make trade-offs, which has also influenced manufacturers’ marketing strategies. One important clarification: this analysis primarily focuses on industrial chocolate. Therefore, you will not find references to artisan chocolatiers or ultra-premium brands such as Patrick Roger.

Size and evolution of the global market

The global chocolate market was estimated at $129.6 billion in 2025, and its compound annual growth rate is projected at 3% through 2035. By then, the projected market value will reach $175.7 billion. This growth is expected to rely more on premiumization and expansion in emerging markets than on increases in physical consumption volumes.

The geographical breakdown of sales in 2024 shows clear European dominance:

- Europe: 48% of global chocolate sales

- North America: approximately 23%

- Asia-Pacific: approximately 13%

- Latin America: approximately 9%

- Middle East and Africa: approximately 5%

- Australasia: approximately 2%

Europe is also the world’s leading cocoa importer, with 58% of global production absorbed by the continent. This concentration is explained by a cultural relationship with chocolate that has no equivalent elsewhere: European consumers buy chocolate as an everyday consumer product integrated into their weekly shopping list, whereas North American and Asian markets rely more heavily on impulse purchases.

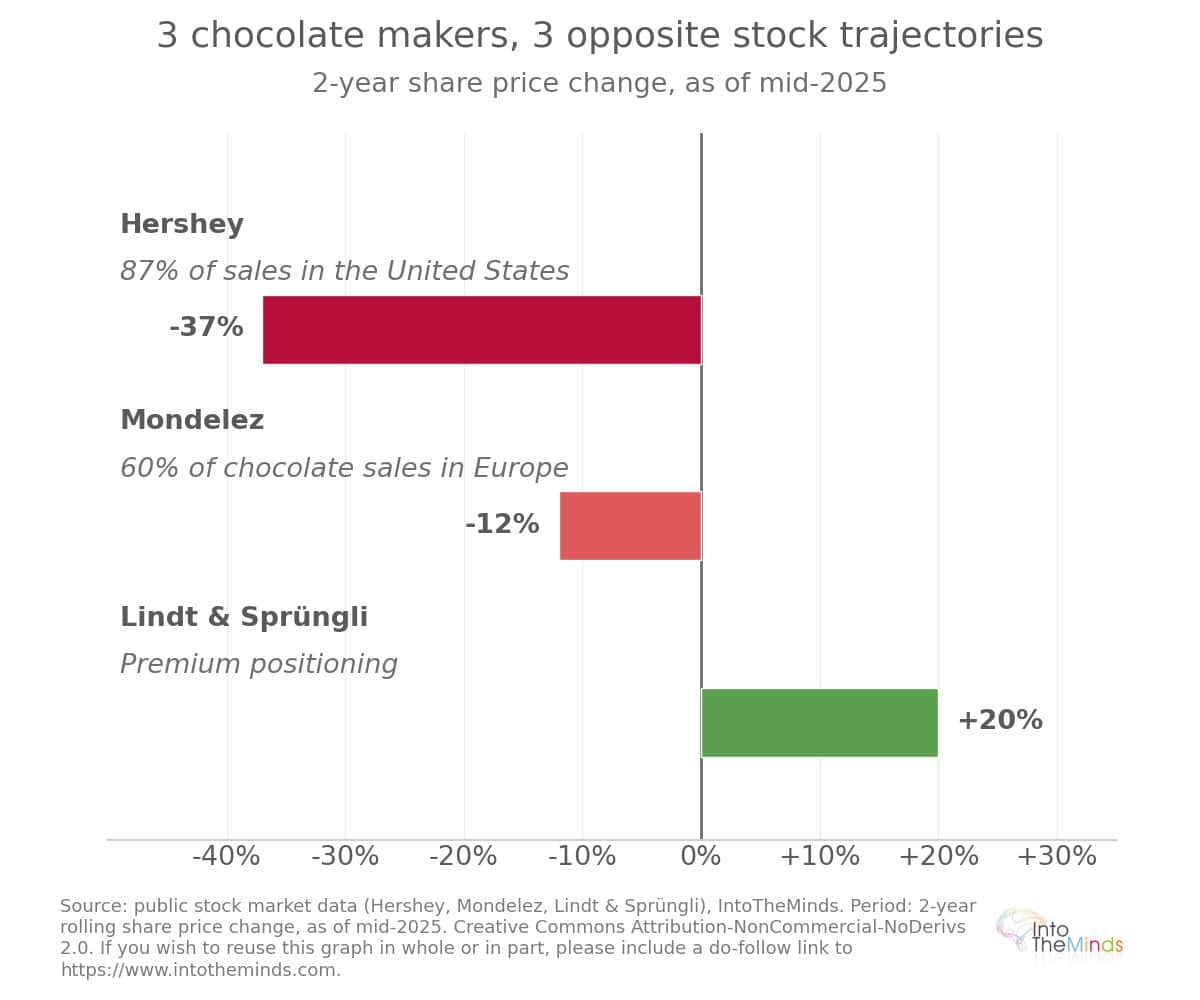

However, the global chocolate market remains highly concentrated at the top. In 2025, the top 5 groups (Mars, Mondelez, Ferrero, Hershey, and Nestlé) collectively controlled 38% of the market, with Mars leading at 12% global market share.

Chocolate consumption in France

France holds a rather unique position. Indeed, 99.3% of French households buy chocolate at least once a year. It can therefore be said that the French market is one of the most penetrated in the world. The sector includes 91 companies, 90% of which are SMEs. It directly employs nearly 30,000 people.

In 2023, the total chocolate market in France was estimated at around €3.5 billion. Half of this amount was generated by chocolate bar sales alone. The table below illustrates the dynamics within the chocolate bar segment, and you can see that despite inflation, demand remains resilient.

| Period | Chocolate bar revenue | Value growth | Volume growth | Average price per kg |

|---|---|---|---|---|

| Mid-2023 | €1.33 billion | +2.0% | -4.2% | €11.46/kg |

| Mid-2024 | €1.43 billion | +8.3% | -0.2% | N/A |

