This article provides a comprehensive overview of the high-protein food market. The consumption of GLP-1 appetite suppressants is driving innovation in the sector, impacting all product categories.

The market for high-protein foods is experiencing significant growth in industrialized countries. This trend is driven by evolving consumption habits, notably influenced by appetite suppressants like Ozempic, as well as a growing interest in sports nutrition. High-protein products are now attracting a broader audience, well beyond elite athletes. Drawing on our experience in market research in France and internationally, we provide a comprehensive overview of the drivers of this market, current trends, and future developments.

Contact the marketing research institute IntoTheMinds

Key Takeaways

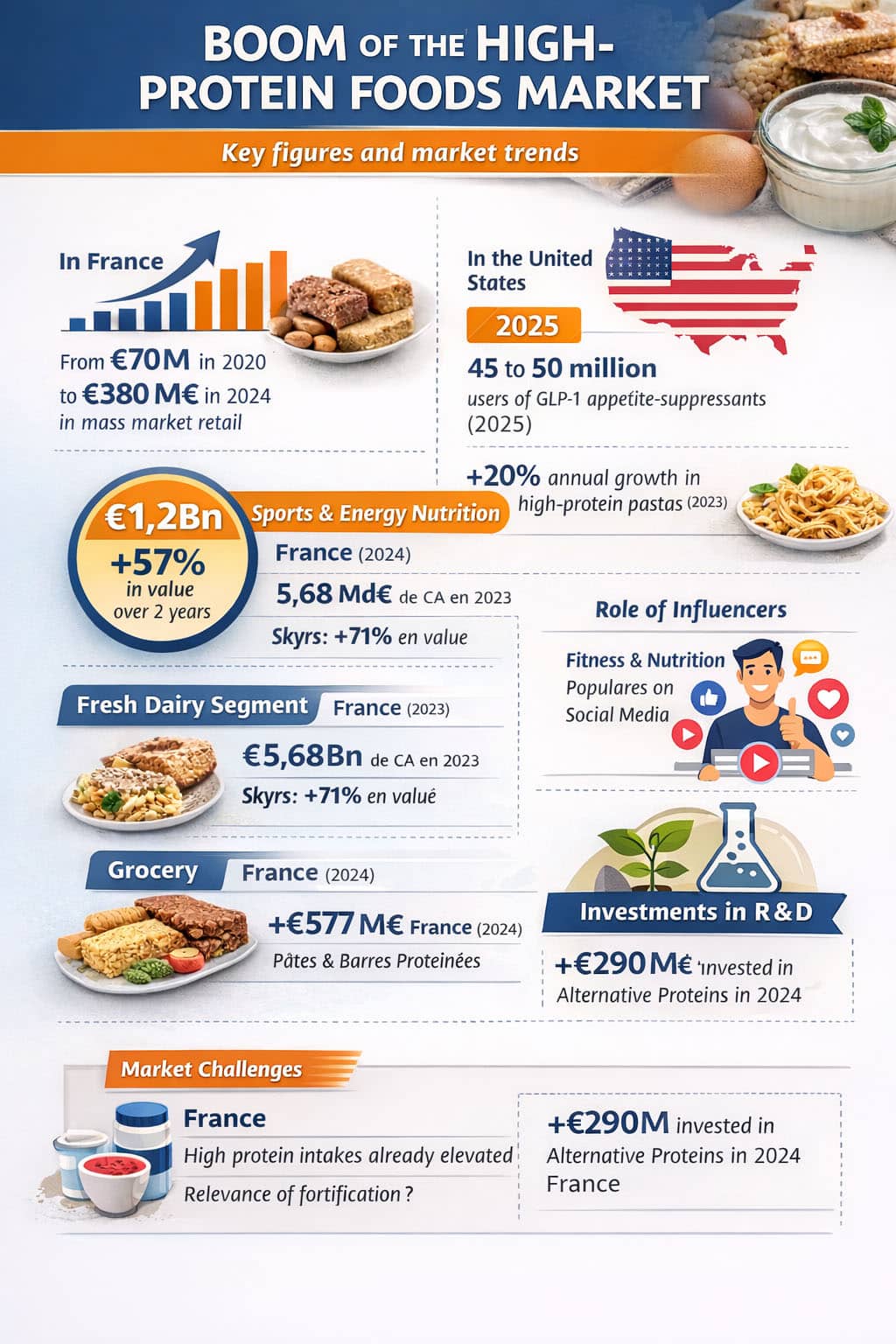

- The revenue of high-protein products has been multiplied by more than 5 between 2020 and 2024

- The fresh segment dominates this category, with skyr and protein yogurts leading the way

- Growth is driven by value, with premium prices 20% to 100% higher

- The market extends beyond fresh products to include grocery items (pasta, bars, snacks)

- 71% of French people engage in regular physical activity, fueling demand for high-protein products

- 24.6 billion USD: Global market size of protein powder in 2024

- >40 billion EUR: Expected global market size of protein powder over the next 10 years

