![These 3 online banks are evolving their business model [Analysis].](/blog/app/uploads/revolut-stays.jpg)

Despite the record profits recorded by banks in 2021, their margins remain under pressure and their business model under attack from all sides by FinTech’s. Slow to change and evolve, they are being overtaken by online banks, some of which have decided to develop their business model by diversifying. Some like Revolut, Tinkoff, and Yono SBI propose to make purchases directly from the app. This movement is not insignificant and foreshadows what already exists in China with WeChat: the use of a “super app” as a unique gateway to daily life activities. Successfully imposing this “super app” model can be significant and will undoubtedly be disruptive for e-tailers.

If you only have 30 seconds

- Revolut proposes to book your hotel from its app to simplify travel logistics

- A Russian online bank (Tinkoff Bank) already proposes this service

- The YONO app launched by the State Bank of India (SBI) is a super app launched in 2015 that allows you to make purchases without leaving the app

- Online banks will seek to diversify because traditional banking activities are not profitable enough

- Super apps will allow them to become a single gateway to daily activities. The access to this single gateway will be paid for by the partners, as well as the access to transactional data

Revolut and travel booking

Revolut is about to launch Stays, a travel booking service that it has just tested in Great Britain and Ireland. In practice, Revolut proposes to its 16 million members to make accommodation reservations among 700,000 available on “Stays.” Revolut has partnered with a booking platform whose identity has not been revealed to suggest such a choice of accommodations.

A cashback system is proposed, which allows to get back on its Revolut account between 7,5% and 10% of the reservation amount.

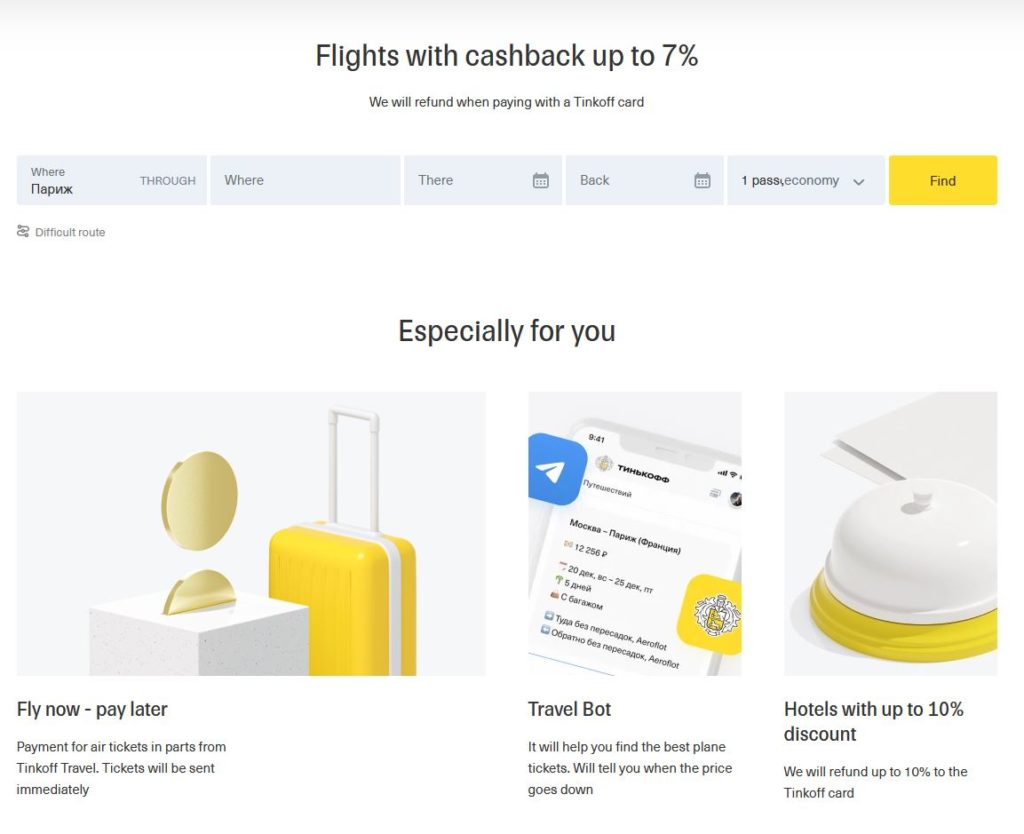

Tinkoff Bank also proposes to book trips

Tinkoff Travel is the travel booking service proposed by the Russian online bank Tinkoff Bank. It also works with a cashback system and allows you to book your plane or train tickets, a rental car, a hotel, or a complete trip. The partners of Tinkoff Travel are known: Star Alliance, Oneworld, and SkyTeam.

