This article provides a comprehensive analysis of the bulk market, based on the latest available statistics. I analyse in particular the situation in France and Belgium.

Bulk retail is no longer confined to specialized organic stores. Between new EU regulations and consumer expectations adapting to the economic context, the bulk market follows different dynamics depending on the country. My analysis focuses on two countries that correspond to the 2 core territories of my market research firm: France, where the sector is struggling to regain its pre-crisis momentum, and French-speaking Belgium, which shows broader but mainly occasional adoption.

Key takeaways

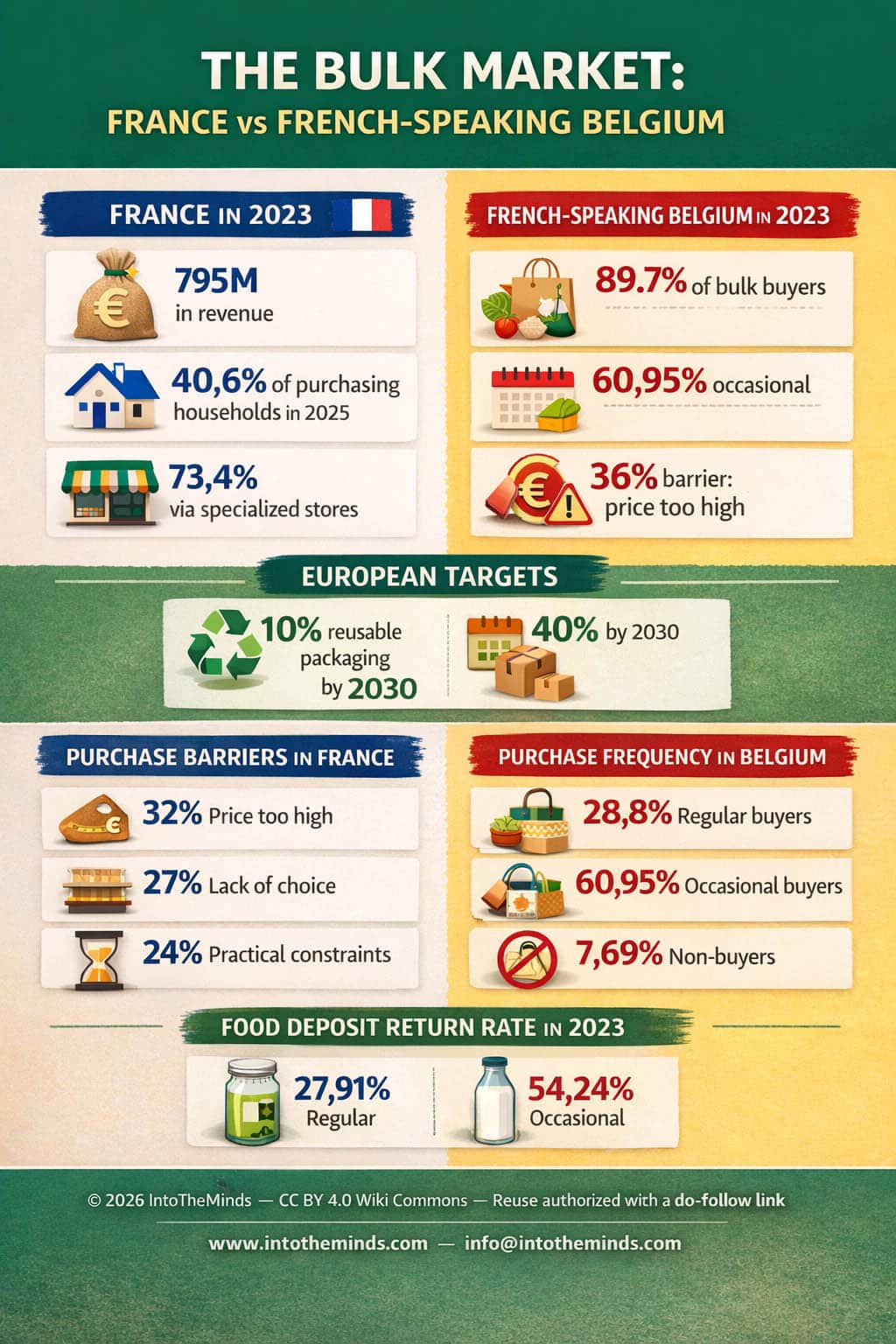

- The French bulk market was worth €795 million in 2023, with 40.6% of purchasing households in 2025