| End of April 2025 | €1.66 billion | +17.3% | +3.4% | €14.12/kg |

The cumulative increase in the average price per kilogram exceeded 23% over two years. French consumers nevertheless maintained their purchases, demonstrating a strong cultural attachment to the product. The preference for dark chocolate is particularly pronounced in France: it represents 30% of adult consumption, six times higher than the European average.

The cumulative increase in the average price per kilo of chocolate exceeded 23% over two years.

Lastly, seasonality plays a structuring role in this market. Easter represents 11.5% of annual chocolate sales in France, while Christmas accounts for 8.5%, meaning that these two periods alone account for nearly 20% of the industry’s annual revenue. For Easter 2025, seasonal chocolate sales reached €435.5 million (+5% in value), but the number of purchasing households declined from 58.7% to 54.7%. This reflects a widening gap between loyal consumers and those turning away from the category due to rising prices. Growing price sensitivity is therefore evident, and shrinkflation practices have likely only exacerbated the phenomenon.

Market leaders and market shares

The competitive structure of the chocolate market in France combines international groups and national players. Among the companies with production facilities in France are Barry Callebaut, Cémoi, Ferrero, Lindt & Sprüngli, Mondelez, Mars, and Nestlé. The network of chocolate SMEs includes companies such as Valrhona, Weiss, and Abtey.

France is the fourth-largest market worldwide for Lindt & Sprüngli, with approximately €430 million in revenue in 2023 (+5.3%). The group’s premium positioning enabled it to weather the inflationary period better than its competitors: its 2023 profit increased by 17.9% to 671.4 million Swiss francs despite rising raw material costs (see stock market performance chart below).

As for private labels, their value market share in chocolate bars reached 27.6% in 2025, with annual growth of +29.3%, compared to +13.3% for national brands. The price gap nevertheless remains significant: around €10/kg for private labels versus nearly €16/kg for national brands.

Segmentation and chocolate product categories

From a marketing perspective, the chocolate market is far from homogeneous. Its segmentation by product type, packaging format, and distribution channel reveals highly different dynamics depending on the category, which is crucial for companies’ strategies in the sector.