- +7%: Average annual growth of the global protein powder market

- 70%: Percentage of American consumers declaring they want to increase their protein intake

- 27%: Market share claimed by Danone in Greek and high-protein yogurts in the United States

- 380 million EUR: Revenue of high-protein foods in French supermarkets in 2024

- +443%: Growth in revenue of high-protein foods in French hypermarkets and supermarkets between 2020 and 2024

- >500 million EUR: Annual sales of high-protein products in France across all channels

- 243.8 million EUR: Revenue of skyr in France

- +71.1%: Growth in value of skyr in France between 2022 and 2023

- 80.8 million EUR: Revenue of fresh high-protein yogurts in France in 2023

- +44.5%: Growth in value of fresh high-protein yogurts in France between 2022 and 2023

First and foremost, it’s important to note that the development of high-protein foods has been supported by other marketing trends we’ve observed, particularly at the SIAL 2022 and 2024 trade shows. One such trend is the search for alternatives to animal proteins, which has notably driven the short-lived plant-based meat industry. In 2024, we observed that proteins were THE trend not to miss in the food market (we provide some illustrations of this in this article).

A rapidly growing sector

The high-protein food market is showing exceptional performance in developed countries. For example, in just four years, the revenue generated by these products in France has grown from approximately 70 million euros to over 380 million euros in supermarkets. This spectacular growth reflects a profound shift in dietary behaviors, partly linked to the increasingly widespread use of appetite suppressants (GLP-1) like Ozempic.

In the United States, GLP-1 medications are now used by 12% to 15% of households. This represents 45 to 50 million consumers, or about 1/8 of the population. Their use modifies both patients’ eating habits and their spending, which decreases by an average of 6%. Consumption shifts towards less fatty, less sugary, or less caloric products, which has been a boon for high-protein products.

Functional nutrition focused on sports and energy includes energy drinks, skyr, and protein bars. This market has more than doubled in two years. Growth reached +57% in value and +42% in volume during this period.

This expansion is accompanied by sustained innovation. For example, in just the first three months of 2025 in France, 23 new products explicitly promoting protein content were launched in stores. These products also respond to more fragmented consumption throughout the day. Portions are therefore individualized. High-protein products address this trend by being positioned as convenient solutions, consumable at different times of the day.

Finally, regarding consumption behaviors, it’s important to discuss consumer profiles. The functional logic is particularly pronounced among young adults and urban professionals. High-protein products are especially popular among those under 35. This segment tends to have more unstructured meals and gives greater importance to snacking. In the case of fresh high-protein desserts, one in ten consumers now buys at least one, and these products create new consumption occasions outside of meal times.

Fresh products: The engine of growth

The fresh segment constitutes the core of the high-protein food market. The figures we cite below pertain to the French market and illustrate its scale and segmentation. With 5.68 billion euros in revenue in 2023, it shows growth of +13% in value despite a slight decline in volume (-0.7%). This performance is largely explained by the premiumization towards protein-enriched products.

Skyr and high-protein products alone account for 37% of the fresh segment’s revenue growth, representing about 3% of volumes. Their growth is impressive: +63.4% in volume and +71.1% in value in 2023. These Icelandic products have won over consumers thanks to their creamy texture and natural protein richness.

Sports high-protein products remain niche. They represent only 0.6% of volumes but have exceptional pricing at 8.18 euros per kilogram. Importantly, 75% of these volumes are incremental, creating new consumption occasions.

Skyr and high-protein products account for 37% of the fresh segment’s revenue growth, representing about 3% of volumes.

The US market: A pioneer in high-protein products

The US market plays a structuring role in the evolution of the global high-protein food market. The dairy sector there represents approximately 113 billion euros in revenue. Greek and high-protein yogurts occupy a central position, accounting for over a quarter of the market in value.

Unlike Europe, consumption in the US is largely oriented towards snacking. Products are designed to be consumed at any time of the day, often as partial meal replacements. The rise of GLP-1 treatments has reinforced this logic, with concerned consumers seeking protein-rich products that are low-volume and easy to consume.

The potential impact of these developments on the US food market is already measured in billions of dollars. Even if European regulatory frameworks limit certain claims, the dynamics observed across the Atlantic offer a prospective view of possible evolutions in Europe, particularly in terms of formats, segmentation, and functional promises.

Brand strategies

Price pressure

Danone created the high-protein segment in France in 2019 with its HiPro brand. The dairy giant already claims 3 million consumers and aims for the 17 million French people who regularly engage in sports. Its dominant position translates into an 86.5% market share in value in the fresh high-protein segment. In the skyr segment, Yoplait leads with 50% of volumes. This performance is supported by controlled pricing.

However, this hegemony attracts private-label brands. In France, Carrefour now offers equivalents of comparable quality but 30% cheaper. Lidl has also expanded its Envia and Milbona ranges with attractive prices.

Competitive pressure is therefore exerted both on prices and innovation, in a context where high-protein products remain significantly more expensive than standard references. The price gap generally ranges between +20% and +100%. This price difference remains acceptable to consumers as long as the functional promise remains clear and credible.