- In French-speaking Belgium, 89.7% of consumers buy bulk products, but mainly occasionally

- Europe requires 10% reusable packaging by 2030, then 40% by 2040

- Price remains the main barrier: 32% of French consumers and 56% of Belgian non-buyers mention it

- Specialized channels still capture 73.4% of the French market value

The regulatory context is reshaping the landscape

The European Union has reached a decisive milestone with its PPWR regulation, applicable from August 12, 2026 in the 27 member states. This legislation sets ambitious targets: 10% reusable packaging by 2030, then 40% by 2040. These figures are not arbitrary. Each European generated 180 kg of packaging waste in 2021, representing a 21% increase compared to 2011.

European regulations may sometimes be mocked (remember the caps that must remain attached to bottles), but without structural change, projections remain alarming:

- +19% packaging waste by 2030

- +46% plastic packaging waste.

In this context, bulk retail is no longer just an ecological niche but becomes one of the key levers of the European “reduce-reuse-refill” strategy.

This regulatory transformation significantly alters the landscape for industry players. Retailers must now integrate these constraints into their medium-term strategy, while consumers see new purchasing solutions emerging. A quick Google search for “PPWR regulation” will confirm this—publications and service offerings are multiplying.

Some stores offer only bulk products. These can then be sold in large containers, as illustrated in this photo.

France: state of the bulk market

The French bulk market is undergoing a reconstruction phase. The figures reveal a volatile trajectory: 40% of purchasing households in 2019, then a drop to 31% in 2021, followed by a rebound to 40.6% in 2025. Paradoxically, this increase in penetration (+1.6 points between 2024 and 2025) is accompanied by a 4.3% decline in value.

This apparent contradiction is explained by purchase intensity. In 2025, French consumers made an average of 5.5 annual visits to bulk sections, with an average basket of €8.11 and an annual spend of €45.5 (+3.2% only). These amounts remain modest compared to the sector’s ambitions.

| Indicator | France 2023 | France 2025 | Change |

|---|---|---|---|

| Revenue | €795M excl. VAT | – | -4.3% |

| Purchasing households | 30% | 40.6% | +1.6 point |

| Annual visits | 6.5 | 5.5 | -15% |

| Average basket | – | €8.11 | – |

| Annual spend | – | €45.5 | +3.2% |

The breakdown by channel reveals another reality: specialized retailers still account for 73.4% of the market value, compared to only 26.6% for general retailers. This dominance is explained by differentiated purchasing behavior: €54 average annual spend in specialized channels versus €18 in traditional mass retail.

Bulk must first be competitive and simple before being merely virtuous

Barriers to adoption

Many surveys have been conducted in France on this topic. My analysis is that the obstacles to bulk development in France remain largely unchanged. In 2025, the TOP 3 barriers to purchase were:

- 32% of consumers considered prices per kilo to be higher

- 27% could not find all the products they were looking for

- 24% felt that self-service is not always convenient.

Time and organizational constraints also weigh heavily: 22% say bulk takes too much time, and the same proportion mention organizational constraints. More concerning, 20% cite lack of product information and poorly maintained sections, while 18% have no suitable store nearby.

Poorly maintained sections and cleanliness are barriers to bulk purchasing. In this photo, you can see one of the inherent issues of this type of retail. Some careless customers do not consider others. Self-service systems generate hidden costs (cleaning) if retailers want to guarantee customer satisfaction.

These barriers are not ideological. On the contrary, they highlight that bulk must first be competitive and simple before being merely virtuous. This reality is particularly relevant in a context where 79% of French people report feeling economically vulnerable or cautious after 20% cumulative inflation between January 2022 and January 2024.