Yono proposes to book train tickets

YONO is the digital platform of the State Bank of India (SBI), launched in 2015. The Yono SBI app provides access to traditional banking services as well as loan requests and purchases. Apart from train tickets and air tickets, the app also includes purchases in other categories and proposes “deals” with online sales platforms.

YONO stands for “You Only Need One,” and this acronym alone summarizes the philosophy of this unique gateway to daily activities.

Analysis

The business model that is emerging with the “super app” is disruptive for many B2C sectors. It is indeed a unique entry point, controlled by the bank, to the consumer. Therefore, the bank may find itself in a solid position to impose its conditions on companies wishing to do business with its customers. If unique partnerships are formed between banks and e-merchants, the choice of a bank could no longer be dictated solely by financial considerations. Like in the airline industry, one would choose one’s company according to the loyalty program it has signed up for.

The other disruptive aspect of super apps is access to data. By making purchases directly from the bank’s application, the bank has access to everything. Nothing escapes it anymore. The picture it will draw of the customer and his habits will be even more complete than today. This precision has a price that banks will not fail to monetize to third parties.

The opinion of Thibault de Barsy, Vice President of the Emerging Payments Association

The success of the Chinese-style super-app (AliPay and WeChat pay) is the model admired by all fintech’s in the rest of the world. Its resounding success lies essentially in the perfect integration of all the financial needs of the individual: paying, cashing, saving, investing, borrowing, and even insuring… the life cycle. But the Chinese authorities are putting the brakes on this too-perfect “coupling” between all these functions and want to break the perfectly assembled Lego into separate blocks. In a recent television interview with CNBC, Warren Buffet himself was positively surprised that the Chinese authorities are doing what the American regulators have not dared to do. In Europe, we wouldn’t even dare to count the number of regulations that would limit such super-apps: dominance, coupled sales, Mifid, … However, the recommendation of a financial product based on behavioral data analysis has never had such a bright future! The proof is the rise of “Buy Now Pay Later” worldwide via the fintech Klarna (Sweden). The tools are there (AI) and the data too! They can even be shared within a secure framework regulated by European-style Open Banking. In conclusion, in the debate that pits “market forces” against the power of the regulatory norm, European financial players are well placed. Still, they are entitled to request greater coherence between regulations that are a priori distinct (“Open Banking” versus “GDPR” is the most obvious example) but yet contradictory for many innovative services.

The success of the Chinese-style super-app (AliPay and WeChat pay) is the model admired by all fintech’s in the rest of the world. Its resounding success lies essentially in the perfect integration of all the financial needs of the individual: paying, cashing, saving, investing, borrowing, and even insuring… the life cycle. But the Chinese authorities are putting the brakes on this too-perfect “coupling” between all these functions and want to break the perfectly assembled Lego into separate blocks. In a recent television interview with CNBC, Warren Buffet himself was positively surprised that the Chinese authorities are doing what the American regulators have not dared to do. In Europe, we wouldn’t even dare to count the number of regulations that would limit such super-apps: dominance, coupled sales, Mifid, … However, the recommendation of a financial product based on behavioral data analysis has never had such a bright future! The proof is the rise of “Buy Now Pay Later” worldwide via the fintech Klarna (Sweden). The tools are there (AI) and the data too! They can even be shared within a secure framework regulated by European-style Open Banking. In conclusion, in the debate that pits “market forces” against the power of the regulatory norm, European financial players are well placed. Still, they are entitled to request greater coherence between regulations that are a priori distinct (“Open Banking” versus “GDPR” is the most obvious example) but yet contradictory for many innovative services.

![Illustration of our post "Porsche: Strategy and Scenarios for Overcoming the Crisis [Analysis]"](/blog/app/uploads/porsche-taycan-carrera-911-120x90.jpg)