Drone deliveries are becoming increasingly widespread, but not at the same pace in all countries. We present the latest facts and analyses on the subject and explain why they could be a game-changer for the supply chain.

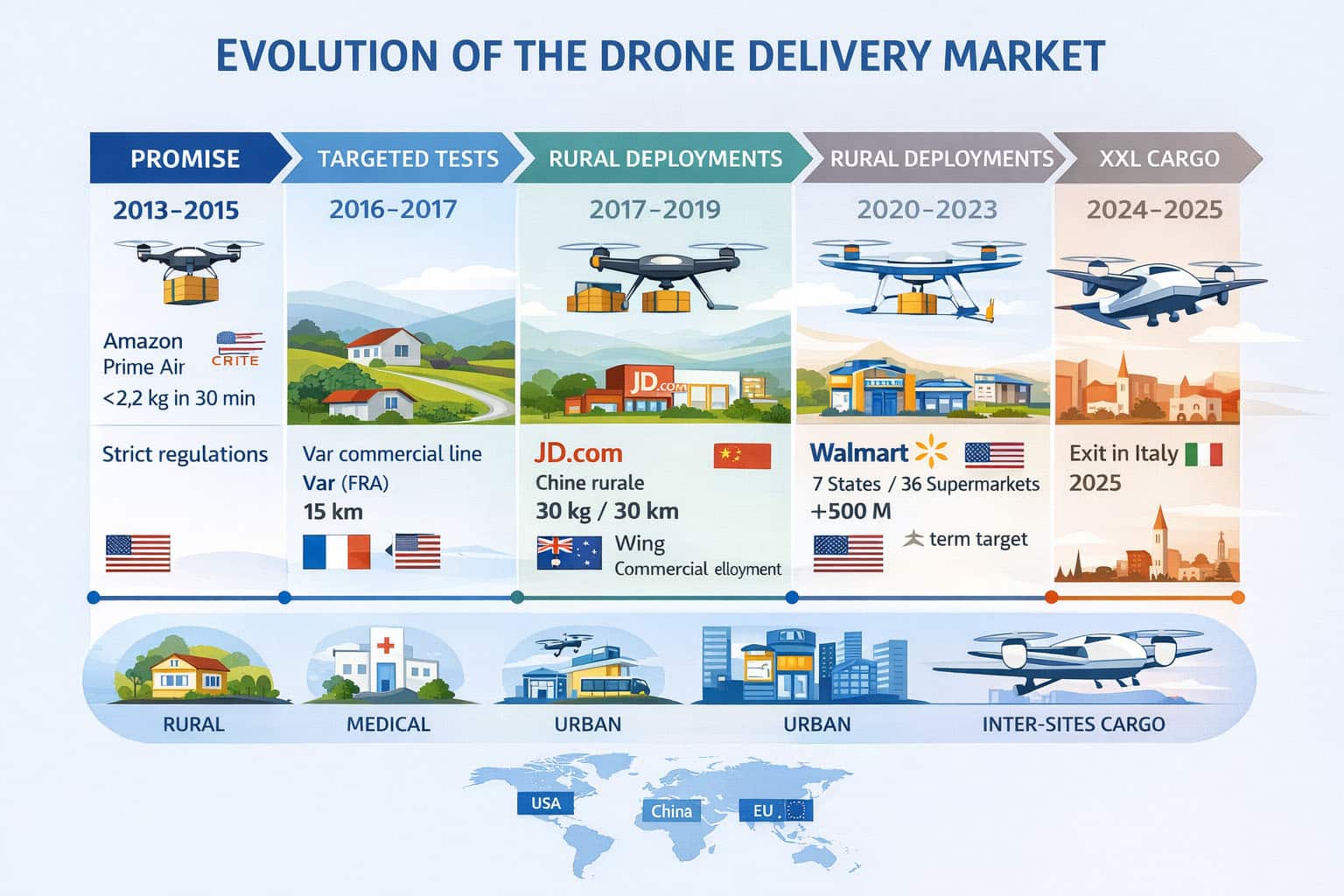

Drone package delivery has reached a decisive milestone in recent years. What was still science fiction in 2013 has now become an operational reality in several regions of the world. Between ambitious commercial promises and strict regulatory constraints, the drone delivery sector is gradually shaping a new logistics model. It represents a low-cost solution for the “last mile” problem that contributed to the decline of quick commerce. In this article, the IntoTheMinds research firm leverages its knowledge of the logistics sector to analyze the evolution of the global drone delivery market, its geographical dynamics, and the emerging prospects for the next decade.