Breakdown of sales by chocolate type

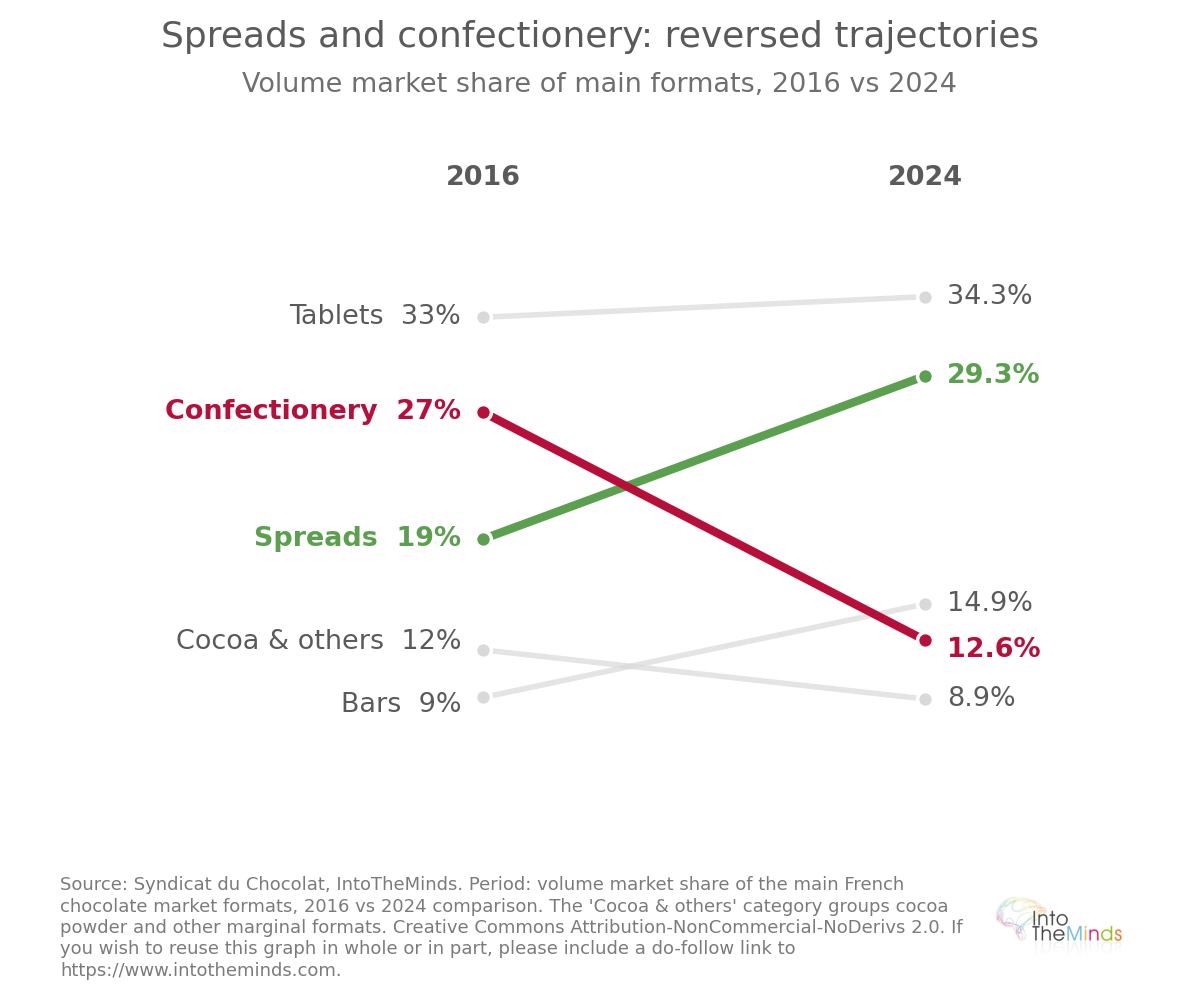

In France, chocolate bars lead product category sales with 34.3% of volume sales in supermarkets and hypermarkets, ahead of chocolate spreads (29.3%), bars (14.9%), chocolate confectionery (12.6%), and chocolate breakfast products (9%). This structure differs slightly from 2016 data, which placed chocolate confectionery in second position (27%) ahead of spreads (19%). The chocolate spread segment is probably the most competitive today, as its growth rides on consumers’ need for comfort food. Market leader Nutella is seeing its market share challenged by competitors such as Rigoni Di Asiago with its Nocciolata brand.

The market share of chocolate spreads has increased by 10 percentage points since 2016

Globally, milk chocolate dominates with around 59% of the total market. Its balanced taste and smooth texture make it the universal entry-level product. Dark chocolate, perceived as more premium and benefiting from a favorable health image, is gaining ground, especially in France where it accounts for 30% of adult consumption. White chocolate remains a limited segment, mainly used in pastry-making and personalized confectionery.

