The fermented beverage market is so promising that it is prompting some major international groups to rethink their production strategy. Originating in the United States, this market is now also developing in Europe, as shown by the statistics we analyze in this article.

The fermented beverages sector is undergoing a period of major transformation. Kombucha, fruit kefir and other probiotic drinks are gradually establishing themselves in our consumption habits. This evolution reflects a profound shift in consumer expectations that we observe daily as a market research agency. Consumers now increasingly favor healthier alternatives to traditional sodas. Analysis of the fermented beverages market reveals contrasting dynamics depending on geographic regions, with the United States leading the way and Europe rapidly catching up.

Contact the IntoTheMinds market research agency

Key takeaways

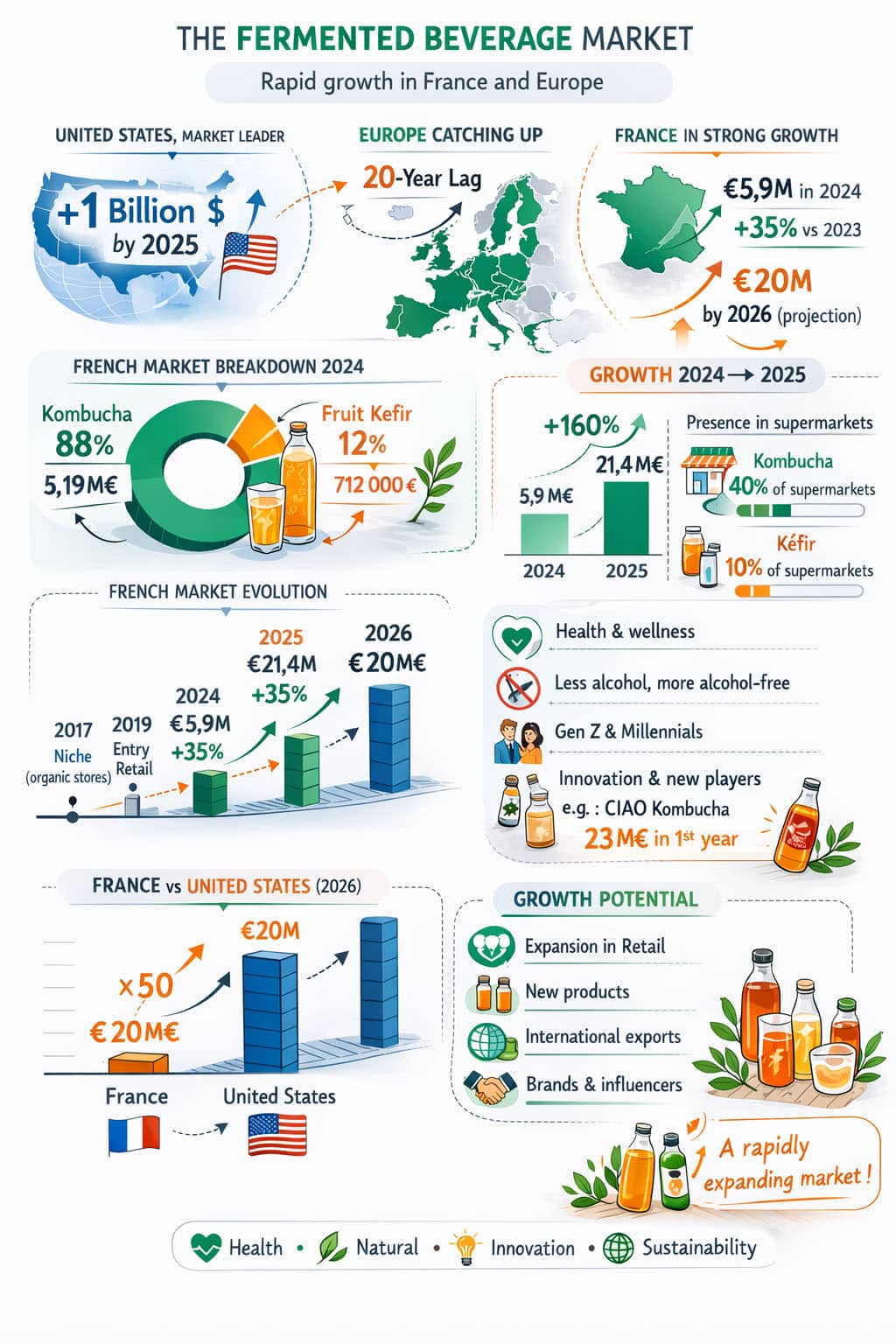

- The U.S. fermented beverages market exceeds one billion dollars in 2025

- France records 35% growth in 2024

- Kombucha represents 88% of the French market

- Kefir is booming with +122% growth

- Projections estimate €20 million in revenue for the fermented beverages segment in France by 2026