At SIAL 2024, we met the Portuguese startup Frol Explorer, which patented a system to add plant proteins to Dolce Gusto capsules. Their goal was to capitalize on the rising trend of functional nutrition.

Expansion into grocery and new formats

The protein trend extends far beyond the fresh segment. Barilla, for example, launched its Protein+ range with 20% plant protein. These pastas provide 40% of the recommended daily protein intake per 100 grams consumed.

The wellness pasta segment represents 77.1 million euros in revenue in France but shows a slight decline in value (-1.7%). This effect is attributed to the decline in organic products. However, volumes increased by +2.7%, reflecting price pressure. In the US, high-protein pasta already represents about 7% of the pasta aisle and records annual growth close to 20% in volume. European manufacturers are closely watching what happens in the US, anticipating that American trends will replicate in Europe.

Protein cereal bars are also gaining ground. Their market share has risen from 3.3% in 2021 to 5.2% in 2023. This progression reflects the expansion of consumption occasions towards snacking and snacking.

Even bread is not immune to the high-protein food trend. Here’s an example found at the SIAL 2024 trade show, showcasing how the trend is now invading all food categories.

Investments in R&D

Manufacturers are investing heavily to support this growth, which contrasts sharply with the stagnation in food innovation we observed a few years ago. Simply put, investments are now much more selective and systematic than in the past.

Some concrete examples:

- Bel is dedicating 7.5 million euros over three years to its R&D center in Vendôme. This facility employs 80 staff and tests 2,100 recipes annually. The goal: achieve a 50% dairy and 50% fruit and plant-based portfolio by 2035.

- The Cocagne project illustrates this innovation dynamic. This partnership between Bel, Avril, Lallemand, and Protial benefits from a 9-million-euro investment over three years, supported by France 2030. In total, 290 million euros were invested in alternative proteins in the first half of 2024.

- Danone is also focusing on specialized nutrition, with 8.5 billion euros in revenue in 2023. The group is investing 70 million euros in Steenvoorde for a medical nutrition line capable of producing 20 million liters annually.

Conclusions

Trends and outlook

The analysis of innovation trends reveals contrasting developments. The ProtéinesXTC 2025 barometer shows an increase in new products in 2023 (+8% in France) not confirmed in 2024 (-4.9%). This stabilization suggests market maturation.

Trends in boom favor sensory variety (+3.1 points), energy, and well-being (+1.6 points). Conversely, plant-based products decline (-2.3 points), as does ecology (-1.7 points). Pleasure reaches 63.8% in France (+3 points), explaining the success of products combining nutritional benefits and indulgence.

This shift towards nutritional hedonism opens new perspectives. Fun and portable formats particularly appeal to young consumers. The challenge for brands is to maintain the balance between health promises and taste pleasure.

Challenges and limitations

Despite this growth, the sector faces several challenges. The vast majority of the population in industrialized countries already exceeds nutritional recommendations (0.8 to 1g of protein per kg per day).

The example of skyr illustrates this marketing discrepancy. This product contains about 10g of protein per 100g, equivalent to a standard petit-suisse, but sells for a much higher price. This situation raises questions about the actual added value of certain product positions.

The market can nevertheless continue its growth in value even if nutritional legitimacy is contested. It leverages self-image, perceived performance, and functional effects. This logic resembles the foodification of nutraceuticals, where food adopts the codes of dietary supplements.

Frequently Asked Questions about the High-Protein Food Market

What is the current size of the French high-protein food market?

The French high-protein food market in supermarkets represents over 380 million euros in 2024, compared to approximately 70 million euros in 2020. This spectacular growth of over 400% in four years reflects enduring enthusiasm for these products. Functional sports/energy nutrition broadly accounts for 1.2 billion euros.

What are the main segments driving this growth?

The fresh segment dominates with skyr (243.8 million euros) and sports high-protein products (80.8 million euros). Skyr shows growth of +71% in value in 2023. Beyond fresh products, protein-enriched pasta and cereal bars are gaining ground. Sports drinks have grown by +119% in two years.

Who are the target consumers of these products?

Initially aimed at athletes, these products now attract a broader audience. 71% of French people report regular physical activity, and 85% associate sports with health. Young urban professionals are the core target, drawn by performance-oriented branding and portable formats.

How are prices evolving in this market?

High-protein products sell on average for 20% to 100% more than their conventional equivalents. This premiumization drives value growth. However, the arrival of private-label brands democratizes access with prices 30% lower than national brands.

What are the sector’s future prospects?

The market is expected to continue growing, driven by innovation and expansion into new segments. Sports nutrition in supermarkets could exceed 400 million euros by 2026-2027. The challenge lies in maintaining the balance between health promises and taste pleasure to appeal to the general public.

![Illustration of our post "SIAL 2024: 12 tips to organize your visit [Guide]"](/blog/app/uploads/sial-2018-etude-de-marche-france-alimentation-1-120x90.jpg)