Ecology is not the main driver of bulk retail in France

Drivers of adoption

Contrary to popular belief, ecology is not the main driver of bulk retail in France. In 2025, 64% of households primarily see it as a way to buy the right quantity, compared to 52% who cite avoiding unnecessary packaging. This logic of quantity and budget control has become central in the current economic context.

This hierarchy of motivations explains why some product categories perform better than others. Spices gained 3.5 penetration points between 2024 and 2025, biscuits 3.3 points, coffee 2.7 points, and legumes 2.6 points. These products share a common trait: they allow precise dosing based on needs.

Conversely, declining categories reveal the model’s limitations: hygiene and beauty products dropped by 10.3%, pet products by 5.3%, and pasta by 6.7%. These segments suffer from regulatory constraints, preservation issues, or less suitable offerings.

Fruits and vegetables are the products most naturally sold in bulk. For several years, bulk has expanded into other product categories.

Mass retail is catching up

General retailers still lag significantly. In 2023, they offered an average of 36 bulk references and 11 reuse references, compared to 590 and 100 in specialized organic stores, and 1200 and 20 in specialized bulk stores.

However, momentum is accelerating. In 2025, E.Leclerc held 17.7% market share in bulk among general retailers, Intermarché 16.3%, and Super U 11.2%. These figures reflect growing awareness, even if the base remains limited.

France is also developing an industrial approach. Nearly 200 experts are working across 16 workshops to standardize technical solutions, with tests planned in 15 stores. This structured approach could accelerate large-scale deployment.

The emergence of the bulk-deposit duo in France

A notable development is the convergence between bulk and deposit systems. In 2025, 32% of French households purchased bulk or food deposit products over the past 12 months, including 26% for bulk and 15% for food deposit. This increase (respectively 25% and 13% in 2024) suggests growing complementarity between these consumption models.

The reuse sector is already well structured: 60 washing centers identified across 18 regions, 12.5 million packages cleaned and returned to the market in 2023, more than 13 million packages collected, and around 1,000 collection points.

Return rates vary significantly by channel: 15% in mass retail, 47% in specialized organic stores, 35% in bulk stores, 87% in home delivery, and 80% in specialized drive-through services. This disparity highlights the importance of distribution channels in system performance.

Belgium: analysis of the bulk market

French-speaking Belgium presents a radically different profile. In 2023, only 7.69% of respondents reported never purchasing bulk products, compared to 28.8% regular buyers and 60.95% occasional buyers. This exceptional penetration is explained by a broader definition of bulk.

Indeed, 87% of Belgian bulk buyers purchase fruits and vegetables, 46% bread and pastries, and 42% dried fruits. This extension to fresh products mechanically increases penetration, as bulk covers part of everyday food purchases.

| Buyer type | French-speaking Belgium 2023 | Main categories |

|---|---|---|

| Regular buyers | 28.8% | Fruits and vegetables (87%) |

| Occasional buyers | 60.95% | Bread and pastries (46%) |

| Non-buyers | 7.69% | Dried fruits (42%) |

Integration into traditional channels

French-speaking Belgium stands out for integrating bulk into mainstream retail. In 2023, 89% of respondents did their grocery shopping in supermarkets and hypermarkets. For bulk, 32% of regular buyers and 38% of occasional buyers purchased it most often in these stores.

This widespread presence contrasts with France. Local stores remain relevant (16% of regular buyers and 18% of occasional buyers), but mass retail clearly dominates. This distribution suggests a more advanced normalization of bulk in Belgium.

Channel diversity confirms this trend: 44% shop in local stores, 20% source directly from producers or farms, 13% from specialized bulk stores, 13% from organic supermarkets, and 12% from local organic grocery stores.

Motivations and barriers

The motivations of French-speaking Belgian consumers align with those observed in France. Waste reduction ranks first (62%), followed by reducing food waste (47%), environmental preservation (43%), and savings from paying for the product rather than packaging (37%).