Contact the IntoTheMinds market research firm

Key Takeaways

- The global drone delivery market was valued at $30.6 billion in 2022 and is projected to reach $101.1 billion by 2030

- As early as 2018, China dominated the sector with 40 drones serving about 100 villages. These drones handle cargo transport up to 30 kg and 30 km

- Rural and remote areas represent the most profitable application for this technology. Drones offer affordable solutions to associated mobility challenges.

- Amazon aims for 500 million packages delivered by drone annually before 2030, but remains limited to 2 U.S. cities in 2023

- Europe is advancing its infrastructure with potential estimated at €14.5 billion by 2030

The Early Years (2013-2017): Between Promises and Technical Realities

The modern history of drone delivery truly began on December 2, 2013 in the U.S., when Amazon unveiled Prime Air. The company set a clear ambition: to deliver packages up to 2.2 kg in under 30 minutes, representing 86% of its shipments. This attractive commercial promise quickly faced civil aviation constraints. The presentation video of the time (see below) was very ambitious and awakened minds to an important innovation for “last mile” coverage. Strategically, Prime Air helps make the entire logistics chain more autonomous, from delivery to in-store product availability with Amazon Go.

By March 20, 2015, U.S. authorities imposed strict testing regulations:

- Daytime flights only

- Maximum altitude of 112 meters

- Drone must remain within visual line of sight of a licensed pilot

These restrictions revealed the gap between marketing ambition and operational reality. Immediate, low-cost solutions remained out of reach.

The first concrete demonstrations emerged in 2016-2017, but in highly controlled environments. On December 7, 2016, Amazon completed its first Prime Air delivery in the UK near Cambridge in 13 minutes, with a maximum payload of 2.5 kg. Meanwhile, France’s La Poste launched a commercial line in the Var region in December 2016, authorized by DGAC:

- 15 km distance

- Once weekly

- Cruising speed of 30 km/h for packages up to 3 kg

This period revealed a fundamental trend: the most credible deployments favored controlled environments and high-value applications. In September 2017, Matternet established an automated network in Switzerland for medical sample transport, reducing transit times from 20 minutes by road to 3 minutes by air over 20 km. Healthcare was identified early as a promising sector for drone delivery.

The Emergence of Two Distinct Models (2017-2019)

Between 2017 and 2019, the market structured itself around two distinct models that persist today.

The Chinese Model: Rural Industrialization

China gained significant lead with JD.com, which launched what could be called a “commercial” line in rural Shaanxi province in June 2017. By June 2018, the company already operated 40 drones serving about 100 villages in Shaanxi and Jiangsu provinces. The largest aircraft could carry up to 30 kg for about 30 km.

This strategy addressed a major economic challenge: JD.com, with $55.7 billion revenue in 2017, noted that rural delivery costs five times more than urban delivery. The goal was to reach 600 million people living in the countryside, representing 45% of China’s population. The project mobilized 200 researchers since October 2015.

The Western Model: Urban Last Mile

In May 2019, Wing (an Alphabet subsidiary) became the first commercial drone delivery service in Australia, in Canberra’s suburbs. The service offered an 8 km radius for payloads up to 1.2 kg, with gradual scaling via registration.

This geographical dichotomy reflects different strategic approaches: China focuses on rural logistics and large volumes, while the West prioritizes urban last-mile and speed promises.

Amazon aims for 500 million packages delivered by drone annually before the end of the decade

The Maturity Phase (2019-2023)

The Battle of American Giants

Between 2019 and 2023, U.S. players intensified development efforts, but results fell short of announcements.

In September 2020, Walmart conducted tests with two partners:

- Zipline targeted an 80 km radius with delivery under one hour, but initially focused on health and wellness

- In November 2021, the Walmart/DroneUp service launched in Arkansas with flights limited to just 1.85 km

Amazon’s return in October 2023 marked an ambitious turn: the company announced plans for 500 million drone deliveries annually “before the decade’s end.” The MK30 drone (see video above) promises a 25 km radius, maximum payload of 2.5 kg, and 40% less noise. However, Prime Air remains active in only 2 cities (Lockeford, California and College Station, Texas) with about 2,000 registered customers.

By late August 2023, Walmart appeared more advanced in territorial coverage with drone delivery from 36 stores across 7 states. This period illustrates the persistent gap between commercial ambitions and regulatory/industrial capabilities.

France: Advanced Experimentation, Limited Deployment

France perfectly illustrates sector challenges. As of April 2019, the Var line remained the only commercial route authorized by DGAC. Results were modest: 91 packages delivered since opening, 95% success rate, 260 flight hours in the previous year (half for testing).