Packaging trends and consumption formats

Plastic film or flexible packaging represents 43.1% of the global chocolate packaging market in 2025. Its lightweight nature, controlled cost, and ability to preserve freshness make it the dominant format for chocolate bars and snacks. Cardboard or fiberboard packaging, considered more premium, is preferred for gift boxes and assortments, especially during Christmas and Easter.

Easter and Christmas account for 20% of the chocolate industry’s annual revenue

Seasonality strongly shapes consumption formats in France. Molded chocolates account for 31% of Easter season revenue (€134.8 million in 2025), followed by seasonal specialties (€106.9 million) and permanent specialties (€45.4 million).

Innovations and new categories

Two phenomena have marked the chocolate market in recent years. On the one hand, the virality of Dubai chocolate (the chocolate-pistachio-kataifi combination) attracted more than 140,000 French households and generated nearly €4 million in revenue during the first four months of 2025. This illustrates the power of social media over purchasing behavior. On the other hand, KitKat’s entry into the chocolate bar segment for its 90th anniversary involved a €40 million investment in a Bulgarian factory and attracted 182,000 buyers as early as February 2025, contributing 12% of the segment’s growth.

Cocoa-free alternatives represent a deeper structural innovation. Products based on sunflower seeds and roasted and fermented oats, developed by Planet A Foods under the ChoViva brand, claim a carbon footprint 74% lower and costs 25% to 30% lower than traditional chocolate. Alsatian chocolatier Abtey already uses this technology for a quarter of its range, with a repurchase rate of 66% and 98% positive reviews. Other avenues are being explored: carob, roasted barley, fermented fruits and legumes, and even lab-grown cellular cocoa.

Key trends and outlook for the chocolate market

The cocoa crisis of 2023-2026 acted as a revealer of the sector’s structural weaknesses while accelerating transformations already underway. In this final chapter, we discuss the fair-trade trend applied to the chocolate market, changes in consumer behavior, and conclude with prospects through 2035.

Sustainability and fair trade

The European Deforestation Regulation (EUDR) came into force on December 30, 2024 for large companies, and on June 30, 2025 for SMEs and microbusinesses. It prohibits the import into Europe of cocoa originating from areas deforested after December 31, 2020, under penalty of fines amounting to at least 4% of annual turnover. This regulatory constraint accelerated investments in traceability across the entire supply chain.

However, not all countries are at the same level regarding efforts to ensure transparency within the supply chain. Here are some indicators:

- Share of certified cocoa: 100% in Germany, 82% in Switzerland, 63% in France

- Fair trade: 20% of cocoa in Germany versus 8% in France

- Households linked to the IFCD exceeding the living income threshold: 12% in Belgium, 11% in Germany, 1.8% in France

- Traceability down to the plot level: 49% for French manufacturers, but only 6% for retail chains

- Child labor prevention systems: 54% of households in the Netherlands, 45% in Belgium, 32% in France

Despite the regulatory emphasis placed on fair trade, it remains marginal in sales figures. Total fair-trade sales reached €2.1 billion in 2022, four times more than in 2015. Chocolate bars represent 43% of fair-trade sales in sweet grocery products. Supermarkets account for 46% of these sales, while specialized networks account for 22%.

The Easter period represents about 13% of annual chocolate sales in France.

Evolution of consumer preferences

The inflation crisis has polarized the chocolate market between two opposing purchasing behaviors:

- On one side, price-seeking consumers are massively shifting toward private label brands. Their value growth is spectacular (+29.3% in 2025 in France, for example). It also significantly outpaces national brands (+13.3%).

- On the other side, an affluent customer base remains loyal to premium brands and accepts significant price increases: Lindt has reported double-digit growth in store sales despite repeated price hikes.

Several underlying trends are also reshaping chocolate consumer expectations:

- Premiumization: growing demand for single-origin, bean-to-bar, and artisanal chocolates

- Health and wellness: development of sugar-free chocolates, protein- or probiotic-enriched products, and vegan alternatives

- Ethics and traceability: increased sensitivity to cocoa production conditions and child labor issues

- Virality and experience: success of social media-inspired formats (Dubai chocolate) and in-store theatrical presentation

- GLP-1 medications: in the United States, the widespread use of obesity and diabetes treatments, known to reduce cravings for sweets, adds additional pressure on volumes. As shown in this analysis, the rise of these drugs is deeply changing consumption habits.