- Europe lags 20 years behind the United States but is catching up quickly

- $9.09Bn: projected global kombucha market by 2030

- $4.26Bn: global kombucha market size in 2024

- $1Bn+: U.S. fermented beverages market size in 2025

- 35%: growth of the French fermented beverages market between 2023 and 2024

- €21.4M: fermented beverage revenue in mass retail in 2025

- 160%: sales growth in mass retail between 2024 and 2025

- 88%: kombucha market share in France in 2024

- 12%: fruit kefir market share in France in 2024

- 28%: kombucha growth in France between 2023 and 2024

- €712,410: fruit kefir revenue in France in 2024

- 122%: fruit kefir growth in France between 2023 and 2024

- €32.7M: fermented milk market revenue in France in 2024

- €23M: revenue generated by the brand CIAO Kombucha in 2025

Geographic analysis of the fermented beverages market

The United States, global engine of the sector

Across the Atlantic, the development of fermented beverages is part of a mature industrial logic and a broader growth dynamic of the non-alcoholic beverage segment. In 2025, this market reaches a valuation exceeding one billion dollars, driven by massive adoption among millennials. One in two consumers from this generation regularly includes kombucha or kefir in their diet.

This American lead is not accidental. As early as 2016, the acquisition of KeVita by PepsiCo marked the entry of major food industry players into this segment. This operation symbolized the transition from an artisanal market to a global industrial dimension. The success factors in the United States rely on three pillars: early adoption by young adults, greater sensitivity to digestive health issues, and the search for alternatives to conventional sodas.

One in two millennials regularly includes kombucha or kefir in their diet.

Australia confirms the international dimension

The geographical expansion of the phenomenon is confirmed in Australia. In 2018, Coca-Cola acquired Organic & Raw Trading Co., manufacturer of the Mojo brand. This operation took place while Australia was recording the world’s fastest kombucha growth within the non-alcoholic beverage universe.

This Australian dynamic validates several strategic hypotheses. It demonstrates that the market has reached a critical size sufficient to attract global leaders. It also confirms that growth is not limited to the United States. Finally, it positions fermented beverages as a strategic segment on a global scale.

Europe in a phase of accelerated catch-up

The Old Continent shows a significant time gap. In 2025, Europe lags approximately 20 years behind the United States. Nevertheless, several signals point toward an acceleration of European development.

The European context is particularly favorable. The rise of sophisticated alcohol-free beverages creates fertile ground. Data from INSEE confirm the structural decline of alcoholic beverages in France between 1960 and 2018. This long-term trend favors the emergence of natural alternatives. The gradual integration of fermented beverages into European gastronomy reinforces this dynamic.

France: from niche to democratization

France perfectly illustrates this transition. In 2017, fermented beverages were barely present in mass retail. The offer was concentrated in specialized organic distribution channels and associated with natural products, digestive health and pioneering entrepreneurship.

The turning point began in 2019 in a context of restructuring within the non-alcoholic beverages market. Carbonated soft drinks without alcohol represented €2.27 billion (+3.1%), while still non-alcoholic beverages reached €3.17 billion (-0.5%). Fruit juices declined by 5%, in contrast with the growth of flat fruit beverages (+6.8%), tea drinks (+3.3%) and especially energy drinks (+20.7%).

| Indicator | 2024 (France) | Change vs 2023 | Market share |

|---|---|---|---|

| Total fermented beverages revenue | €5,894,470 | +35% | 100% |

| Kombucha | €5,185,535 | +28% | 88% |

| Fruit kefir | €712,410 | +122% | 12% |

| Kombucha presence in supermarkets | 40% | – | – |

| Kefir presence in supermarkets | 10% | – | – |

Alongside fermented beverages, the fermented milk segment shows a different level of maturity. In France, revenue reached €32.7 million in 2024 (+13.7% in value vs 2023), despite a volume decline of 2.8%.

This development illustrates value creation and premiumization. Fermented milk represents 30.5% of revenue and 26.4% of volumes within ultra-fresh pasteurized milk. The kefir segment stands out particularly with +15% in volume and +23.8% in value compared with 2023.