Infrastructure progressed faster than usage, leaving few case studies. In February 2024, Essonne established a drone corridor for deliveries within 20 km (ultimate goal: 56 km). Drones fly at maximum 120 meters altitude and can reach 110 km/h, primarily over fields.

In October 2021, Rungis market hosted about 50 internal flights transporting various goods including a defibrillator. The operation required a vertiport and dedicated team.

These two cases remain very limited, ultimately involving just two companies.

What’s the Future of Drone Delivery?

The Shift Toward Cargo Drones (2024-2025)

2024 marks notable evolution: the market extends beyond last-mile to heavier cargo drones for intermediate links. Business-to-business delivery is opening.

In China, Tengden is developing a civil cargo drone capable of carrying 2 tons of freight for 600-1,800 km. In Europe, Dronamics designs the “Black Swan” for 350 kg over 2,500 km (see video below), with claimed costs around €5 per kilogram and planned postal partnerships for Greek islands.

Meanwhile, pragmatic uses persist: in France’s Vercors since 2016, a postal drone carries 8 packages totaling 10 kg over 10 km.

Market Projections and Regulatory Realities

In December 2025, the European Commission mentioned €14.5 billion potential by 2030 for Europe. Germany would grow from €955 million in 2022 to over €1.7 billion in 2030. Potential emissions reduction of 180 million tons CO2-equivalent is cited for various use cases.

However, regulations can abruptly halt projects. In December 2025, Amazon announced stopping commercial drone delivery plans in Italy after a “strategic review,” despite successful December 2024 tests in San Salvo (Abruzzo). Cited reasons involved commercial and regulatory conditions.

Beyond regulatory constraints, drone development and manufacturing challenges exist. China dominates component supply. Achieving autonomy is crucial for European security, especially with the Cybersecurity Act revision by the European Commission.

Market Evolution Outlook (2025-2035)

Analysis of the past decade provides insight into the most promising use cases:

- Rural and remote areas: The most operational figures appear where mobility is limited. China serves 100 villages, France uses mountain corridors and the Var line. Economic and operational advantages are easier to demonstrate here.

- Medical and emergency sector: Time savings are clear. Swiss experience showed 3 minutes by drone versus 20 minutes by road. Added value justifies infrastructure costs. Again, drones solve mobility challenges for healthcare.

- Closed sites and internal logistics: These markets enable rapid testing (warehouses, industrial zones, wholesale markets) for value-added logistics services. Controlled environments facilitate regulatory acceptance.

- Dense urban and consumer markets: Progress remains slower, hindered by safety, noise, traffic management and social acceptance. Operations may still be discontinued, as in Italy in 2025. However, drone delivery could solve problems caused by quick commerce and its dark stores.

Market Evolution by Region

| Region | 2018 | 2023 | 2025 | 2030 Projection |

|---|---|---|---|---|

| China | 40 drones, 100 villages | Continued expansion | 2-ton cargo drones | Global leader |

| United States | Limited testing | 36 Walmart stores, 2 Amazon cities | 500M packages/year target | Mass deployment |

| Europe | Experiments | Infrastructure corridors | €14.5B potential | Mature market |

| France | Var line | Essonne corridors | 91 total deliveries | Specialized niche |

Frequently Asked Questions About Drone Delivery

What are the main obstacles to drone delivery development?

Regulatory constraints dominate: altitude limits, visual line-of-sight requirements, weather restrictions and no-fly zones. Noise pollution and social acceptance also pose major challenges in dense urban areas.

Is drone delivery truly eco-friendly?

For packages up to 2 kg, ADEME’s SHERPA study shows drone carbon footprint represents less than 1% of a light utility vehicle’s, from manufacturing to operation. Ecological benefits depend on local energy mix and usage frequency.

When will drone delivery become widespread?

Projections vary by region. Amazon targets 500 million annual deliveries before 2030 but remains limited to 2 cities in 2023. Europe anticipates a €14.5 billion market by 2030. Widespread adoption depends on regulatory evolution and social acceptance.

What types of packages can be delivered by drone?

Current commercial drones carry between 1.2 kg (Wing in Australia) and 30 kg (JD.com in China). New cargo drones target 350 kg to 2 tons. Fragile, medical and urgent items represent the most suitable segments.

Will drone delivery replace other transport methods?

No, the market trends toward hybridization. In dense areas, cargo bikes remain competitive with 5 delivery points/hour versus 3 for vans. Drones complement rather than replace logistics, especially for hard-to-reach areas.

![Illustration of our post "75% of backlinks come from translations [Research]"](/blog/app/uploads/langues-langages-talen-120x90.jpg)