The divergence between Europe and North America is particularly striking. European cocoa demand fell by 7.8% year-on-year in Q1 2026, compared to 3.8% in North America, confirming that the US market is more resilient in volume despite a decline in units sold (-2% over 52 weeks ending mid-2025). US chocolate spending reached $23.5 billion in 2025, up 39% since 2020, but this growth is almost entirely price-driven: the average unit price reached $3.68 in late March 2026, up 10% year-on-year.

The premiumization of the chocolate market leads to polarization: on one side industrial chocolates, and on the other high-end artisanal chocolates such as those of Patrick Roger.

Growth projections 2026–2035

The global chocolate market is expected to grow at around 3% per year in value through 2035, reaching $175.7 billion. This growth will be driven mainly by:

- Expansion in emerging markets, particularly India, Mexico, and Latin America, where urban growth and rising disposable income are boosting consumption

- Premiumization in mature markets, which supports value even when volumes stagnate

- Development of e-commerce and direct-to-consumer channels, enabling more personalized brand experiences

- Product innovation, including partial or full cocoa alternatives, which could expand the addressable market

The main uncertainty concerns cocoa supply. Maintaining global production of 5 million tons per year requires massive investment in plantation regeneration, greater professionalization of the supply chain, and sufficient farmer compensation to prevent younger generations from abandoning cocoa farming. Without these conditions, the price volatility observed between 2023 and 2026 risks repeating itself.

FAQ: The questions you are asking

How is the chocolate market performing in France in 2026?

The chocolate market in France shows notable resilience in value terms, even though volumes remain under pressure. Tablet sales revenue reached €1.66 billion by the end of April 2025, up +17.3% in value, driven by significant price increases. In 2026, the decline in cocoa prices (below $3,000/ton in February 2026) is expected to gradually feed through to consumer prices, but with a lag of several months due to raw material hedging already contracted by manufacturers. Companies seeking a deeper understanding of the French market can rely on a B2C market study to identify growth segments and emerging purchasing behaviours.

Who are the leaders in the chocolate market?

At global level, the five largest groups (Mars, Mondelez, Ferrero, Hershey and Nestlé) collectively control 38% of the market in 2025, with Mars leading at 12%. In France, major players include Barry Callebaut, Cémoi, Ferrero, Lindt & Sprüngli, Mondelez, Mars and Nestlé among international groups, along with a dense network of SMEs such as Valrhona, Weiss and Abtey. Lindt & Sprüngli has been particularly resilient during the crisis thanks to its premium positioning, posting a 17.9% profit increase in 2023 despite surging raw material costs.

What is the growth rate of the global chocolate market?

The global chocolate market is expected to grow at a compound annual growth rate (CAGR) of 3% between 2026 and 2035, reaching $175.7 billion. This growth is mainly driven by premiumisation in mature markets and expansion in emerging markets (India, Mexico, Latin America). Physical volumes are growing more slowly than value, confirming that growth is driven more by price increases than by higher per-capita consumption.

What are the sustainability challenges in the chocolate industry?

The EU Deforestation Regulation (EUDR), which came into force at the end of 2024, requires full traceability of cocoa back to the plot, with fines of at least 4% of annual turnover. France lags behind Germany, Belgium and Switzerland in certified cocoa (63% vs 100% in Germany) and fair trade (8% vs 20% in Germany). In addition, 5.5 million cocoa farmers worldwide still live in poverty, threatening the long-term sustainability of the supply chain. Companies wishing to assess their positioning on these issues can use customer satisfaction surveys with clients and partners.

How are chocolate manufacturers responding to cocoa price volatility?

Faced with rising cocoa prices (up to $12,931/ton in New York in December 2024), manufacturers have adopted three main strategies. The first is passing price increases on to consumers: Cémoi raised prices by an average of 25% in August 2024, and Hershey announced increases of 13–20% in 2025. The second is recipe reformulation, reducing cocoa content or using substitutes such as Planet A Foods’ ChoViva products. The third is focusing on premiumisation and marketing innovation to maintain perceived value. Companies wishing to test pricing or new formulations with consumers can rely on targeted opinion surveys.