Market evolution over time

2024: first consolidated snapshot

The year 2024 marks a decisive turning point with the first precise measurement of the French market. Total fermented beverages revenue reached €5,894,470, representing growth of 35% compared with 2023. This increase corresponds to an additional €1.5 million.

The breakdown reveals the dominance of kombucha with €5,185,535 (+28% vs 2023), representing about 88% of total revenue. Fruit kefir, although starting from a smaller base with €712,410, shows explosive growth of 122%. Distribution confirms the expansion potential. Kombucha is present in 40% of French supermarkets, kefir in only 10%. These figures mean that 60% of supermarkets still do not offer kombucha and 90% ignore kefir. The development potential remains considerable.

2025: scaling up in mass retail

The year 2025 confirms the acceleration of the phenomenon. In mass retail, fermented beverage revenue jumped to €21.4 million, representing growth of nearly 160%. This spectacular increase demonstrates the democratization of the segment.

The market structure becomes clearer: kombucha retains 92% of the market share while fruit kefir represents 8%. In this segment, Labo Dumoulin holds 50% market share in mass retail. Projections estimate total revenue of €20 million by 2026. This French perspective, although encouraging, reveals the persistent scale gap with the United States. While France aims for €20 million in 2026, the U.S. market already exceeds one billion dollars in 2025.

The generational extension: the CIAO Kombucha case

The year 2025 also marks the arrival of players from new ecosystems. The launch of CIAO Kombucha by YouTuber Squeezie illustrates this diversification. Since its launch, this brand has generated €23 million in revenue and reached the 18th position among soft drink brands in its first week.

This performance reveals several insights. A single brand can generate revenue higher than the entire 2024 market. Historically, the primary target group consisted of consumers aged over 35. This launch explicitly targets younger consumers, significantly expanding the market potential. Another key lesson is that when influencers of Squeezie’s scale take interest in a market, it indicates genuine potential. The kombucha market is therefore no longer anecdotal and should represent a significant growth lever in the future.

A structural shift in consumption habits

This development fits into a long-term transformation of consumption behavior. According to INSEE, the share of spending on alcoholic beverages has been declining in favor of non-alcoholic beverages since 1960. Fermented beverages benefit from this structural dynamic.

Several factors converge: reduced alcohol consumption, the sophistication of alcohol-free beverages, integration into gastronomy and the search for alternatives to sodas. This transformation goes beyond a simple trend and reflects a deeper societal evolution.

Challenges and future outlook

Despite this promising growth, the sector faces several challenges:

- The protection of product names remains problematic. The term kombucha is not protected, unlike kefir which legally refers to milk kefir. This situation already generates disputes that could affect consumer trust in the future.

- The potential arrival of major industrial players is another challenge. Groups such as the Dutch company Refresco are closely observing this market. The emergence of private-label products could alter the competitive balance.

Nevertheless, the outlook remains favorable. The gap with the United States offers considerable catch-up potential. The evolution of consumption habits, particularly among younger generations, supports this dynamic. Product innovation and the expansion of distribution channels remain the main growth drivers.

Frequently asked questions

What is the current size of the French fermented beverages market?

In 2024, the French fermented beverages market represents €5.9 million in revenue, with 35% growth compared with 2023. In mass retail specifically, this figure reached €21.4 million in 2025, representing a 160% increase.

What are the main differences between kombucha and fruit kefir?

Kombucha results from the fermentation of infused tea and dominates the market with 88% of sales. Fruit kefir comes from the fermentation of fruits and sugar with specific translucent grains. Although it represents only 12% of the market, kefir shows explosive growth of 122% in 2024.

Why is Europe lagging behind the United States?

Europe shows a gap of approximately 20 years compared with the United States. This delay is explained by later adoption of wellness trends, different distribution channels and more complex regulation. However, recent developments show an acceleration of European catch-up.

What are the growth prospects for 2026?

Projections estimate €20 million in revenue in France by 2026. This growth is driven by expanded distribution (60% of supermarkets still do not offer kombucha), broader generational targets and product innovation.

How can the recent success of CIAO Kombucha be explained?

The launch of CIAO Kombucha by Squeezie illustrates the generational expansion of the market. This brand has generated €23 million in revenue since its launch and reached the 18th position among soft drinks. Its success demonstrates the ability to attract young consumers, who were traditionally less targeted by this segment.