Selection criteria reflect similar pragmatism: quality (58%), price (54%), freshness (52%), and local or seasonal origin (48%). This hierarchy confirms that bulk grows sustainably only when it combines environmental benefits with tangible advantages.

Despite high satisfaction (80% of buyers or former buyers are satisfied), barriers remain strong. High prices are cited by 36% of buyers, lack of product information by 27%, concerns about preservation by 22%, and inconvenient transport and storage by 22%.

Among non-buyers, price rises to 56%, followed by lack of sales points (35%), transport and storage constraints (35%), and difficulty anticipating containers (29%). These obstacles show that bulk adoption is hindered by everyday practicality and economics, not ideological resistance.

Deposit systems in Belgium

French-speaking Belgium also shows strong adoption of deposit systems. In 2023, 27.91% of respondents usually bought products with deposit packaging and 54.24% did so occasionally. Glass dominates (78%), followed by plastic (32%), metal or stainless steel (19%), and wood (15%).

The experience is generally well rated, with 45% giving a score of 4 out of 5 and 31% giving 5 out of 5. However, barriers are logistical: 35% cite home storage, 32% lack of nearby collection points, 28% loss or breakage before return, 26% unclear instructions, and 25% transport to return points.

These obstacles highlight a key challenge: in Western Europe, the spread of deposit systems and bulk retail will depend on making return loops almost invisible to consumers.

Bulk market: European outlook

France and Belgium illustrate two complementary stages of the European market. France shows a more structured, regulated, and industrialized sector, but still limited in usage frequency. French-speaking Belgium reveals broader cultural adoption, but often more occasional and focused on a few categories.

Both markets converge on one key point: bulk grows when it reduces waste, but above all when it helps buy the right quantity, better control budgets, and simplify everyday life. This reality will shape the sector’s future at the European level.

The transition to mass bulk retail will not depend solely on regulatory targets for 2030 or 2040. It will depend on the ability of industry players to make bulk simpler, more visible, and more competitive than traditional packaged products. The companies that succeed will be those that move beyond a purely ecological approach to deliver real everyday value.

Frequently asked questions about the bulk market

Is bulk really cheaper than packaged products?

The reality is nuanced. According to ADEME, a bulk product can be 10 to 15% cheaper than a packaged equivalent, mainly because you are not paying for packaging. However, 32% of French consumers still consider per-kilo prices higher in 2025. This perception is explained by several factors: bulk products are often organic or higher quality, purchase volumes remain low, and direct comparison with promotions on packaged products may disadvantage bulk.

Why is the bulk market stagnating in France despite environmental challenges?

The French paradox shows that ecological awareness is not enough. In 2025, 64% of households primarily see bulk as a way to buy the right quantity, compared to 52% who mention avoiding packaging. Practical barriers dominate: time constraints (22%), organizational difficulties (22%), lack of convenience (24%). In a context where 79% of French people feel economically vulnerable, bulk must first be simple and competitive before being virtuous.

How can the relative success of bulk in French-speaking Belgium be explained?

French-speaking Belgium benefits from a broader definition of bulk, including fruits and vegetables (87% of buyers), bread and pastries (46%). This extension to everyday fresh products facilitates adoption. Moreover, 89% of consumers shop in mass retail, where bulk is better integrated than in France. This normalization explains why 89.7% of French-speaking Belgians buy bulk, even if often occasionally.

Which bulk products perform best?

In France, the best-performing categories in 2025 are spices (+3.5 penetration points), biscuits (+3.3), coffee (+2.7), and legumes (+2.6). These products share common characteristics: precise dosing, good preservation, and flexible use. Conversely, hygiene and beauty declined by 10.3% and pet products by 5.3%, penalized by regulatory or preservation constraints.

Will European regulation accelerate bulk development?

The European regulation applicable from August 2026 sets binding targets: 10% reusable packaging by 2030, then 40% by 2040. This regulatory pressure should accelerate retailer investment in bulk and reuse solutions. However, success will depend on making these solutions more practical and competitive than packaged alternatives, beyond legal constraints.