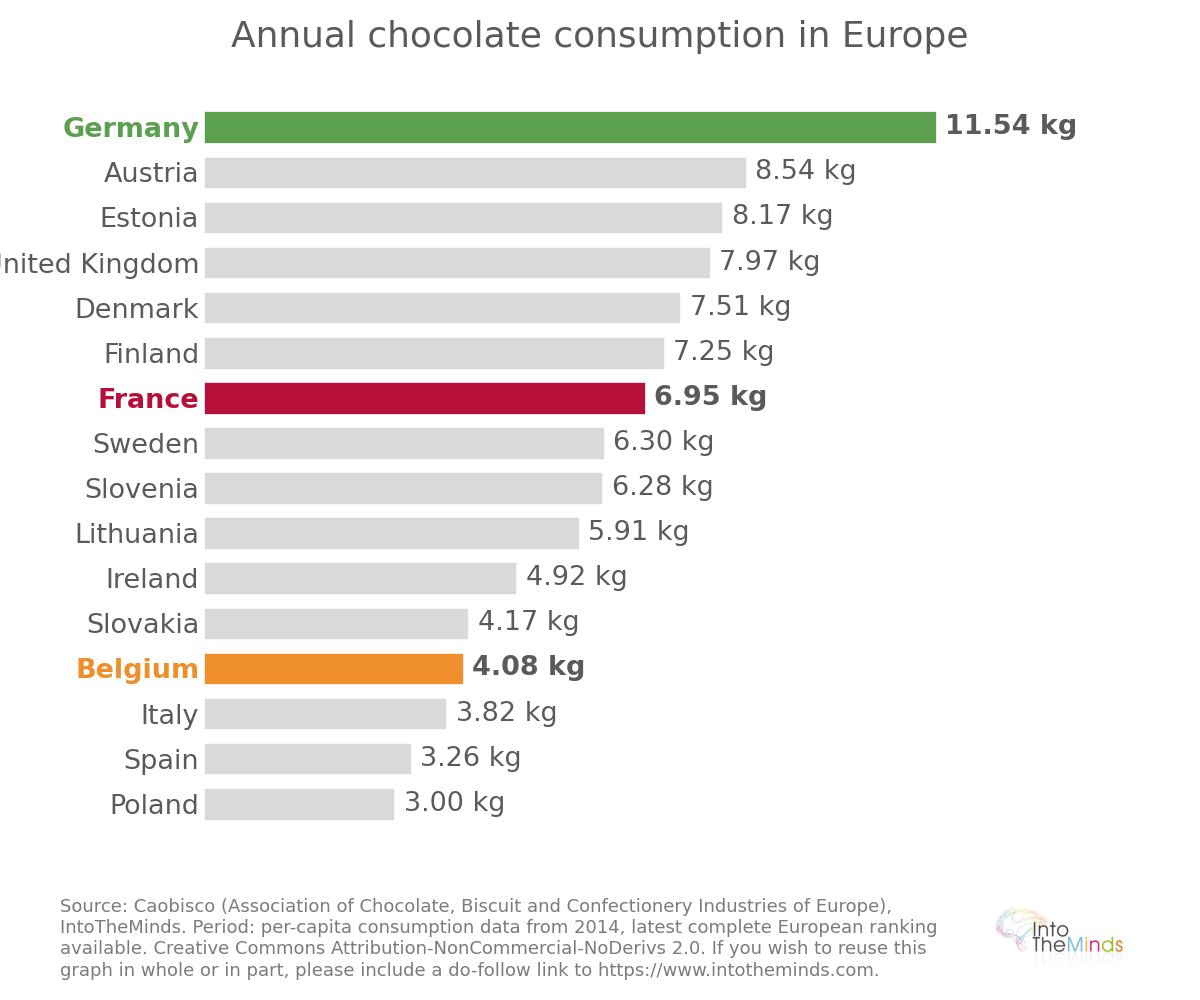

What is per capita chocolate consumption in Europe?

Per capita consumption differences remain very significant in Europe. In 2014 (latest comparable country data), Germany led with 11.54 kg per person per year, followed by Austria (8.54 kg), Estonia (8.17 kg), the United Kingdom (7.97 kg) and Denmark (7.51 kg). France ranked 7th in Europe with 6.95 kg per capita, well ahead of Poland, which ranked last at 3 kg. These differences reflect deep cultural variations in chocolate consumption, which directly influence distribution strategies and brand positioning across markets.

![Illustration of our post "LinkedIn Top Voice: who are these influencers? [Research]"](/blog/app/uploads/algorithme-linkedin-2022-120x90.jpg)

![Illustration of our post "In-store digital: customers want efficiency [Survey]"](/blog/app/uploads/flagship-store-lacoste-paris-champs-elysees-14-120x90.jpg)